Swiss Franc The Euro has fallen by 0.05% to 1.0753 EUR/CHF and USD/CHF, December 9(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The market is hopeful today. The Johnson-von der Leyen dinner is seen as evidence that both sides see one more opportunity, and sterling is among the strongest currencies today. Hopes of a 0 bln+ fiscal stimulus package in the US helped stir animal spirits and lift US stocks to record highs yesterday. Nearly all the Asia Pacific equity markets but China rallied, led by Japan and South Korea, to snap a two-day decline. Europe’s Dow Jones Stoxx 600 is at new highs, with energy and consumer discretionary the strongest sectors, and US stocks build on yesterday’s gain. Benchmark

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brazil, Brexit, Canada, China, Currency Movement, Featured, Hungary, newsletter, Poland, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.05% to 1.0753 |

EUR/CHF and USD/CHF, December 9(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The market is hopeful today. The Johnson-von der Leyen dinner is seen as evidence that both sides see one more opportunity, and sterling is among the strongest currencies today. Hopes of a $900 bln+ fiscal stimulus package in the US helped stir animal spirits and lift US stocks to record highs yesterday. Nearly all the Asia Pacific equity markets but China rallied, led by Japan and South Korea, to snap a two-day decline. Europe’s Dow Jones Stoxx 600 is at new highs, with energy and consumer discretionary the strongest sectors, and US stocks build on yesterday’s gain. Benchmark 10-year yields are a little firmer, with the US yield near 0.94%. Italian and Greek yields are at new record lows, while Portugal’s benchmark yield remains a little below zero. Note that the yield of the index of US corporate bond yields below investment grade fell to a record low yesterday (~4.34%). The US dollar is trading heavily against all the major currencies. Emerging market currencies are mostly higher, with the eastern and central European currencies leading the way. A few Chinese banks reportedly were dollar buyers late in the official session after the dollar fell below CNH6.5 in the offshore market for the first time in a couple of years. Gold is paring its recent gains. It had rallied more than $30 in the first two days this week and is off about $10 today near $1860. In contrast, crude oil is higher after slipping lower in the past two sessions. The January WTI contract is pushing back above $46 a barrel. |

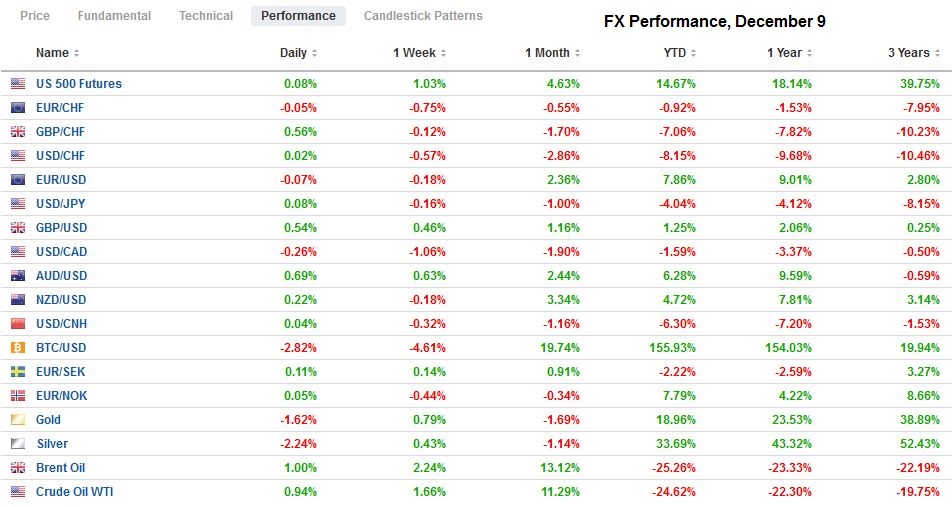

FX Performance, December 9 - Click to enlarge |

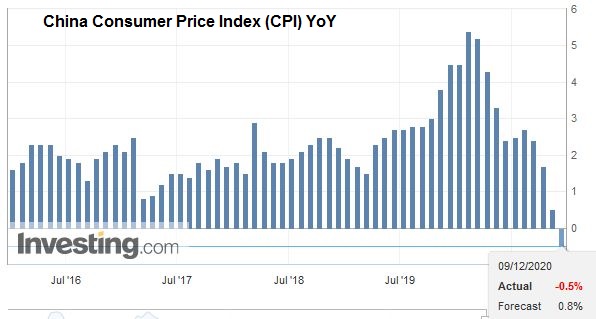

Asia PacificChina’s CPI fell below zero for the first time in more than a decade. The 0.5% year-over-year decline in November is weaker than expected. However, this likely overstates the case. Food prices are the culprit. They fell 2% year-over-year as pork prices plunged 12.5%. |

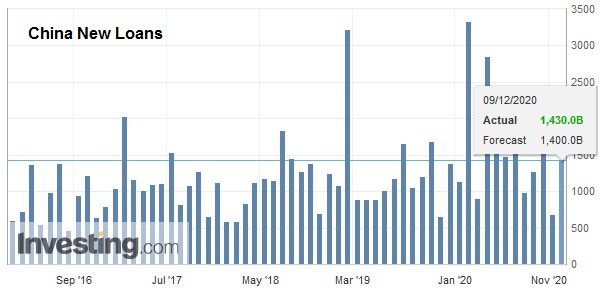

China New Loans, November 2020(see more posts on China New Loans, ) Source: investing.com - Click to enlarge |

| Recall that in October, pork prices fell for the first time in nine months. The price of pork fell by 3% in October and another 6.5% in November. Service prices rose by 0.3% in November, the same pace as October. Core inflation, which excludes food and energy, remained stable at 0.5%. The deflation in producer prices lessened. |

China Consumer Price Index (CPI) YoY, November 2020(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

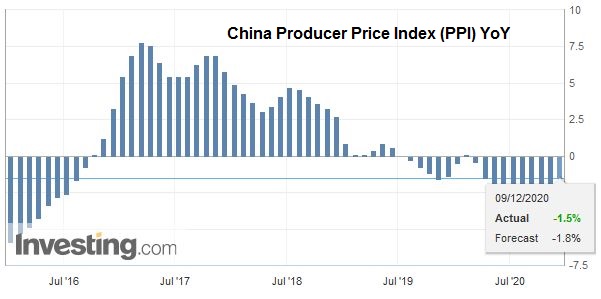

| The November PPI was 1.5% below a year ago after a 2.1% decline in October. The recent rise in industrial commodities, like coal, oil, iron ore, and copper, may be helping mitigate the deflationary pressures at the producer level. |

China Producer Price Index (PPI) YoY, November 2020(see more posts on China Producer Price Index, ) Source: investing.com - Click to enlarge |

Separately, China reported strong lending figures. New bank loans rose by CNY1.43 trillion in November, more than double the CNY690 bln in October. Lending from shadow banking slowed slightly to about CNY700 bln (from ~CNY730 bln). Bank lending accounted for the rise in aggregate financing by CNY2.13 trillion from CNY1.42.

Japan reported a surge in October core machinery orders, which is a proxy for business investment. After falling by 4.4% in September, core machinery orders jumped 17.1% in October, starting Q4 on a solid note. The median forecast in the Bloomberg survey anticipated a 2.5% gain. The monthly gains were sufficient to lift the year-over-year rate into positive territory (2.8%) for the first time since November 2019.

The dollar is in a narrow range against the yen through the European morning (~JPY104.05-JPY104.25). The first set of options that roll-off today are struck at JPY104.40. Monday’s range (~JPY103.90-JPY104.30) continues to dominate the uninspiring price action. The Australian dollar has broken higher from the recent consolidation and approached $0.7480. The intraday momentum studies are stretched. Nearby resistance is seen in the $0.7500-$0.7520 area. The PBOC set the dollar’s reference rate at CNY6.5311, a little lower than the models suggested. The dollar held yesterday’s low near CNY6.5210 and rose to a three-day high around CNY6.5460. The dollar recorded its high in a spike in late dealings thought to be Chinese banks.

EuropeThere are two developments to note regarding the UK-EU negotiations. Most importantly, the Irish Protocol has been agreed upon, which resolved several outstanding issues about the Irish border. It also allowed the UK to drop several controversial measures in the Internal Market Bill and the Taxation Bill that undermined the Withdrawal Agreement. This is a different set of negotiations from the trade talks but is a necessary part of the overall Brexit. Second, Johnson and von der Leyen will have dinner together tonight. Although significant gaps remain between the two sides, many are hopeful that a way forward can still be forged. Separately, the UK has indicated it will drop the tariffs on US goods for its part of the Airbus-Boeing dispute. This is a unilateral gesture. Recall that the EU, having won its case about improper subsidies to Boeing, was allowed to slap tariffs on $4 bln of US goods. Previously, the US won its case that Airbus was illegally subsidized and won the right to put a levy on $7.5 bln of European goods. These included Scotch whiskey, biscuits, and clotted cream from the UK. Retaliatory tariffs for the US “national security” levies on imported steel were not addressed. The news is just breaking, and the full details are not yet available, but Merkel, who steps down next year, appears to have struck a compromise with Poland and Hungary over the EU budget and stimulus plans. Both the zloty and forint strengthened on the news. The compromise needs to receive broad approval, but the initial indication is promising. |

Spain Industrial Production YoY, October 2020(see more posts on Spain Industrial Production, ) Source: investing.com - Click to enlarge |

The euro is bid but remains in a range set on Monday (~$1.2080-$1.2165). Last week’s high was just shy of $1.2180. With the ECB meeting tomorrow, new buying may be deflected today. Initial support is seen at $1.2100. Sterling is bid and traded at a three-day high near $1.3460. Recall that before last weekend, it traded to almost $1.3540. Sterling had traded quietly in the Asia Pacific session and rallied throughout the European morning. The euro is trading at three-day lows against sterling. It had reached almost GBP0.9150 on Monday and is now near GBP0.9000. A break could see GBP0.8950-GBP0.8970.

America

The White House submitted its own stimulus proposal for $916 bln. It includes a $600 stimulus check to most Americans, which the bipartisan proposal did not do. However, to fund it, the extra federal unemployment insurance was cut. Separately, the House passed the defense bill ($740.5 bln). President Trump has threatened to veto because it approves the renaming of bases and does not strip social media companies’ protections. However, the margin of approval (335 to 78) could withstand a veto.

The Bank of Canada meeting may be of little consequence today. It is not expected to do anything, including holding a press conference or updating forecasts. The central bank has promised not to lift the overnight target rate of 25 bp until at least 2023. It continues to buy C$4 bln a week of government bonds. In the statement, the central bank will likely assure businesses and investors that there is scope to provide more support if necessary. It would be unusual to draw attention to the Canadian dollar, which is trading at two-year highs amidst a broad weakening of the US dollar in recent weeks. Deputy Governor Beaudry will give a speech tomorrow, but the exchange rate does not appear particularly salient. This year, it is up less than 1.5% against the US, making it one of the underperformers among the major currencies.

Brazil’s central bank meets later today and is widely expected to keep the Selic rate at the record low of 2%. The dollar is trading near six-month lows against the Brazilian real. Support for the greenback is seen in the BRL4.9750-BRL4.9880. Mexico reports November CPI. It is expected to have fallen below 4% for the first time since July. Seasonal sales have been brought forward. The core rate is expected to have fallen for the first time since January 2015. The central bank meets next week, and despite the softening of inflation, many expect the pause in the rate-cutting cycle continues into early next year. Banxico delivered a 25 bp rate cut in September to bring the target to 4.25%.

The US dollar has been nesting for a few sessions between roughly CAD1.2770 and CAD1.2825. The momentum indicators are stretched and have not been alleviated by the sideways activity. The greenback may be pushed lower first, and there may be some support near the CAD1.2740-CAD1.2750 area, but the charts seem to warn against chasing it now. The greenback remains pinned near its trough against the Mexican peso. It is holding just above MXN19.70. The next interesting chart level is near MXN19.65, the 200-week moving average. On the upside, an initial resistance is seen in the MXN19.75-MXN19.80 area and then MXN19.90.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

FX Daily, July 6: New Record Number of Covid Cases Doesn’t Curtail Appetite for Risk

2020-07-06

Overview: A new daily high number of contagions globally has been reported, but the risk-appetites have been stoked. Chinese stocks have been on a tear. The Shanghai Composite rallied 5.7% today to bring the five-day advance to 13.6%. Most other regional markets, including Hong Kong, rallied as well (3.8%). Australia was the main exception, and it pulled back by 0.7%. It is still up a solid 3.4% over the past five sessions.

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

2020-07-22

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

2020-08-18

The NASDAQ rallied 1% yesterday to record highs as the Dow Industrials struggled, and the S&P 500 was able to eke out a small gain. The coattails were short, and the strength of the yen may have contributed to a 0.2% loss of the Nikkei. Still, its 6.2% advance this month is the best among the G10.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

2020-08-31

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

2020-09-15

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

2020-11-20

Overview: News that the stimulus talks between the House Democrats and Senate Republicans was the excuse traders were looking for to extend the US equity gains yesterday, but shortly after the close, confirmation that Treasury was not going to agree to extend several Fed facilities sent stocks reeling.

FX Daily, November 24: Diverging PMIs Fail to Give the Dollar Lasting Support

FX Daily, November 24: Diverging PMIs Fail to Give the Dollar Lasting Support

2020-11-24

Overview: The contrast between the eurozone and US preliminary PMI readings caught the short-term market leaning the wrong way, and the dollar snapped back after extending its recent losses. However, today the US dollar is back on its heels and returning to yesterday’s lows against most major currencies.

FX Daily, December 1: No Follow-Through After Month-End Adjustments

FX Daily, December 1: No Follow-Through After Month-End Adjustments

2020-12-01

The near-record rallies seen in the major equity markets in November may have contributed to the month-end drama yesterday. There has been no follow-through activity. Stocks bounced back, and the US dollar is heavy, with few exceptions.

Tags: #USD,Brazil,Brexit,Canada,China,Currency Movement,Featured,Hungary,newsletter,Poland