There have been three general issues that the macro-fundamental picture has revolved around this year: trade, growth, and Brexit. On all three counts, conventional wisdom seems unduly optimistic, and this may have helped dampen volatility. A series of signals suggest that the US and China remain far apart in trade negotiations. The US wants China to promise to increase agriculture imports from American farms to more than twice the 2017 peak. Not only is China understandably reluctant to commit to it, but the US is seeking a concession like European powers did in the 19th century. The US wants a fixed sphere of interest in China’s agriculture market and is quantified at bln. Ironically, at the turn of the 20th-century, the US defended China’s sovereignty

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, ECB, Featured, Federal Reserve, GBP, Hong Kong, newsletter, trade, US

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

There have been three general issues that the macro-fundamental picture has revolved around this year: trade, growth, and Brexit. On all three counts, conventional wisdom seems unduly optimistic, and this may have helped dampen volatility.

A series of signals suggest that the US and China remain far apart in trade negotiations. The US wants China to promise to increase agriculture imports from American farms to more than twice the 2017 peak. Not only is China understandably reluctant to commit to it, but the US is seeking a concession like European powers did in the 19th century. The US wants a fixed sphere of interest in China’s agriculture market and is quantified at $50 bln. Ironically, at the turn of the 20th-century, the US defended China’s sovereignty and territorial integrity from Europe and Japan that were trying to carve it up into spheres of influence.

In the middle of the negotiations, the US deemed it necessary and proper to slap anti-dumping duties on Chinese ceramic tiles. It did not derail talks. It is part of “talking and fighting” as the Chinese call this type of negotiation. However, the situation escalated last week as the US Congress passed with two measures aimed at the situation in Hong Kong. First, it required the State Department to affirm Hong Kong’s autonomy every year to extend its special trade privileges and access to the US market. Second, another bill banned sales crowd control weapons like tear gas, to Hong Kong. A presidential veto can be overridden. If Trump does nothing, by the end of the week ahead, the bills become laws and could very well threaten the trade talks.

The violence in Hong Kong is indeed worrisome. Reports suggest many injuries are taking place after the students have been taken into custody. As intense and scary it is, there are several more confrontations between governments and their own citizens, like in Bolivia, Chile, Lebanon, and Iran, not to mention France, that have been more violent and resulting in more deaths. The moral righteousness in some quarters seems both cause and effect of the new Cold War II thinking that allowed the Wall Street Journal to show a chart of the US trade deficit with China, and the date it identified to begin was the Tiananmen Square Massacre.

The reports of China’s camps for Uighur Muslims are heart-wretching. Man’s ability to be wolf to man knows no bounds even under the veneer of civilization and education. And yet, I found it hard to explain to a Chinese friend recently how the US penal system is not a close cousin. Blacks and browns are over-represented. It is not based on religion as it is in China. Americans believe they have been liberated from religious distinctions. Class is the key, and justice is a commodity. Often it appears, the more money you have, the better the justice you can buy.

Life itself has become a class struggle. How long one lives is partly a function of genetics, but also a function of access to good health education, healthier food choices (M&A and concentration among grocers), and affordable health care itself. What about the human rights of the victims of the more than 350 mass shootings in the US this year? The number of people killed in each is more than the number of people killed in the five months of Hong Kong demonstrations.

This is framed such to help illustrate that, contrary to conventional wisdom, China is not a big Japan. The lessons that US Trade Representative Lighthizer drew from his days confronting Tokyo may not apply to Beijing. Japan was totally reliant on US defense, and it accepted the basic premises of Pax Americana. Japan had little interests outside of its neighborhood. China is more than a horse of a different color. It is a different kettle of fish. IT has a different world view and value system. It has the military might to rival the US as a regional hegemon (during peace times). Its interests are global, and access to its market, as it learned from the US, is another way to reward friends and punish adversaries. As the Chinese tariffs on US goods rose, those levied on others have generally fallen.

“Good progress” or “cautiously optimistic” characterization of the talks fan hopes that an agreement is still the most likely course of action. The length of time since the Americans claimed agreement in principle was struck on October 11 suggests that it was not only premature, which implies the US was hungry to be able to announce a deal, but also that the talks since have stalled. When negotiations stall, both sides often dig in and become less flexible.

Trump bragged that phase one accounted for about 60% of when he envisioned was the total deal. From China’s standpoint, that means that 60% of the tariffs should be rolled back. The US sees the tariff as both a stick to punish and carrot to induce the desired behavior.

On several occasions now Trump has threatened that if a deal is not struck, more tariffs will be imposed. The next set of tariffs (15% on roughly $160 of goods which includes many consumer goods) is to start on December 15. The Administration held out the possibility last week that these could be suspended during talks as were last month’s. If you were on the other side of the negotiating table, what might you conclude about the US?

Chinese President Xi has achieved what few have in recent years, and that is to unite the US Congress. The votes on the Hong Kong bills were nearly unanimous. It illustrates that the confrontation with China is not just about Trump. In fact, it increasingly appears that the differences between the main two US political parties are tactical rather than strategic vis a vis China. One side confronts China mano a mano, and the other side is more interested in confronting China at the head of a coalition of others. But the American political elite and most of the chattering class seem determined to confront China with the same moral fervor as the Soviet Union was challenged.

It is as if there is a new parlor game guessing whether Beijing prefers Trump to a Democrat contender. The President would have us believe China prefers a Democrat because they would not be a tough as him. Yet it seems that if China is to be challenged, is it better by a US acting alone or at the head of a coalition? Trump pulled the US out of the Trans-Pacific Partnership that had been part of the US pivot to Asia to ostensibly contain China. The Disruptor-in-Chief as estranged its European allies and has levied tariffs on Japan and German steel and aluminum imports on national security grounds.

The Trump Administration has demanded its allies pay more for the privilege of stationing US forces. Earlier this year, Japan balked at the US request for a five-fold increase in payments to the US. The 2019 budget earmarked about $1.8 bln for cost-sharing with the US. Reports indicate that Soth Korea, for example, is paying about $925 mln this year to house the 28.500 soldiers, and was requested to pay $5 bln in 2020. Who else could have gotten South Korea to sign a defense agreement with China a little more than a week ago?

Investors also seem too sanguine about the outlook for the UK election and, therefore, Brexit. Sterling rallied from $1.22 to nearly $1.30 between October 10 and October 17. Since then, it has chopped mostly between $1.28 and $1.30. The polls consistently show the Tories ahead of Labour. However, it is still not clear that it will secure a majority of seats in the new House of Commons. And even if it does garner a majority, or tries to rule as a minority government, and somehow gets the Withdrawal bills passed, Brexit is not over, nor has a no-deal departure been ruled out.

Assume the UK leaves on January 31, nothing changed on February 1. During a standstill agreement that runs to the end of 2020, the UK and EC will be negotiating a post-divorce trade deal. It will be like deja vu all over again. Brinkmanship, redlines, and deadlines. A ditch may be preferable to Johnson than asking for an extension on trade talks. And if no agreement is struck, the UK leaves with only the WTO rules to shape the new trade relationship with the EU, its most important trading partner. We think the risk is that sterling pulls back before the election toward $1.25-$1.26.

United StatesThe US, eurozone, and China each have one economic release next week that will command attention. There would seem much to chose from in the US, with several regional Fed manufacturing surveys for November, new home sales, durable goods orders, and the second look at Q3 GDP. However, we suspect the October personal consumption expenditure may be the most impactful for Q4 GDP forecasts. Consumption rose by an average of 0.5% a month through the first half before slowing to 0.3% in Q3. The median forecast in the Bloomberg survey anticipated a 0.3% increase. However, this is not in real terms, and when adjusted for inflation, real consumption may have only risen by 0.1%, which would be the weakest since February. With the Fed widely understood to be on hold in December, neither the PCE deflators nor the Beige Book will likely move the market. The headline PCE, which the Fed targets at 2%, may tick up 1.4% from 1.3%, while the core rate, which Fed officials talk about, is expected to be steady at 1.7%. If the core PCE deflator is the “preferred” measure as some journalists and analysts insist, it begs the question of why isn’t it targeted. |

Economic Events: United States, Week November 25 - Click to enlarge |

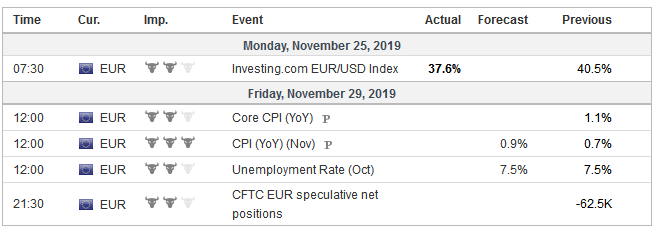

EurozoneThe eurozone reports the preliminary estimate for November CPI. The base effect means that its inflection is likely to rise for the next few months, starting with the November report. Consider that last November, consumer prices fell by 0.6%. They were flat in December before falling 1% in January. March and April 2020 will be considerably more difficult comparisons as CPI rose 1.0 and 0.7% in March and April of this year, respectively. The median forecast in the Bloomberg survey called for the headline rate to have fallen by 0.4%, which would still allow the year-over-year pace to accelerate to 0.9% from 0.7%. The core rate may have edged higher to 1.2% from 1.1%. The ECB meets next on December 12. It is nearly inconceivable that ECB moves then, regardless of the high-frequency economic data. The impact of the recent easing has not been fully felt yet. It is Largarde’s first meeting, and there is a greater degree of continuity between her and Draghi than Draghi and Trichet. The change in governance/management style means being less imperial, which was a knock on Draghi, especially by those that disagreed with the content of the policy, The data has not deteriorated, though the risks remain substantial. |

Economic Events: Eurozone, Week November 25 - Click to enlarge |

ChinaChina’s November PMI will be reported at the end of next week. Both the manufacturing and service components are expected to rise a little. The high-frequency data deteriorated in October, and the small gains November’s PMI would be suggestive of the stabilization of the world’s second-largest economy more broadly. Still, between demographics, debt-fuelled growth, and a vulnerable financial system, China’s challenges are serious, and the trade battle with the US is a distraction. President Xi, who is regarded as the most powerful leader since Deng Xiaoping and has his thought embedded in the Constitution, has seen his two big policy initiatives run into trouble: Made in China 2025 and the Belt Road Initiative. The former at the hands of the Americans and the latter under the weight of bad loans, it is becoming the colonial power that it hated by taking 99-year control of ports of insolvent sovereigns. The sales tax increase that went into effect on October 1 pulled output and sales into September. October will be payback. Retail sales jumped 7.2% in September and forecast to fall by more than 10% in October. Year-over-year, Japan’s retail sales probably contracted by almost 4%. Industrial production is likely to have unwound September’s 1.7% surge. Foreign demand (exports) and domestic demand weakened. A 2.0% decline in October would leave output 5.3% below year-ago levels, the weakest in six years. |

Economic Events: China, Week November 25 - Click to enlarge |

Tags: #GBP,Brexit,China,ECB,Featured,federal-reserve,Hong Kong,newsletter,Trade,US