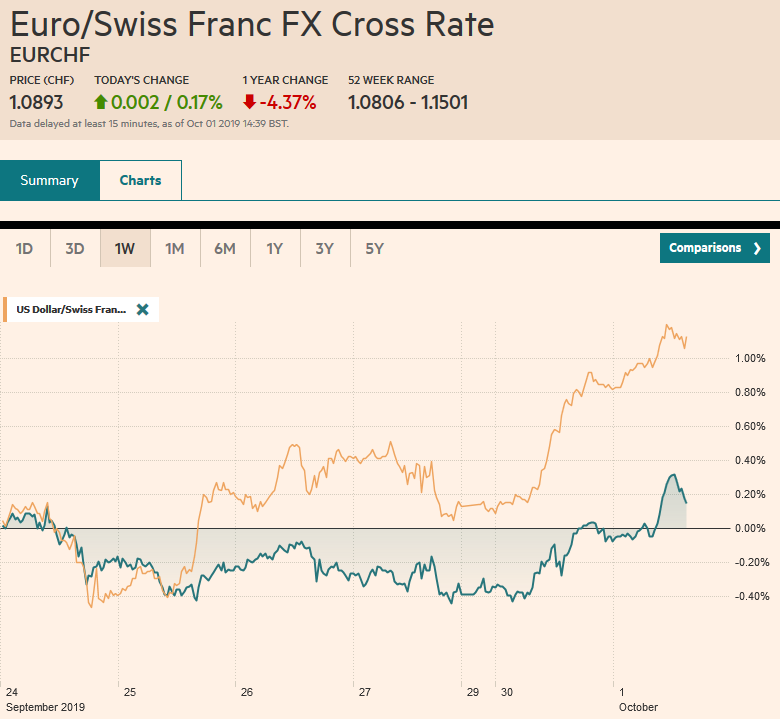

Swiss Franc The Euro has risen by 0.17% to 1.0893 EUR/CHF and USD/CHF, October 1(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The US dollar is rising against nearly every currency today as global growth concerns deepen. Japan’s Tankan Survey showed large manufacturers confidence is a six-year low. The Reserve Bank of Australia cut 25 bp as widely expected and kept the door open for more. The final EMU PMI ticked up from the flash, but it is still at a seven-year low. The MSCI Asia Pacific Index eked out a small gain, and a weaker yen facilitated a rise in Japanese shares. Europe’s Dow Jones Stoxx 600 rose initially but is threatening to end a three-day advance, while US shares are trading firmer. A poor

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, Currency Movement, EMU, EUR/CHF, Eurozone Consumer Price Index, Eurozone Core Consumer Price Index, Eurozone Manufacturing PMI, Featured, Japan, Japan Manufacturing PMI, Japan Unemployment Rate, newsletter, South Korea, U.K. Manufacturing PMI, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.17% to 1.0893 |

EUR/CHF and USD/CHF, October 1(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US dollar is rising against nearly every currency today as global growth concerns deepen. Japan’s Tankan Survey showed large manufacturers confidence is a six-year low. The Reserve Bank of Australia cut 25 bp as widely expected and kept the door open for more. The final EMU PMI ticked up from the flash, but it is still at a seven-year low. The MSCI Asia Pacific Index eked out a small gain, and a weaker yen facilitated a rise in Japanese shares. Europe’s Dow Jones Stoxx 600 rose initially but is threatening to end a three-day advance, while US shares are trading firmer. A poor reception to a bond auction in Japan seemed to have a knock-on effect and is lifting benchmark 10-year yields 4-6 bp. Oil is coming back bid after falling for the past five sessions, during which time November WTI tumbled roughly 8%. Gold, on the other hand, is extended its recent losses. It has lost about 3% over the past three sessions to trade near two-month lows (below $1460). The charts warn that the risk may extend toward $1400, where the breakout took place a few months ago. |

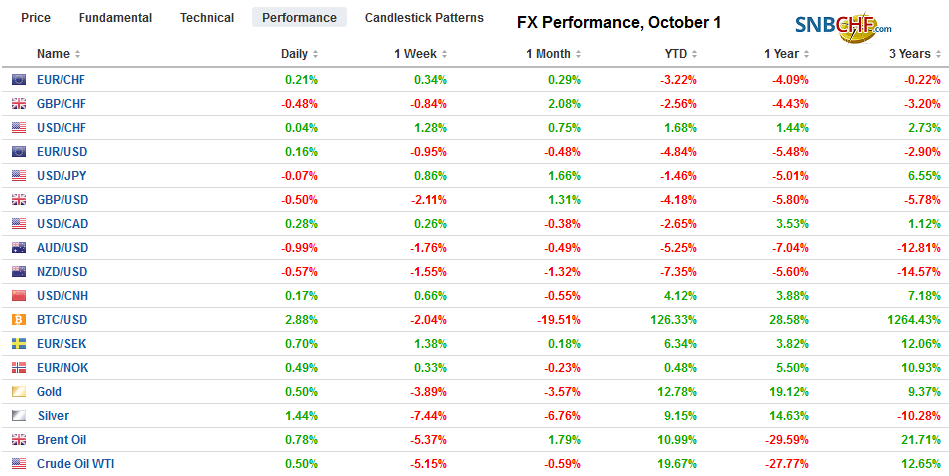

FX Performance, October 1 - Click to enlarge

|

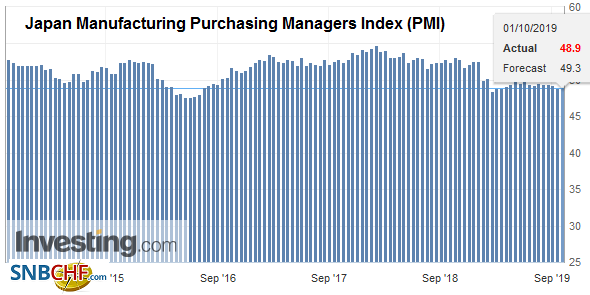

Asia PacificThe Tankan Survey results were a little better than expected for the most part but still reflected slowing from the last survey. All-industry capex plans were scaled back more than anticipated (6.6% vs. 7.4% previously and 7.0% forecast). Japanese manufacturers project the dollar to average JPY108.68 in the current fiscal year that ends in March 2020. In the first half of the fiscal year, it has averaged JPY108.64. The September manufacturing PMI was confirmed at 48.9 down from 49.3. It is the fifth consecutive month below the 50 boom/bust level and also suggests the sales tax increase that went into effect today (10% from 8%) may be hitting a weakening economy. |

Japan Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

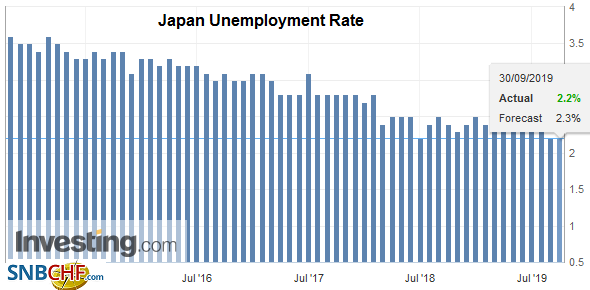

| While the unemployment rate and jobs-to-applicant ratio were flat (2.2% and 1.59 respectively), new jobs offers fell 5.9%, which may be an early warning sign as well. |

Japan Unemployment Rate, August 2019(see more posts on Japan Unemployment Rate, ) Source: investing.com - Click to enlarge |

Threatening to overshadow the economic data, the BOJ’s machinations in the bond market has disturbed what is often a sleepy market. First, the BOJ scaled back its purchases several times last month. Then yesterday it indicated it would reduce the bond it is buying except for the short-term tenors. It took on greater flexibility and suggested it could stop buying bonds with maturities of 25-years and longer.These changes have injected uncertainty into the market and saw the weakest reception at today’s 10-year bond sale in a few years. The BOJ is putting more emphasis on the yield curve, and Governor Kuroda has underscored this in recent comments. Not only is the BOJ trying to engineer higher long-term rates, but it is also expected to cut the short-term rate at a meeting at the end of the month. The sell-off in JGBs today appeared to spur the sell-off in US Treasuries.

The Reserve Bank of Australia delivered the widely expected 25 bp rate cut, bringing the cash rate to a record low of 75 bp. It signaled that this is not necessarily the end of the easing cycle. RBA Governor Lowe seemed again to emphasize the labor market’s performance going forward. That said, we expect the RBA to pause. The rate cuts and fiscal stimulus are already having an impact. The September PMIs ticked higher, and an index of house prices showed the largest rise since early 2017.

South Korean data illustrates the deflationary pressures in the region. Indeed, its September CPI fell to -0.4% year-over-year, the weakest on record. The core rate fell to 0.6% from 0.9%. Its full month trade figures were in line with the earlier updates. Exports fell 11.7% year-over-year, which is not quite as bad as August’s 13.8% drop (revised from -13.6%), while imports are 5.6% lower than a year ago, worse than August’s 4.2% decline. The September PMI fell to 48 from 49 and has not been above 50 since April. The central bank is likely to cut rates again later this month.

The dollar has risen to test last month’s high a little shy of JPY108.50. A move through there could sput a test on the JPY109 area, which it last saw two months ago. The 200-day moving average is found near JPY109.16. It has not traded above this average since May. Our idea of a sell-the-rumor, buy-the-fact activity on the Australian dollar lasted seconds as the move above yesterday’s highs met a deluge of selling. The Aussie was driven through $0.6700. It has spiked below $0.6700 three times in August and September but has not closed below there. Still, it needs to close above yesterday’s lows (~$0.6740) to avoid a bearish outside down day.

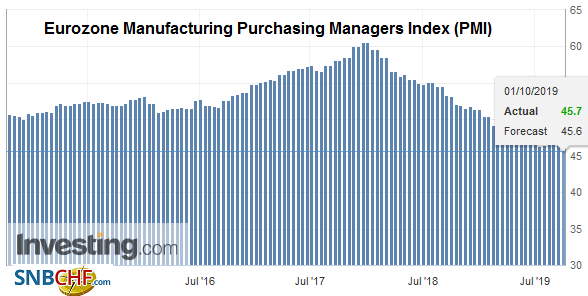

EuropeObservers have played up the opposition to the resumption of asset purchases by as many as eight ECB members. It is rarely acknowledged that most of the dissenting countries objected to asset purchases initially as well. Also, some of the objections were over the timing of the announcement. Perhaps the most unspoken pushback against these observers who are largely taken the creditors’ side in the debate, is asking what a realistic alternative is. Yes, fiscal support could be helpful, and it is coming but slowly. And in the meantime, yesterday’s German CPI posted its first back-to-back decline since October-November 2017. Today’s data drive home the point. The manufacturing sector in EMU is contracting (45.7 vs. 45.6 flash and 47.0 in August), and price pressures are moving in the wrong direction. New orders stand at a seven-year low. |

Eurozone Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

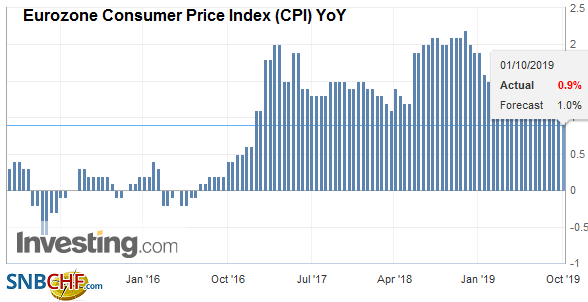

| The 0.9% aggregate CPI matches the lowest in almost three years. |

Eurozone Consumer Price Index (CPI) YoY, September 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

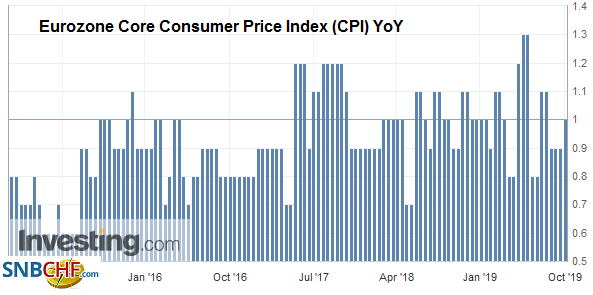

| Headline CPI peaked last October at 2.2%. Most of this is noise. Consider the signal: the core rate bottomed in 2015 at 0.6% and now stands at 1.0%. |

Eurozone Core Consumer Price Index (CPI) YoY, September 2019(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

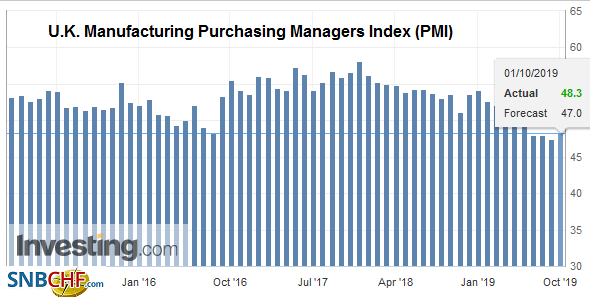

| The UK’s manufacturing PMI edged up to 48.3 from 47.4. This was better than expected but does not change anything materially. The manufacturing sector is contracting. Brexit uncertainty looms, and the market seems more convinced of a rate hike next year than how Brexit will play out. Prime Minister Johnson is expected to send a new text to Brussels later today ostensibly with new proposals for the Irish border. Early reports suggest that it seeks customs clearance on sides of the border. However, the initial reaction has not been favorable. Nevertheless, it is seen as likely the first serious proposals by the UK government since May was forced out. |

U.K. Manufacturing Purchasing Managers Index (PMI), September 2019(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The euro was sold to about $1.0880 before finding better bids, and it recovered to session highs in the European morning. Still, it is unlikely to push above $1.0920 without new developments. Despite the euro being at levels not seen since mid-2017, implied volatility remains subdued and in the lower end of the range seen over the past two months. Only a move above yesterday’s highs (~$1.0950) would lift the technical tone, and there is an option for about 1.1 bln euros there that will be cut today. Sterling is also trying to stabilize after testing $1.2260, its lowest level in nearly three weeks. Initial resistance is seen near $1.2310, with yesterday’s high around $1.2345 providing a more solid cap.

America

The economic calendar for North America today is packed. Investors will also watch the takedown of the Fed’s $100 bln overnight repo operation at the start of the new month. The US reports the September manufacturing PMI and ISM, August construction spending, and September auto sales. The US economy appears to have grown around 2% in Q3, and today’s data is unlikely to change this perception. The Fed’s Clarida and Bowman speak today, but the topics and forums do not lend themselves to much headline risk. This changes later in the week with more Fed speakers including Powell. Canada reports monthly GDP figures for July. The economy is expected to have grown 0.1% for a 1.4% year-over-year pace. A weaker number and especially a contraction would spur questions about the Bank of Canada’s neutral setting and could weigh on the Canadian dollar. Mexico reports its PMI and manufacturing and non-manufacturing indices. Soft data will encourage ideas that the Banxico is not done with its easing course after two cuts under its belt already.

The US dollar has been confined to a CAD1.32-CAD1.33 trading range since the middle of September. It stalled a little above CAD1.32 before the weekend, and by the rule of alternation, it is set to test the upper end. The top of the range also houses the 200-day moving average. The US dollar tested it several times in the second half of last month but failed to close above. A break of it signals a push toward CAD1.3345, the high from September 4 after the spike to around CAD1.3380 in the previous session. The greenback is also pushing higher against the Mexican peso. It has met the (50%) retracement objective of its dramatic decline in the first half of September near MXN19.78. The next retracement target is near MXN19.90. Initial support may be found near MXN19.74.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,Currency Movement,EMU,EUR/CHF,Eurozone Consumer Price Index,Eurozone Core Consumer Price Index,Eurozone Manufacturing PMI,Featured,Japan,Japan Manufacturing PMI,Japan Unemployment Rate,newsletter,South Korea,U.K. Manufacturing PMI,USD/CHF