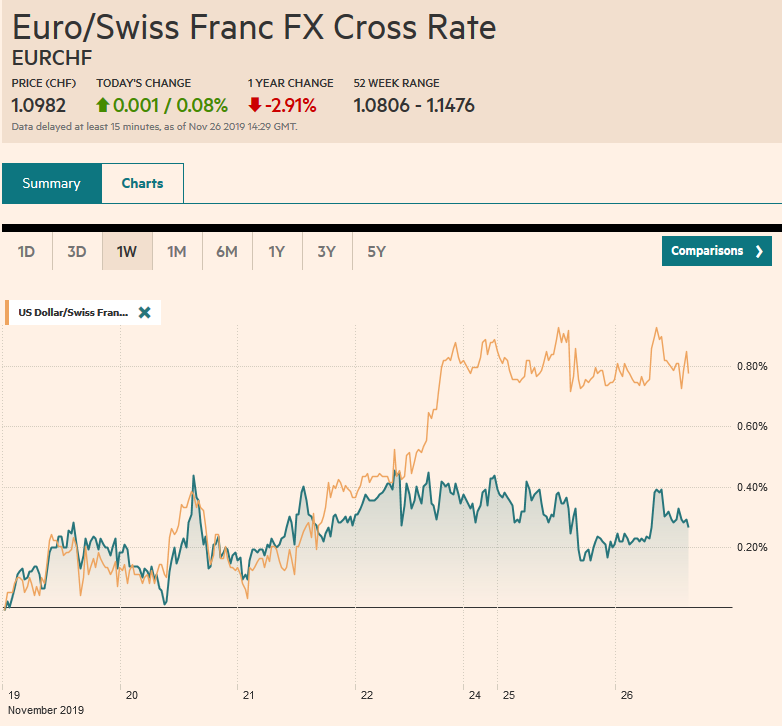

Swiss Franc The Euro has risen by 0.08% to 1.0982 EUR/CHF and USD/CHF, November 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Neither optimistic comments from Federal Reserve Chairman, that the economic glass is more than half full, nor a seemingly positive spin on the weekend fall calendar between Chinese and US officials have succeeded in deterring some profit-taking today. Most of the large markets in the Asia Pacific region were higher, with the notable exception Hong Kong, which began higher and reversed lower, South Korea, and India. Europe’s Dow Jones Stoxx 600 is little changed near the 4.5-year high set a week ago, and US shares are trading a little heavier. Global 10-year benchmarks are 1-3 bp

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, China, EUR/CHF, Featured, Federal Reserve, FX Daily, newsletter, trade, U.S. House Price Index, U.S. New Home Sales, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.08% to 1.0982 |

EUR/CHF and USD/CHF, November 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Neither optimistic comments from Federal Reserve Chairman, that the economic glass is more than half full, nor a seemingly positive spin on the weekend fall calendar between Chinese and US officials have succeeded in deterring some profit-taking today. Most of the large markets in the Asia Pacific region were higher, with the notable exception Hong Kong, which began higher and reversed lower, South Korea, and India. Europe’s Dow Jones Stoxx 600 is little changed near the 4.5-year high set a week ago, and US shares are trading a little heavier. Global 10-year benchmarks are 1-3 bp lower. Of note, China’s four-tranche dollar bond sale drew around $15 bln in demand for the initial $6 bln offering, helped perhaps by a bit wider premiums over Treasuries than last year’s sale. China’s government and corporates have raised about $200 bln this year in bond sales compared with about $150 bln in 2018. The dollar itself is narrowly mixed today. The Scandis are leading the advancers, while a poll showing a tighter race has spurred some profit-taking on sterling’s recent run-up. Most of the accessible emerging market currencies are lower, including the Turkish lira, which is facing US sanctions with the test of its Russian made anti-aircraft system exacerbating the frustration with the Syrian invasion. Gold held support near $1450, and oil prices are consolidating ahead of what is projected to be the first decline in US inventories in five weeks. |

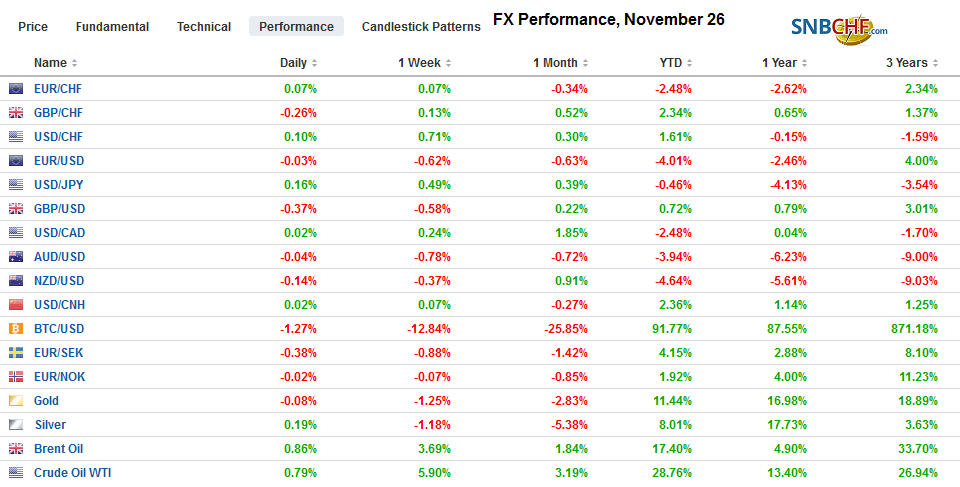

FX Performance, November 26 - Click to enlarge |

Asia Pacific

China reports that negotiators “reached a consensus” on how to “properly” resolve the outstanding issues” and will stay in touch for the phase 1 deal. It is not clear what this really means in terms of whether an agreement will be struck this year, but it sounds as if the 15% tariff on roughly $160 bln of Chinese goods that the US has threatened for the middle of December will not be implemented. Meanwhile, even though China appears to be making concessions, such as the intellectual property action yesterday and the lifting of the ban on American poultry, expectations of what can be agreed in phase one seemed to have been scaled back so that the key rests on whether there is a meaningful rollback of existing US tariffs. Near-term escalation appears to be off the table, for the time being, despite Trump’s threats to raise tariffs if there is no agreement. However, the fundamental disagreement is illustrated by Xi arguing for an equal deal while Trump claims that because China already has a large advantage, an agreement must favor the US.

Alibaba share prices jumped around 8% today in its Hong Kong debut, but the failure of Hong Kong Chief Executive Lam to make any concessions in the wake of the weekend vote threatens new unrest. Although the many state organs had anticipated a pro-government victory, the 40% of the vote it still garnered was seen as a solid base for next year’s more important elections. Separately, the economic disruption is clear in Hong Kong’s October trade figures. Exports were weaker than expected, falling 9.2% year-over-year after a 7.3% decline in September. Imports fell 11.5% following a 10.3% decline. Meanwhile, Trump still has a few days to decide what to do about the bills passed by Congress regarding Hong Kong. He can veto, and Congress would likely override the veto. He can do nothing, and the bills become laws in early December. Trump can sign the bill and turn them into law. The immediate question is how much it will impact the trade talks. Chinese officials have signaled this is a redline issue.

Japan’s 40-year bond sale saw strong demand. The bid-cover was 3.50-times compared with 2.69x at the last auction. The bond did well after the sale as well, even though more supply is expected next year. It yields about 45 bp and reflects the demand for positive yielding instruments. The BOJ will buy 5-10-year JGBs tomorrow and announce December’s purchase plans ahead of the weekend. Some expect the central bank to reduce the amount of 10-25 year bonds its buys from the JPY100 bln this month (reflecting a JPY20 bln reduction). It is expected to further scale back purchases next year and appears to have reduced its equity purchases as well as Nikkei trades at its best level of the year. The Nikkei gapped higher for the second consecutive session earlier today but reversed to close on its lows.

The dollar closed NY on its highs but below JPY109 and spiked to JPY109.20 in Tokyo before pulling back. There is a $2.3 bln option at JPY109.50 that rolls off today and a $1.1 bln option at JPY108.95 that expires tomorrow. Initial support is now seen near JPY108.80. One-month vol (~4.8%) is a new seven-month low. The Australian dollar is trading quietly within yesterday’s range and holding below $0.6800, where an A$507 mln option will be cut today. It does not appear done testing support around $0.6770. The dollar continues to trade in the range seen at the end of last week against the Chinese yuan (~CNY7.0250-CNY7.0450).

Europe

While many polls have shown the UK Tories with a double-digit lead of over Labour, the latest ICM/Reuters polls showed a tightening of the race. It gave the Conservatives a seven-point lead. There has been increased reflection on what happened in 2017 when the polls showed then-Prime Minister May ahead and anticipated the Tories would retain its majority. As we know, it unraveled quickly in the closing weeks of the campaign. One-month sterling implied volatility remains elevated (11.5%-12.0%).

The tension between Germany and France is the subject of much handwringing and chin-wagging. Although it has been overshadowed by other issues, like Brexit and the change of leadership at the EC and the ECB, and is a perennial issue for Europe, the divergence appears to have grown. Macron is ambitious, and Merkel is circumspect. Macron’s recent parry calling NATO “brain dead” apparently riled the German establishment. Germany is more sympathetic to expand the EU while Macron wants reform first. The tension between the “two pillars of Europe” could emerge as an important theme next year. Germany had complained that former French President Hollande was too weak but not finds Macron too strong.

The euro is trading in a less than a 15-pip range through the European morning. It has held above $1.10 (adn the month’s low near $1.0990). It needs to rise above yesterday’s high (~$1.1030) to be anything of note. Sterling is in half a cent range, mostly below $1.29. The pre-weekend low was near $1.2825, where a GBP235 mln option will expire today. Unless it, and really $1.2800 is convincingly penetrated, the flattish consolidation continues.

AmericaThe Federal Reserve conducted its first repo operation that covers the year-end roll. It was a 42-day operation that will be unwound on January 6. The Federal Reserve offered $25 bln, but the banks wanted nearly twice as much ($49.05 bln). On the other hand, the demand for the overnight repo (<$69 bln) was a little more than half of what the Fed made available ($120 bln). The next repo to cover the year-end period is December 2. The Fed announced it would boost the size of the operation to $25 bln from $15 bln. The Fed seems to be underestimating the demand. In the markets, over-the-turn funds were going for around 3.4% compared with the overnight collateralized rate of about 1.60%. There may be information gleaned by officials to see banks’ needs expressed, but the Fed could solve the problem by taking a page from the ECB’s playbook. The European Central Bank offers full allotment at its refinancing operation. Before the crisis, it was common to have banks bid for it like the Fed presently does. This is not about expanding the Fed’s balance sheet as it did during QE. These measures are about the transmission mechanism of monetary policy and to ensure it is smooth. Don’t confuse oil and gasoline, though they both are two liquids you put into a vehicle. |

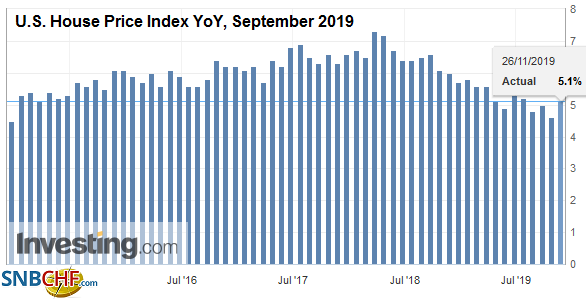

U.S. House Price Index YoY, September 2019(see more posts on U.S. House Price Index, ) Source: investing.com - Click to enlarge |

| Powell’s speech late yesterday did not break new ground. The downside risks that he and other officials have highlighted were not emphasized, though, and the economic glass was characterized as being “more than half full.” At the same time, he seems to emphasize the importance of the strong labor market. A deterioration of the outlook would likely meet the Fed’s definition of a material change that would warrant a reconsideration of policy.

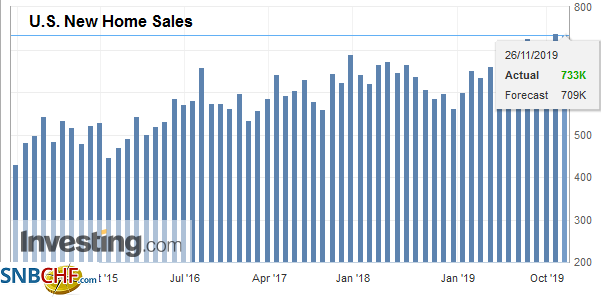

The US economic calendar is chock-full today, but little that provides participants with new trading incentives. October trade and inventory data will likely impact Q4 GDP forecasts, where the Atlanta and NY Fed tracking models warn of near-stagnation in the first half of the quarter. House prices and new house sales are not the stuff that typically moves the market. US oil inventories are expected to have fallen for the first time in five weeks, but the API estimate often does not jive with the EIA estimate that comes out on Wednesday. Mexico reports September retail sales. It is expected to have risen by about 0.5%, which would be the strongest since May, but will have little market impact given that Q3 GDP has already been reported (flat quarter-over-quarter). |

U.S. New Home Sales, October 2019(see more posts on U.S. New Home Sales, ) Source: investing.com - Click to enlarge |

The US dollar continues to consolidate in the upper end of the three-month range against the Candian dollar as it straddles the CAD1.33-handle. Resistance is seen in the CAD1.3325-CAD1.3350 area. Initial support is near yesterday’s low (~CAD1.3285), but a break of the pre-weekend low (~CAD1.3255) is required to take the pressure off the upside. The greenback also appears to be comfortable in the recent range against the Mexican peso (~MXN19.3150-MXN19.5525). That said, investors seem to be growing a bit more concerned about President AMLO’s efforts to window dress the fiscal position ahead of year-end. Also, the defense of the central bank’s independence recently by several former officials would suggest it is a response to some provocation.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,China,EUR/CHF,Featured,federal-reserve,FX Daily,newsletter,Trade,U.S. House Price Index,U.S. New Home Sales,USD/CHF