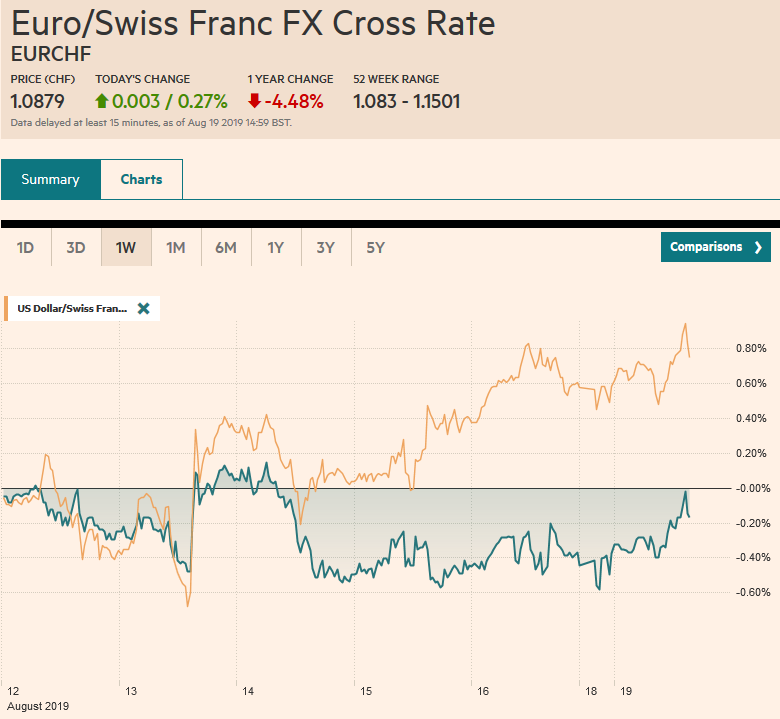

Swiss Franc The Euro has risen by 0.27% to 1.0879 EUR/CHF and USD/CHF, August 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: China announced some changes in its interest rate framework that is expected to lead to lower rates. This helped lift equity markets, which were already recovering at the end of last week from the earlier drubbing. Chinese and Hong Kong shares led the regional rally with 2-3% gains. The Nikkei gapped higher for the third time in six sessions, and the first two were followed by lower gaps. European stocks are higher, and the Dow Jones Stoxx 600 is trying to string the best two-day advance since the start of the year (~2%). US shares are firmer, and the S&P 500 may gap higher today

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, ARS, China, Currency Movements, EUR/CHF, Eurozone Consumer Price Index, Eurozone Core Consumer Price Index, Featured, FX Daily, Japan Trade Balance, newsletter, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.27% to 1.0879 |

EUR/CHF and USD/CHF, August 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: China announced some changes in its interest rate framework that is expected to lead to lower rates. This helped lift equity markets, which were already recovering at the end of last week from the earlier drubbing. Chinese and Hong Kong shares led the regional rally with 2-3% gains. The Nikkei gapped higher for the third time in six sessions, and the first two were followed by lower gaps. European stocks are higher, and the Dow Jones Stoxx 600 is trying to string the best two-day advance since the start of the year (~2%). US shares are firmer, and the S&P 500 may gap higher today above 2900 to bring last week’s high near 2950 into view. The animal spirits lifting equities is seeing a setback for bonds. The US 10-year yield is up six basis points, a little above 1.60%. European benchmark yields are mostly four-five basis points higher, though Italy’s 10-year yield is up nearly nine basis points ahead of tomorrow’s speech to Parliament by Prime Minister Conte that may proceed a vote of confidence or his resignation. The dollar is mostly a little firmer, though the euro’s upticks are an exception among the majors. The large accessible emerging market currencies, including the Russian ruble, South African rand, Turkish lira, and Mexican peso are all nursing small losses. Gold has retreated to test $1500. It had reached $1535 last week. Oil is about 1% firmer. |

. |

Asia PacificThe PBOC introduced a new benchmark rate, the loan prime rate, that will replace the one-year lending rate likely points to a small rate cut. It will be set monthly on the 20th of the month, and tomorrow’s setting will be compared to the 4.35% one-year lending rate. Meanwhile, while allowing the yuan to weaken, the PBOC continues to moderate the pressure. Today’s reference rate was set at CNY7.0365, while was slightly weaker for the dollar than the median forecast of CNY7.0374. The spot rate for the dollar is slightly stronger still, which means the downside pressure on the yuan may not have been exhausted. The dollar is also firmer against the offshore yuan (CNH) after slipping lower in the last two sessions. Japan reported July trade figures. The decline in exports moderated. The July decline of 1.6% year-over-year is the smallest since February and follows a 6.6% fall in June. Aircraft-related parts shipments to the US and exporting ships to Europe helped blunt continued weakness in autos (-11%), semiconductors (-7.7%) and chip-fabrication equipment (-14%). Exports to Asia were off 8.3% (-8.2% in June). This is included a 9.3% drop in sales to China and a 6.9% decline in sales to South Korea. Exports to Europe rose by 2.2% (-6.7% in June). Shipments to the US increased by 8.4% (4.9% in June). Japan’s imports slipped by 1.2% (-5.2% in June). Separately, note that South Korea reports its trade figures for the first 20-days of August on Wednesday and will generate more insight into the regional trade patterns. |

Japan Trade Balance, July 2019(see more posts on Japan Trade Balance, ) Source: investing.com - Click to enlarge |

The dollar gained against the yen in the past two sessions and is firmer today. A three-day advance would be the longest in a little more than a month. The dollar is holding above JPY106 for the second consecutive session, something it has not done since the start of the month. It needs to resurface above JPY107.00 to be meaningful, and there are about $765 mln in expiring options almost evenly divided between two strikes (JPY106.75 and JPY107.00) that may stand in the way. The Australian dollar is stuck in a well-worn range for the eighth consecutive session. It needs to resurface above $0.6820 or fall below $0.6735, and this does not look likely today.

Europe

Some discussion that if Germany were to slip into a recession, the government would loosen the purse strings has surfaced. We note that the worlds fourth-largest economy has contracted two of the past three quarters and meets the commonsense definition of a recession even if not two consecutive quarters. The Bundesbank warned today that the German economy may contract in Q3. Perhaps it will take a drubbing by the CDU and SPD in the September 1 state elections to spur action. Meanwhile, politics is very much in focus this week. UK’s Johnson will go abroad for the first time as Prime Minister. His visit to Germany and France Wednesday and Thursday is to reinforce the message that 1) the UK will leave with or without an agreement on October 31 and 2) Parliament is unable to stop it. Other reports have indicated that Germany, for one, has resigned itself to this eventuality.

Italy’s politics may come to a head this week. Prime Minister Conte will speak to the Chamber of Deputies tomorrow. He could resign or sit through a vote of confidence, which he will likely lose. The issue will become whether another coalition can be forged from the existing parliament, even if for a limited agenda, such as the passage of the 2020 budget and some political reforms, like reducing the number of deputies.

The UK risks incurring the wrath of the US. A Gibraltar court ruled at the end of last week against the US attempt to detain the Iranian oil tanker caught by the British ostensibly on its way to Syria, which is barred by Europe. European law does not prohibit the sale of Iranian oil as the US does. The Iranian oil tanker (now called the Adrian Darya 1 rather than Grace 1) is thought to be headed to Greece. Iran is expected to shortly release the Stenn Impero that it had captured.

| The ECB will not be happy with the revisions to the July CPI figures. The core rate was unchanged at 0.9%, but the headline rate was revised to 1.0% from 1.1%, while the monthly decline was revised to 0.5% from 0.4%. |

Eurozone Consumer Price Index (CPI) YoY, August 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

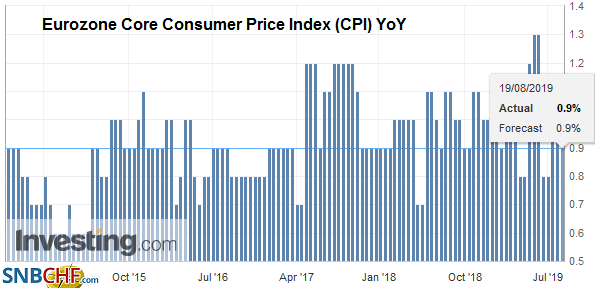

| The ECB is expected to unveil a multi-prong response to the downside risks that are materializing. On Thursday, the flash August PMI will be published, and more softness is expected. |

Eurozone Core Consumer Price Index (CPI) YoY, August 2019(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The euro is straddling the $1.1100 level but is inside the pre-weekend range. There is a nearly 550 mln euro option at $1.1115 that will be cut today. The intraday technicals warn that North American may probe the downside. The low from the end of last week was near $1.1065. Sterling was unable to push through $1.2175 that was approached ahead of the weekend. It has retreated to about $1.2115 in the European morning. Additional support is seen near $1.2085 today. Swiss sight deposits continue to rise. The nearly CHF3.8 bln increase last week was the most in around 18 months and is the fifth consecutive increase. This is what one would expect if the Swiss National Bank was intervening in the foreign exchange market to slow the franc’s ascent. The franc is near two-year highs against the euro, but the euro is finding a near-term base near CHF1.0835.

America

The North American economic and speaking calendar is nearly empty today. The US is expected to make a decision about Huawei today and whether it will grant a 90-day reprieve so the Chinese company can continue to maintain existing telecom networks, especially in rural areas. The broad export ban is not under review. Separately, the US will make a decision on Mexican tomatoes. The US accused Mexico of dumping tomatoes ($2 bln a year market) and slapped a provisional 17.6% duty since May. An agreement is needed today to provide a sufficient period for public commentary; otherwise, the provisional tariffs will become permanent on September 19.

Argentina remains in the spotlight. The peso stabilized in the second half of last week but will be challenged again. Fitch cut its sovereign rating by three notches (from B to CCC), and the negative outlook warns of the risk of another cut. S&P cut its rating to B- from B and also has a negative rating. Both of the decisions were announced after the markets closed ahead of the weekend. This leaves Moody’s B2 rating (equivalent to B by the others) out of line, but it had switched to a negative outlook from stable last month. President Macri was dealt another blow by the resignation of Treasury Minister Dujoune, who called for “significant renewal.” Today’s money market operation is of much interest. If the central bank does not roll-over the full ARS260 bln of funds (LELIQ) that is due, it will likely add to the pressure on the currency.

The US dollar is trading lower against the Canadian dollar for the third session, which if sustained, would be the longest losing streak in a month. There is near-term potential toward CAD1.3220 and then CAD1.3185. A break of this area would boost confidence US dollar top is in place (double top near CAD1.3340). Initial resistance is pegged near CAD1.3280 now. The dollar remains firm against the Mexican peso. The MXN19.76-MXN19.77 area stands in the way of a push toward the June high near MXN19.88. A break of MXN19.60 area would fan ideas that the greenback has put in a near-term high.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,ARS,China,Currency Movements,EUR/CHF,Eurozone Consumer Price Index,Eurozone Core Consumer Price Index,Featured,FX Daily,Japan Trade Balance,newsletter,USD/CHF