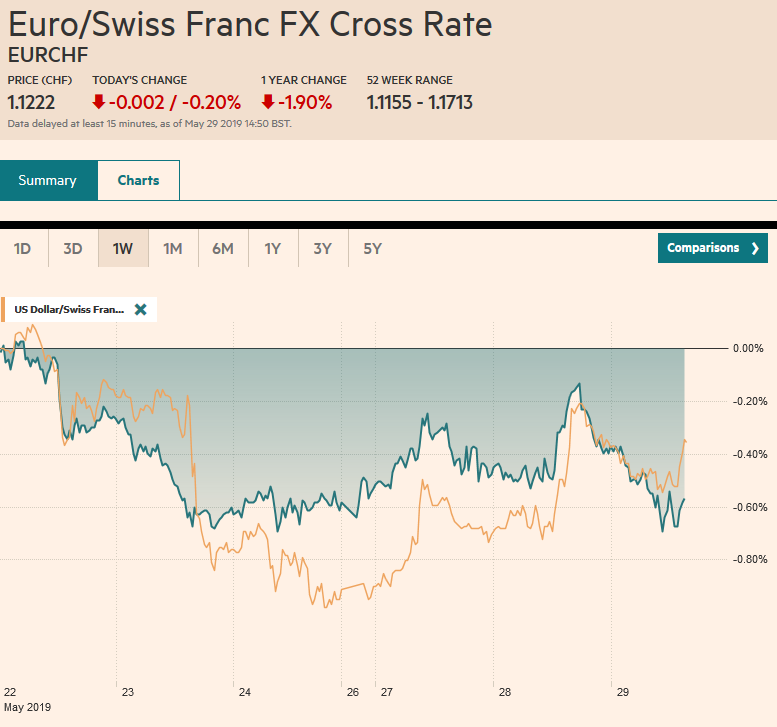

Swiss Franc The Euro has fallen by 0.20% at 1.1222 EUR/CHF and USD/CHF, May 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The slump in equities continues after the poor showing in the US yesterday. Nearly all bourses in Asia Pacific and Europe are lower. Indonesia is the notable exception as domestic operators re-position after the election. Foreign investors have been notable sellers of Korean and Taiwanese shares this month (in excess of .2 bln). Europe’s Dow Jones Stoxx 600 is testing its lowest levels since March, and the S&P 500 is poised to gap lower through the 2800-level that has offered support in recent weeks. The technical target we suggested

Topics:

Marc Chandler considers the following as important: 4) FX Trends, Bank of Canada, EMU, Featured, newsletter, trade, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.20% at 1.1222 |

EUR/CHF and USD/CHF, May 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The slump in equities continues after the poor showing in the US yesterday. Nearly all bourses in Asia Pacific and Europe are lower. Indonesia is the notable exception as domestic operators re-position after the election. Foreign investors have been notable sellers of Korean and Taiwanese shares this month (in excess of $6.2 bln). Europe’s Dow Jones Stoxx 600 is testing its lowest levels since March, and the S&P 500 is poised to gap lower through the 2800-level that has offered support in recent weeks. The technical target we suggested is in the 2700-2720 area. Meanwhile, bond yields continue to plunge. The US 10-year yield is near 2.22%, while 10-year German Bunds yield minus 16 bp and the 10-year JGB offers minus 10 bp. Spain and Portugal’s benchmark yields are off 4-5 bp. Italian yields are slightly lower. Australia’s 10-year yield is trading through the 1.50% cash rate. The dollar is firmer against most currencies, though the Swiss franc and Japanese yen are resisting also benefitting from the risk-over environment. The South African rand is leading the emerging market currencies lower. Concerns President Ramaphosa’s reform agenda will be compromised as the new cabinet appointments are awaited. The dollar’s move above ZAR14.75 is an inflection point. The high from last October near ZAR15.05 is the next important area. |

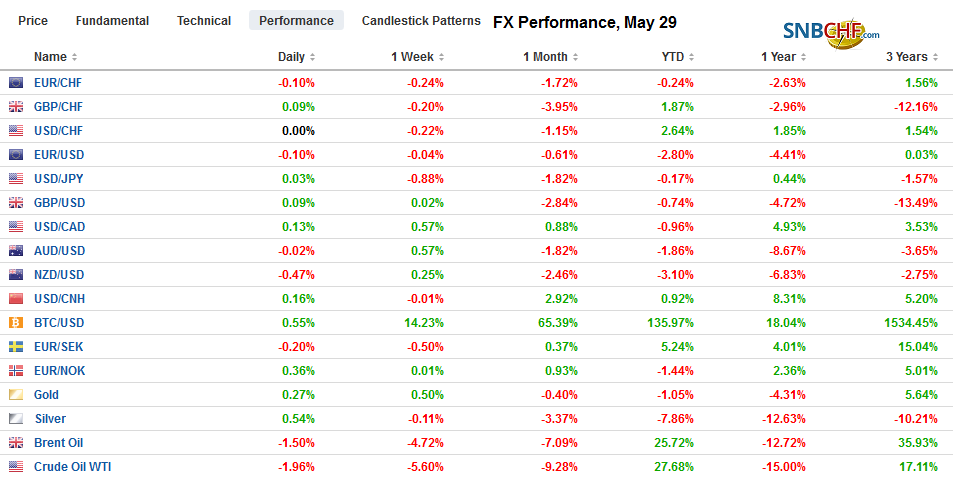

FX Performance, May 29 - Click to enlarge |

Asia Pacific

There continues to be much discussion about Chinese using its rare earths dominance to retaliate against the US. The National Development and Reform Commission (NDRC) suggested China was not on the verge of weaponizing these strategic minerals, indicating it would continue to meet world demand. Ominously, it noted that the Chinese people would not be happy if the rare earths are used to curb its development. The US has been careful not to put a new levy on the imported earths from China, which amount to about 4k tonnes last year at the cost of around $175 mln. China has put a 25% tariff on the one producer of rare earths that are exported to China for processing. Far and away, the most rare earths the US imports are embedded in a wide range of products. Owing to this, we have argued that it will be difficult for China to weaponize the rare earths without causing wider collateral damage. Meanwhile, China’s rhetoric is escalated. News wires are reporting the using an important Chinese phrase to the effect of “don’t say you weren’t warned.”

We had suggested that his public support, the stronger than expected Q1 GDP, and the fact that opposition in disarray, the Japanese Prime Minister Abe may be tempted to dissolve the lower chamber of the Diet and hold elections alongside the upper house elections slated for July. The election for the lower house is not required until October 2021. There is more discussion of this possibility in the press and among LDP officials. Time is not on Abe’s side. Whenever the retail sales tax increases, it has hit the economy. Although the government has taken some counter-measures, the risk is that tax hike in October weighs on weakens the economy again. In recent years, the lack of clear rivals in the LDP made Abe more secure. However, gradually Koizumi, the son of the former prime minister is beginning to draw attention as a potential candidate.

The dollar slipped to new two-and-a-half-week lows against the Japanese yen near JPY109.15. There is a $425 mln option at JPY109 and a $370 mln option at JPY108.75 that will be cut today. The JPY108.65 area is a (50%) retracement of the dollar’s recovery from the January 3 flash crash that saw the greenback drop below JPY105, while the low from late January was near JPY108.50. Looking ahead, there is a $1.3 bln option at JPY109 that expires tomorrow and a $1.4 bln at JPY108.50 on Friday. While the Australian dollar appears to have carved out a shelf near $0.6865, it now has failed for the fourth session to push above $0.6940. The Chinese yuan was virtually unchanged, though the off-shore yuan (CNH) weakened slightly for the second consecutive session.

Europe

The jockeying for position after the European Parliament election is nothing new, and the rhetoric around it and the differences should not be exaggerated. The European leaders agreed to have a six-person committee, two from each of the top three party groupings (center-right, center-left, and the Liberals) to begin the negotiating process with hopes of some preliminary agreements over the next month.

The strength of the German labor market has been a major prop for sentiment and hope of a recovery in H2. Today’s surprising jump in unemployment, the first in nearly two years raises new questions. The number of unemployed jumped by 60k. The median forecast in the Bloomberg survey was for an 8k decline. The Labor Office notes that around 2/3 of the increase was due to reclassification, but acknowledged that there was some genuine weakness. The unemployment rate rose to 5% from 4.9%.

Separately, France reported stronger than expected consumption in April. The 0.8% increase was twice what the median forecast (Bloomberg survey) expected. The news was marred by the downward revision to the March series from -0.1% to -0.3%. Still, the point is the resilience of the French consumer and the strong start to Q2. France also was the first to report May CPI figures ahead of the aggregate that will be reported a little ahead of next week’s ECB meeting. The harmonized measure of CPI rose 0.2% for a 1.1% year-over-year pace. This follows a 1.5% year-over-year increase in April. The decline in oil prices appears to be the main drag. This is expected to be representative of the region.

The euro is trading heavily. At $1.1150 it has met the (61.8%) retracement objective of the bounce seen at the end of last week. A convincing break signals a test on last week’s low, which is also an 18-month low near $1.11. There are large options struck there that expire today and Friday, which may make penetration difficult. Sterling is edging back to last week’s lows near $1.26. Below $1.2580 and the flash crash low around $1.2440 becomes the next major chart point though $1.25 may offer some psychological support.

America

The US Treasury widened the number of countries it reviews for their currency practices and eased part of the criteria, and despite Trump’s claims to the contrary, have again not found a single country guilt of manipulating its currency, including China, in its semi-annual report. The number of countries that meet at some of the criteria increased from six to nine. Five countries were added (Ireland, Italy, Vietnam, Singapore, and Malaysia) to the previous list that included China, Japan, Germany, and South Korea. India and Switzerland were removed from the watch list. No country has been named a currency manipulator since 1994.

The Bank of Canada meets today, and there is little doubt that policy is on hold, with the overnight rate at 1.75%. Many expect policy to remain on steady at least through the October election and possibly into next year. Separately, while there is much talk about who will replace Carney at the head of the ECB when he steps down early next year, the governing Liberal Party, which the polls say will lose in the national election, is talking about placing Trudeau with Carney, according to some press reports. The US dollar is pushing above CAD1.35 in Europe. Although the dollar has breached this level recently, it has been unable to close above it since the very start of the year. Some short-term players may go with the breakout if it moves above CAD1.3530.

Mexico’s central bank issues its inflation report today. It is likely to shave both growth and inflation forecasts. The risk-off mood is weighing on the peso. The dollar is poised to test this month’s high near MXN19.32. Above there, risk extends toward MXN19.50.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Bank of Canada,EMU,Featured,newsletter,Trade