There is a popular notion, at least among American libertarians and gold bugs. The idea is that people will one day “get woke”, and suddenly realize that the dollar is bad / unbacked / fiat / unsound / Ponzi / other countries don’t like it / . When they do, they will repudiate it. That is, sell all their dollars to buy consumer goods (i.e. hyperinflation), gold, and/or whatever other currency. Redemptions Balanced With Deposits No national currency is gold-backed today. In a gold backed currency, each currency unit begins life with someone who chooses to deposit his gold coin in exchange for the paper currency. And it ends life with someone redeeming the paper to get back the gold coin. A good analogy is bone in the

Topics:

Keith Weiner considers the following as important: 6) Gold and Austrian Economics, 6a) Gold & Bitcoin, Arbitrage, Basic Reports, dollar price, Featured, franc, Gold and its price, gold basis, Gold co-basis, gold price, gold silver ratio, negative interest, newsletter, silver basis, Silver co-basis, silver price, Swiss, zero interest

This could be interesting, too:

investrends.ch writes Lufthansa will zentralisieren – Swiss betont ihre Stärke

investrends.ch writes Swiss erwartet weiteren Druck auf den Gewinn

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

There is a popular notion, at least among American libertarians and gold bugs. The idea is that people will one day “get woke”, and suddenly realize that the dollar is bad / unbacked / fiat / unsound / Ponzi / other countries don’t like it / <insert favorite bugaboo here>. When they do, they will repudiate it. That is, sell all their dollars to buy consumer goods (i.e. hyperinflation), gold, and/or whatever other currency.

Redemptions Balanced With Deposits

No national currency is gold-backed today. In a gold backed currency, each currency unit begins life with someone who chooses to deposit his gold coin in exchange for the paper currency. And it ends life with someone redeeming the paper to get back the gold coin. A good analogy is bone in the human body. One process is constantly removing bone material. And another process is growing more. What seems to be a static bone, with fixed length and mass, is constantly being torn down and rebuilt. The seemingly stable bone is actually in equilibrium between two opposing forces.

So it is with the gold standard. Some people are redeeming paper to get the gold coin. Others are depositing gold coins to get paper. The seemingly stable gold standard is actually in equilibrium between two opposing processes.

We often hear that governments hate the gold standard because they cannot print gold. This is true, but there is another reason. When people don’t like the interest rate or the soundness of the banks, they withdraw their gold coin. What had seemed to be stable, is no longer. This has nothing to do with quantity of currency or gold. It has everything to do with honesty.

Thus our definition of inflation is not based on increase in quantity (or its assumed consequence, rising prices). Inflation is monetary counterfeiting. It is borrowing without means or intent to repay.

For some odd reason, people tend to want to pull their gold coins out of a bank that engages in this practice. It’s a real head-scratcher. Someone should write about this mystery…

Anyways, in the gold standard (i.e. in a free market for money and credit), people have a choice. They can deposit or redeem their deposits. It is never safe for the banks and the government to presume how people will choose.

In making once-redeemable currencies irredeemable, governments have disenfranchised the people. If you don’t like a bank deposit, perhaps because its interest rate is too low, you can withdraw irredeemable central bank notes. However, those notes pay zero. So you are out of the frying pan, and into the fire. Also, the central bank lends to the government and the banks. So its paper has the same risks.

Declaring Currency to be Gold Backed

Many people think that a government could make its irredeemable currency gold-backed once again. But this is like trying to make a dead bone, live again. The currency no longer has either process: deposits or redemptions. The government would be starting—in the best case—with a great gold hoard. It also has a vast quantity of paper currency, some of it productive and much of it counterfeit. And there’s no way for the people to differentiate.

Who would deposit gold into such a system?

Aside from that slight little problem, neither the government nor the banks quality to borrow gold today. They do not have a gold income, nor do business enterprises.

To declare a “gold standard” today, can only mean a gold price-fixing scheme. With no deposits—no willing depositors, and no productive purpose for a gold deposit and hence no interest on gold—it will be a one-sided process. There will be demand for gold by people who hold paper, but no corresponding demand for paper by people who own gold.

And this demand is not really redemption, as it does not extinguish a debt. All of the debt—from student loans and credit cards, to car and home mortgages, to business loans to bonds to accumulated welfare-state deficits—is denominated in the old irredeemable paper. None of these parties are suddenly paying their debts in gold (if you think lobbying in Washington or Brussels is bad now, just imagine if every debtor was going to be forced to pay their debts in gold!)

So this alleged gold standard has: no interest on gold, no deposits coming in, and is not using gold to extinguish any debts. It has only people trading their currency for gold. I.e. buying gold.

If the government sets a low price, then the people will buy all of its gold and it will run out. If it sets a price too high, then there will be no buying. And, of course, there is not a fixed “right” price of gold or anything else. The market clearing price moves for many reasons, not least of which is the endless dilution of the currency that represents good credit with more and more units of counterfeit currency.

Like all other central bank price-fixing schemes, such a “gold backed currency” would fail.

And this brings us back to the Swiss franc, which was the subject of a price-fixing scheme, to keep the value down to €0.83. This scheme failed spectacularly in January 2015. And it was doubly interesting, because if currency is printed as most people suppose, then there is no reason why the Swiss National Bank could not have continued printing.

The Mechanics of Currency Collapse

We said then, and again in our recent series of articles, that the franc will collapse.

Just as people won’t suddenly get woke to the dollar and repudiate it, they won’t with the franc either. That is not how it works. So last week, we promised to discuss how the franc could collapse. The currency is fraught with potential mechanisms.

One is the negative deposit rate. Currently, retail depositors do not pay. They get a rate of zero, and so they experience no reason to withdraw paper currency in preference to a bank deposit.

And arguably, corporations and institutions are far less equipped to hold paper cash. For one thing, the quantities are much larger. And corporate financial controls are usually not designed to deal with hundreds of millions or billions worth of paper.

So far so good, right? Not quite. There are two problems even so. Banks are losing on every retail deposit. 0 interest is far too high in a negative rates world. How much this is costing? Whether this, by itself, will cause a crisis is for someone else to analyze. We can only say that perpetual losses are not sustainable.

And the problem gets worse. Because, rates will resume their falling trend. So even if banks can afford a 75bps subsidy to retail depositors today, they cannot afford a 100bps or 150bps subsidy tomorrow. There is a line, somewhere, and it will be reached sooner or later.

Note that we are not saying that people will suddenly realize something. We are arguing mathematical inevitability that banks will have to charge negative interest to retail depositors.

When they do, then people have a reason to withdraw paper cash (cash is at 0%, which is better than negative). This will be a run on the bank. When the government made the currency irredeemable, the central planners thought they had ended the possibility of a systemic run (as opposed to a run on a single failing bank). But that is only true if interest rates are >= 0%.

“OK,” you say, “they can fix this by banning cash francs. Everyone will be issued a card and must use the card to debit and credit their accounts.” We will not address the sinister overtones of totalitarianism implicit in this idea. We will focus only on the economics.

First, let’s look at retail depositors. How is anyone supposed to achieve any savings goal whatsoever, if he is forfeiting 75bps a year (or more) due to negative interest charged by a Sisyphean banking system? It’s impossible. No matter how much you push up that franc-rock balance, negative interest will roll it back down.

All Swiss citizens who wish to accumulate savings will be forced to do so in another currency.

This is not a matter of getting woke. This is merely the struggle under a negative interest rate currency.

The people will be forced to sell francs and buy dollars (it will be dollars primarily, followed by gold). Not because they have any sudden monetary understanding. Not because they have any long-term view of the franc. Not because they intend to, or are aware of, a currency collapse. But simply to avoid their bank balance being rolled back by a vindictive Zeus.

“OK,” you say. “This may be in the future but it is not happening today.” This is true. But businesses are a different story.

We have already made the argument last week that they have an incentive to work out deals with their customers and vendors, to use dollars. So we will not dwell on this today. We have also argued that if a business can borrow money at negative interest then it can destroy capital while making a profit. If destroying capital is profitable, then it will be done at large scale. No currency (or economy) can survive this indefinitely.

And there is another business problem. Every business has an optimal mix of cash, current assets, and long term assets. Smart managers determine these levels and maintain accordingly. A negative interest rate necessarily skews this calculation. Everyone wants to avoid losses, so they will seek to minimize cash balances as much as possible. This will have several followon effects. One of them is obvious, that they incur greater risk due to lower cash balances.

Another is that businesses will become less liquid, and hence less flexible and less agile.

A third, is they will prefer for customers to pay later, rather than sooner. This flies in the face of thousands of years of commerce. But now there is a perverse incentive to want to be paid Net 90 rather than cash. So there will be a preference to extend credit to customers, to avoid being paid until there is an expense due. In other words, if Acme owes CHF1,000,000 on January 1, then it wants its customer to pay on January 1, and not sooner.

Or it would, all else being equal. Of course, extending terms adds to credit risk. So as with cash balances, this is not an automatic push-it-to-the-max. It will simply move the slider towards the direction of longer credit terms.

Will customers demand a discount to extend the payment deadline? It is logical…

Businesses will bid up the price of other assets, and hence push down the yields. Ignoring receivables which we just discussed, we have also looked at the cost of trading one’s francs for dollars, and buying a franc future. There is no escaping the fallout of negative rates. All assets will be covered in toxic radioactivity that drags down their yields.

Finally, let’s look at the concept of net present value and apply it to business liabilities. In a normal world, i.e. positive interest rates, a payment to be made or received in the future has a lower value than a payment today. The present value of a future payment is discounted by the market interest rate. So, for example, if the interest rate is 10% a payment of CHF100 in one years’ time is worth CHF90.91 today.

Our Old Friend: Net Present Value

But at zero interest, a future payment is worth its nominal value today. This, in itself, will cause collapse as all irredeemable debt is perpetual. The value of a perpetuity at zero interest is: infinite.

And just what the heck is the net present value of a future payment at negative interest rates? The math says it is higher in the present. In other words, at -10% interest, a payment of CHF100 next year is worth CHF111.11 today.

If falling interest rates is like falling into the gravity well of a black hole, negative rates is like being inside the mass of the object itself. The burden of debt rises until it crushes you.

And as we saw with customer credit above, there is a common sense way to understand this phenomena. You would rather someone owe you a fixed amount, than pay you. At least so long as his credit is good. Which the falling interest rate is impairing. Even if nothing else does it, the falling interest rate will destroy the ability of debtors to pay.

Defaults, a cascading series of failures to pay, where one party cannot pay and that stresses his creditor to the point of not paying, and so on, will destroy a currency eventually. That is our forecast for the franc.

We realize this is bleak. And that is why we write to warn the world of what’s coming. And why we pursue vision of paying interest on gold, which is the only path out of this impending catastrophe.

This Report was written from London. Also visiting Madrid, Zurich, Hong Kong, Singapore, Sydney, and Auckland. If you would like to meet, please contact us.

Supply and Demand FundamentalsThe price of gold went up seven bucks, and that of silver rose eight pennies. For many people, the attraction to gold and silver began with a desire to protect themselves from the monetary train wreck of 2008. That often grew into a sense that gold is the solution to that problem. Certainly, millions of people around the world are reaching towards gold for that reason. Possibly including the central bank of Hungary recently. That’s why it is important to say that betting on the price of gold is not a solution. Someone buys gold, another sells it. Dollars and gold change hands. Rinse, repeat. Nothing changes, much less is solved. Nevertheless, it’s something to do for fun and profit! Now let’s look at the only true picture of the supply and demand fundamentals of gold and silver. But, first, here is the chart of the prices of gold and silver. |

Gold and Silver Price(see more posts on gold price, silver price, ) - Click to enlarge |

| Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). It rose slightly this week. |

Gold:Silver Ratio(see more posts on gold silver ratio, ) - Click to enlarge |

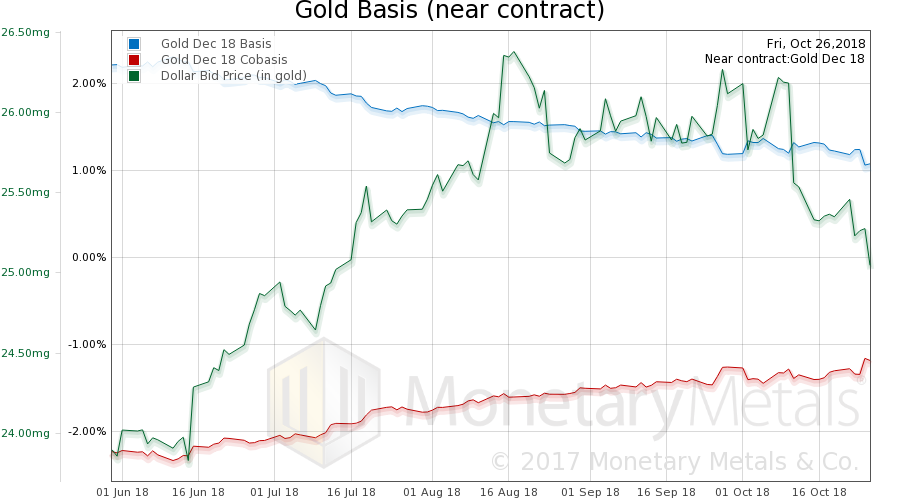

| Here is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price.

There’s something interesting about this graph, in light of the recently activated discussion: whether we have hit a bottom in the gold price, whether gold will go up as (if) stocks go down. Notice since late September (if not mid-August), the falling dollar (which is the reality of a rising gold price). And along with that is a slow but steady rise in the cobasis. According to the December cobasis (not so much the continuous cobasis) gold is becoming a bit scarcer at higher prices. It’s scarcer now at $1,230 than it was at $1,180. There has been buying of physical metal in the past few months. The Monetary Metals Gold Fundamental Price rose another $27, from $1,306 to $1,333. |

Gold Basis and Co-basis and the Dollar Price(see more posts on dollar price, gold basis, Gold co-basis, ) - Click to enlarge |

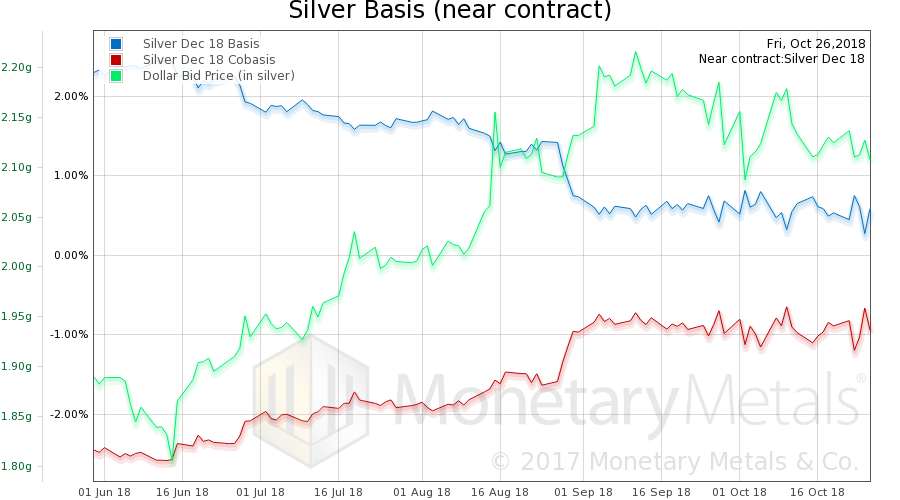

| Now let’s look at silver.

By contrast, the price action in silver has been more tepid, and the cobasis has gone sideways. The Monetary Metals Silver Fundamental Price dropped 11 cents, from $15.40 to $15.29. |

Silver Basis and Co-basis and the Dollar Price(see more posts on dollar price, silver basis, Silver co-basis, ) - Click to enlarge |

© 2018 Monetary Metals

Tags: Arbitrage,Basic Reports,dollar price,Featured,franc,gold basis,Gold co-basis,gold price,gold silver ratio,negative interest,newsletter,silver basis,Silver co-basis,silver price,swiss,zero interest