See the introduction and the video for the terms gold basis, co-basis, backwardation and contango. Explaining a new paradigm can be both simple and impossible at the same time. For example, Copernicus taught that the other planets and Sun do not revolve around the Earth. He said that all the planets revolve around the Sun, including Earth. It isn’t hard to say, and it isn’t especially hard to grasp. Indeed, one of its virtues was making the universe simpler. In the old geocentric model, there is the phenomenon of so called retrograde motion—the planets appear to stop moving forward in their orbits, and move backwards temporarily. It’s difficult to describe mathematically, and worse, no one could explain the cause.

Topics:

Keith Weiner considers the following as important: 6a) Gold & Bitcoin, Basic Reports, capital destruction, Dollar, dollar price, falling interest, Featured, gold basis, Gold co-basis, gold price, gold silver ratio, inflation, Money, new paradigm, newsletter, Real interest rate, reset, silver basis, Silver co-basis, silver price

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

See the introduction and the video for the terms gold basis, co-basis, backwardation and contango.

Explaining a new paradigm can be both simple and impossible at the same time. For example, Copernicus taught that the other planets and Sun do not revolve around the Earth. He said that all the planets revolve around the Sun, including Earth. It isn’t hard to say, and it isn’t especially hard to grasp.

Indeed, one of its virtues was making the universe simpler. In the old geocentric model, there is the phenomenon of so called retrograde motion—the planets appear to stop moving forward in their orbits, and move backwards temporarily. It’s difficult to describe mathematically, and worse, no one could explain the cause.

The hard part of accepting this paradigm shift, was that people had to rethink their entire view of cosmology, theology, and philosophy. In the best case, people take time to grapple with these challenges to their idea of man’s place in the universe. Some never accept the new idea.

Rising Prices Aren’t Intrinsic to the Currency

It is the same with money. The prevailing paradigm—the dollar-centric view—is akin to the Medieval geocentric view. This view is characterized by two premises. One, the dollar is money. And two, the value of money is not defined in terms of gold (which is believed to be just a commodity like oil or wheat). The value of money is defined as the inverse of the general price level. This means: what you can buy is intrinsic to the currency.

We can see this point in action, in almost any article about Venezuela. Nicolás Maduro, their corrupt and inept dictator, has destroyed production of just about everything. And he has rendered it impossible to import or distribute what little they still have. Consumer goods are truly scarce, so of course prices are skyrocketing. But people call this inflation or hyperinflation.

They accept that what you can buy is a property of the currency itself, missing that in Venezuela you can’t buy anything anymore, because of the socialist dictatorship.

Everyone knows that the dollar loses value. The Federal Reserve’s target is to make the dollar lose 2 percent per annum. The dollar goes down, and this is not a bug but a feature.

The Unit of Account

Being money, the dollar is therefore the unit of account. However, this contradicts the fact that the dollar goes down. A unit has to be stable, to be useful to measure anything. So how do people reconcile this contradiction? The dollar is the unit of account, but the dollar is constantly shrinking—i.e. it fails as a unit.

Their answer is to try to measure money in terms of prices. They add up the price of apples, oranges, petrol, rent, etc. And they use this consumer price index to define the value of money. They claim to measure the purchasing power of money. Remember that prices are measured in money. So measuring money in terms of prices is circular reasoning.

Anyways, purchasing power enables them to perform a neat trick. It informs them what the exchange rate of two currencies ought to be, based on so called purchasing power parity (PPP). PPP is the exchange rate at which you could trade your dollar for euros or yuan, and buy the same amount of goods in these currencies as you could with your dollar. We would not recommend trading the FX markets based on this notion.

We wonder if they use the purchasing power of the Yuma, AZ dollar or the midtown Manhattan dollar. The former has five to ten times as much power contained inside of it!

We are joking, but there is a serious point. The price you pay for your coffee and breakfast eggs with sausage is obviously dependent on the value of the currency. But it’s also dependent on a whole lot of nonmonetary factors, such as the cost of getting supplies into a dense city on an island. And of course regulations and compliance, taxes and fees, zoning, labor law, building code, etc. It is less expensive—it costs fewer real resources—to operate a store on East Palo Verde Street than it does on Lexington Avenue.

Is the Dollar Money

Now we examine that first premise. Is the dollar money? Consider the gold standard we once had. You could bring a twenty dollar bill to a bank, push it across the counter, and the teller would give you a gold coin. If the world for the paper bank note is “money”, then what is the word for the gold coin?

Since them, the dollar has been made irredeemable. Americans could not redeem their paper bank notes after President Roosevelt’s infamous decree in 1933. Foreign central banks could not redeem theirs after President Nixon’s equally infamous decree in 1971. Now it’s irredeemable, but does that change it into money?

At the recent Sprott Resources Conference, Grant Williams said that gold is the only commodity that does not go no bid. In times of crisis, ordinary things go no bid. Who would make a bid on real estate in Los Angeles if the U.S. Geological Survey said an earthquake is coming, 15 on the Richter scale, and nothing taller than a dollhouse will be left standing? There would be plenty of offers to sell real estate, but no bid to buy.

Why should gold be different? The answer is, “well it just is.” Needless to say, this is not satisfactory.

This is the monetary equivalent of retrograde motion in the Medieval geocentric view of the planets. Why do the planets reverse direction in their orbits? They just do.

In the paradigm shift we propose—that gold is money—there are no special cases. All things go no bid in a crisis. The key to this simplicity is to understand that gold is money. Money is the thing which is either bidding or not bidding.

When that crisis comes, the dollar will go no bid (but today is not that day). When we realize gold is money, then we no longer have this bit of “retrograde no bid” in need of an explanation.

The Glaringly Evident

The challenge to accepting the new paradigm is that it forces you to reexamine everything. The downside, if you don’t, is you can be blind to serious problems that should be glaringly evident.

It is glaringly evident that interest rates have fallen relentlessly since 1981. This is a serious problem Young people, deprived of interest and hence compounding, despair of ever being able to save for retirement. With banks cutting interest on accounts to nearly zero, one may as well dream of walking on the moon as having a few million dollars at age 65—both are equally unobtainable.

However, in our observation, the finance and economics mainstream don’t really acknowledge the long-term trend of falling interest rates. How is this possible?

The bond price moves inversely to the interest rate. A falling rate is the same thing as a rising bond price. A falling interest rate trend is the same thing as a bond bull market.

The Yin and Yang of a Bond Bull Market

A bull market!

Who could be against a bull market? A bull market is what the mainstream acknowledges. And by a process of arbitrage, a bull market in bonds induces a bull market in other assets including stocks and real estate.

A bull market is a positive spin on the epic collapse of interest.

Meanwhile, armed with the same dollar-centric paradigm, critics of the Fed scramble for traction. They keep saying that the government lies, and understates inflation in the Consumer Price Index.

The more mainstream folks in the liberty movement disagree. They point to the new iPhone, which admittedly is very cool, or the fact that Amazon ships your stuff even faster. To us, this sounds like Dug the Dog saying “squirrel!”

So some creative dollar-thinkers have discovered a new way to measure the dollar. No, not gold. Never that! We have actually seen people argue that the value of the dollar is the inverse of the stock market! 1 / P is out. Now it’s 1 / S&P.

They are struggling to explain an apparent paradox. If the Fed’s newly printed money isn’t going into consumer goods, then where is it going? It must be going into assets.

Not even Ptolemy’s geocentric model got this complicated. So let’s move away from this dead-end of monetary science. We have a much simpler idea.

Capital is Getting Scarcer

Capital assets really have gone up since 1981.

And let’s think about that for a minute. What is it about rising prices? What is it about Venezuela? Oh, right, prices are rising. When something becomes scarce, the price rises. And capital has been getting scarcer since 1981.

We write a lot about the destruction of capital, as the salient process of our system. For people to destroy their capital is a perverse outcome. It is a response to the perverse incentive of falling interest rates.

If capital is being destroyed, then wouldn’t capital assets becomes scarcer? If we see rising prices, isn’t that evidence of growing scarcity?

Theory predicts capital destruction as a consequence of falling interest rates. Theory also predicts rising prices as a consequence of increasing scarcity. And we have long had both falling interest and rising asset prices.

John Maynard Keynes, citing Vladimir Lenin, said that debauching the currency, “engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.” There is a reason why not one in a million can diagnose it.

The reason is that the other 999,999 believe the dollar to be money. They think that the measure of the value of the money is 1 / P. So they first look at consumer prices, but get frustrated that prices aren’t rising as they expect (especially commodities). Then they turn to asset prices and they think they have found the answer.

Real Interest Rates

As an aside, if the value of money is 1 / P, then then that means:

real interest rate = nominal interest rate – inflation

In the dollar-centric paradigm, interest is adjusted by inflation. So people who believe this will say “sure, nominal interest was much higher in 1981, but so was inflation.” We have published the graph of real interest rates before, suffice to say that the so called real rate is also falling. So not only are many people blind to the epic collapse of the actual interest rate at which actual lenders actually lend to actual borrowers—which they dismiss as nominal. They also miss the fact that this so-called real interest rate is falling too.

If you borrow $1,000,000 at 5% interest, then you really must pay $50,000 a year. That is real.

Monetary Paradigm Reset

Anyways, it is not that they are stupid. Most people are not stupid. The problem is that they are stuck in a false paradigm, which blinds them to the truth. The pre-Copernicus astronomy Medievals were stuck thinking that planets moved forwards in their orbits, punctuated by some backward motion. And today’s dollar Medievals are stuck thinking that the dollar is devalued by its quantity, and this devaluation can be seen in the prices, if not of consumer goods, then of capital assets.

The single most important issue of our era is the monetary paradigm reset, as people move away from the generally accepted dollar-centric paradigm, to the correct gold-centric paradigm.

Supply and Demand Fundamentals

Shh, don’t tell the dollar-paradigm folks that the dollar went up 0.2mg gold this week. Or if that hasn’t blown your mind, the dollar went up 0.01 grams of silver.

It’s less-uncomfortable to say that gold went down $10, and silver fell $0.08. It doesn’t force anyone to confront their deeply-held beliefs about money. But it does have its own Medieval retrograde motion to explain.

How the #$%&! could gold possibly be going down?!?

Next week, we will dive deeper into some analysis of what could be driving gold down in recent months.

In the meantime, let’s just say that we observe two facts. One, the market price of gold has been coming down since the second half of April. It has dropped about $135 since then. Two, our calculated fundamental price, based on the basis, had been rising through late April. Since then, it has come down about $220.

Whatever the cause may be, something real has happened. It is up to market participants to deal with it. Or else they can trade their money for Federal Reserve Notes, in the belief that this would eliminate all risk…

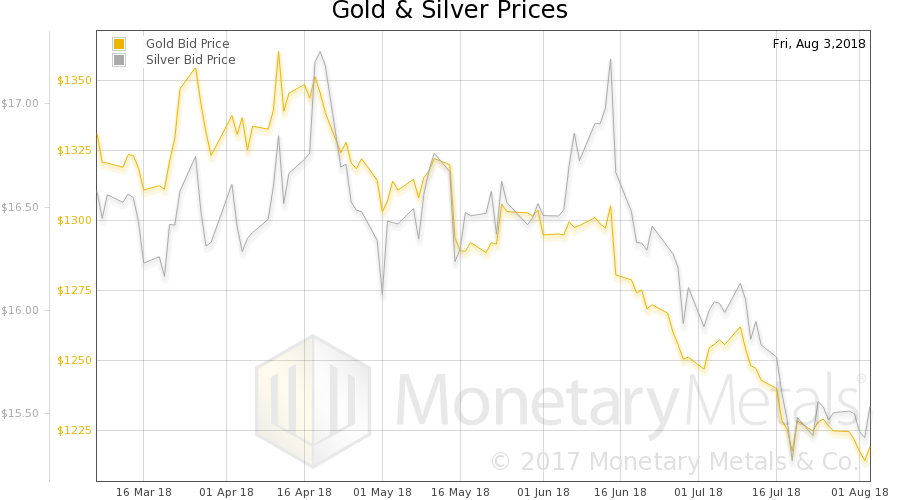

| We will look at an updated picture of the supply and demand picture. But first, here is the chart of the prices of gold and silver. |

Gold and Silver Price(see more posts on gold price, silver price, ) - Click to enlarge |

| Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio (see here for an explanation of bid and offer prices for the ratio). It fell a hair week. |

Gold:Silver Ratio(see more posts on gold silver ratio, ) - Click to enlarge |

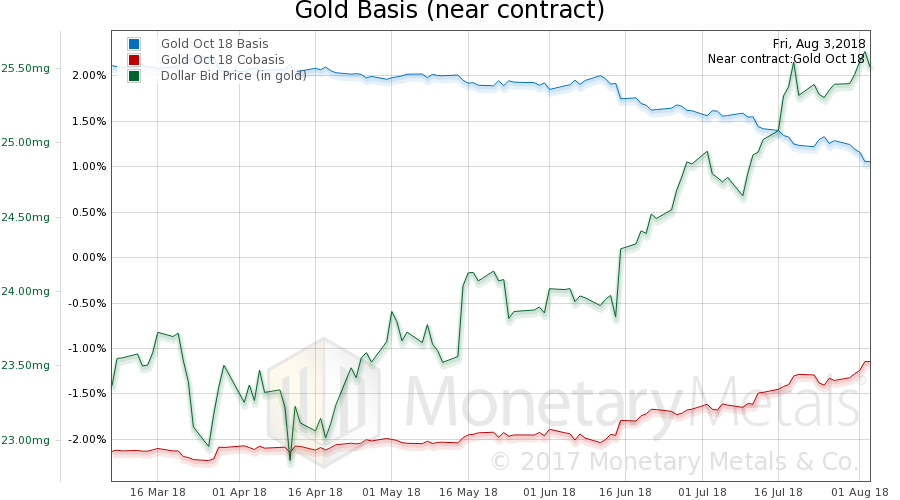

| Here is the gold graph showing gold basis, cobasis and the price of the dollar in terms of gold price.

As the price of the dollar moved up this week (we don’t need to say that this means the price of gold, measured in dollars, fell do we?) we see a little bit of rising scarcity in the cobasis for the October contract. However, that is not true for farther-out contracts. The Monetary Metals Gold Fundamental Price went down another $5 this week to $1,304. |

Gold Basis and Co-basis and the Dollar Price(see more posts on dollar price, gold basis, Gold co-basis, ) - Click to enlarge |

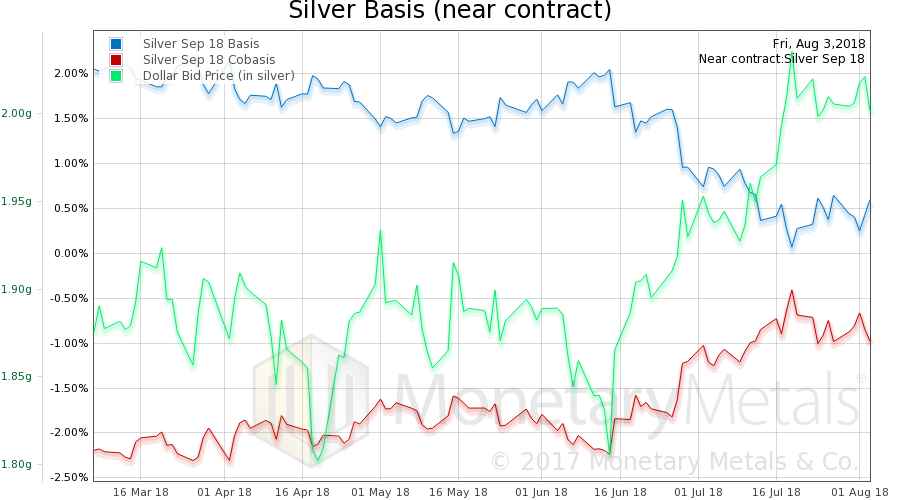

| Now let’s look at silver.

In silver, the near contract shows no change in scarcity. It’s not all that surprising, given that the price didn’t move much. However, it’s somewhat surprising as the near contract happens to be September and we are nearing First Notice Day. There is already selling pressure on this contract, which will tend to push its price down and hence its basis down and cobasis up (basis = future – spot, and cobasis = spot – future). Basically (OK, pun intended) September silver basis and cobasis show nuthin’. The further contracts show falling cobasis (scarcity) and rising basis (abundance). Even as the price dropped a few pennies. |

Silver Basis and Co-basis and the Dollar Price(see more posts on dollar price, silver basis, Silver co-basis, ) - Click to enlarge |

The Monetary Metals Silver Fundamental Price fell another 20 cents, to $16.52.

© 2018 Monetary Metals

Tags: Basic Reports,capital destruction,dollar,dollar price,falling interest,Featured,gold basis,Gold co-basis,gold price,gold silver ratio,inflation,money,new paradigm,newsletter,Real interest rate,reset,silver basis,Silver co-basis,silver price