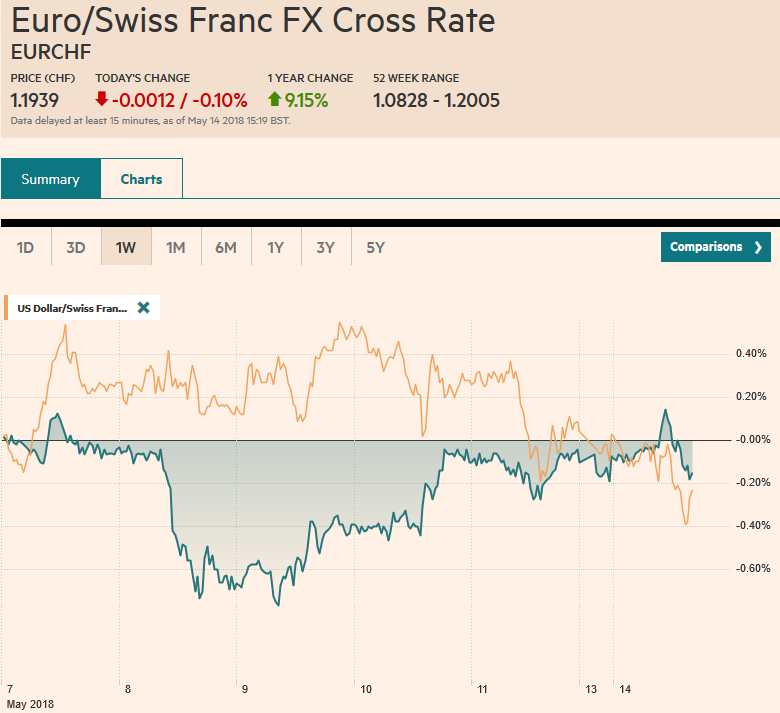

Swiss Franc The Euro has fallen by 0.10% to 1.1939 CHF. EUR/CHF and USD/CHF, May 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The US dollar is sporting a softer profile against most of the major and emerging market currencies to start the new week. It already seemed to be tiring in the second half of last week. With today’s mild losses, Dollar Index is off for a fourth consecutive session, the longest losing streak in over a month. The US and China appear to have taken measure to diffuse the trade tensions between the world’s two largest economies. The US is reversing itself on sanctions imposed on China’s ZTE that had appeared to threaten its future. China

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, EUR/CHF, Featured, GBP, Japan Producer Price Index, JPY, newslettersent, TLT, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has fallen by 0.10% to 1.1939 CHF. |

EUR/CHF and USD/CHF, May 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

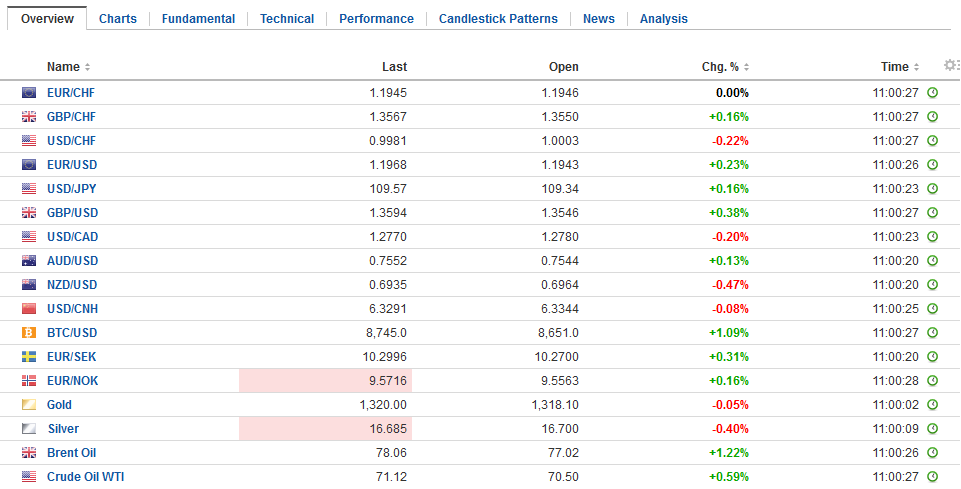

FX RatesThe US dollar is sporting a softer profile against most of the major and emerging market currencies to start the new week. It already seemed to be tiring in the second half of last week. With today’s mild losses, Dollar Index is off for a fourth consecutive session, the longest losing streak in over a month. The US and China appear to have taken measure to diffuse the trade tensions between the world’s two largest economies. The US is reversing itself on sanctions imposed on China’s ZTE that had appeared to threaten its future. China indicated it will launch a review of Qualcomm’s application to acquire NXP Semiconductor. This is ahead of the Chinese trade delegation coming to Washington for talks starting tomorrow. |

FX Daily Rates, May 14 - Click to enlarge |

| Malaysian markets re-opened for the first time since last week’s election surprise. The NDFs had sold off, but when the onshore market resumed business, the ringgit recovered and managed to close fractionally higher. The stock market rose 0.2%, recovering fully from the slide suggested by offshore ETF trading. It benefited from the regional advance. The MSCI Asia Pacific Index rose nearly 0.5%, its third consecutive gain and five of the past six sessions. The index of H-shares that trade in Hong Kong led the regional advance with a 1.6% gain, followed by the Hang Seng itself (1.35%). The Nikkei matched the regional index performance and reached its best level since early February. Separately, note that the MSCI Emerging Markets Index is up 0.25% to extend its advance for a sixth session. It is the longest streak since the 11-day run in January.

European shares are trading a little heavier. The Dow Jones Stoxx 600 is off nearly 0.2%. After a sharp run-up since the end of March, the index hit a fall last week just above 390.00. It has been trading in a narrow range a little above there. Today is the fourth such session. As the market appears to have largely shrugged off the outcome of the Malaysian election, so too it is the market largely ignoring the likelihood of a new Italian government composed of the Five Star Movement and the League. |

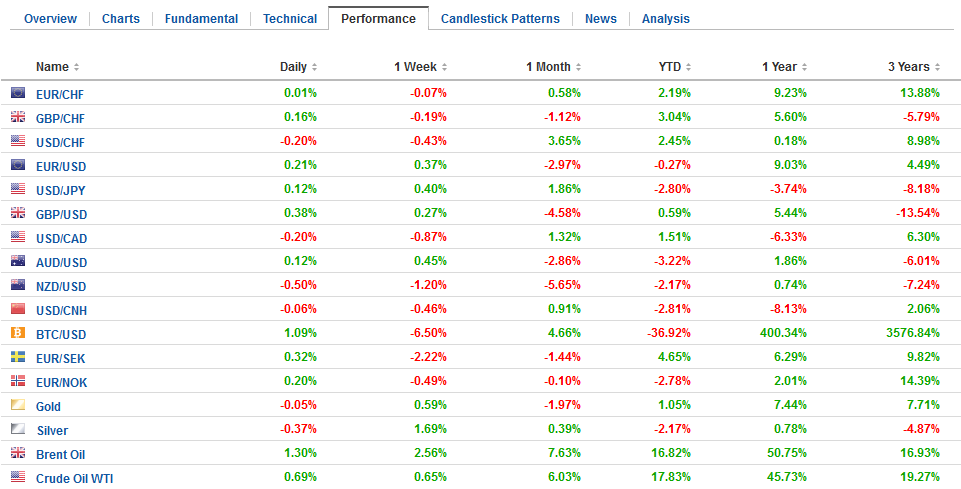

FX Performance, May 14 - Click to enlarge |

JapanThe yen and the New Zealand dollar are the only majors not gaining on the dollar today. The Kiwi continues to lag following the central bank’s dovish posture. The dollar has tried pushing through the JPY110 twice in the past fortnight. The near-term range is clear JPY108.65-JPY110.00. There is a large $1.3 bln dollar option struck at JPY110 that expires today. The $1.1 bln struck at JPY108.65 expiring today seems less relevant. The $395 mln struck at JPY109.25 also may more interesting. |

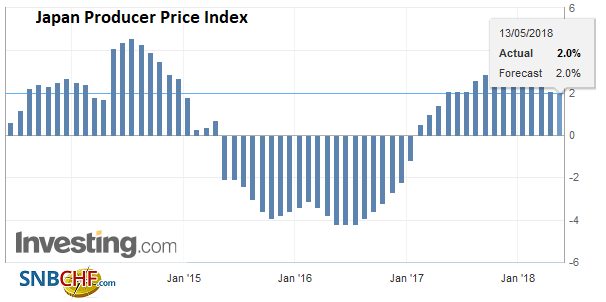

Japan Producer Price Index (PPI) YoY, Jun 2013 - May 2018(see more posts on Japan Producer Price Index, ) Source: Investing.com - Click to enlarge |

Italian shares are off slightly, though the bourse’s 10.4% gain this year is easily the best in the G7. Italian bond yields are higher today but in line with the increase in yields throughout the region. The yield of Italy’s 10-year benchmark has risen five basis points to poke above 1.90%. Spain’s benchmark yield is up a bit more ant 1.31%, while German and French 10-year benchmark yields are up about four basis points.

The broad strokes of the new government’s agenda have been indicated in the press to include a flat tax of 15% (though 20% for incomes above some 80k euros), basic income that seems like unemployment insurance, and unwinding pensions from 2011 that increased the retirement age. The program is likely to clash with the EU, but that is for another day. Ideas that both the Five Star Movement and the League have softened their direct confrontation over the euro or membership in EMU appears to be offering some consolation presently. Meanwhile, the two parties apparently are still debating over who to support for the next Prime Minister.

Over the weekend, the German construction sector settled the wage negotiations. Following earlier deals among metal workers and public sector employees, the 800k-strong construction union agreed on a six percent pay raise, retroactive from the start of the month. While the tight-fisted budget is a source of frustration for many of Germany’s partners, the high wage settlements is a helpful offset.

The euro is the strongest of the majors today, rising to almost $1.20 in late morning turnover in Europe. There is a 563 mln euro option struck at $1.20 that expires today. The $1.2020 area corresponds to the 200-day moving average, and the 38.2% retracement of the decline since the April 17 high (~$1.2415) is near $1.2050. We note that in the futures market, speculators have added to the gross long euro position for the past two weeks and for four of the past five weeks. There has been no capitulation.

Sterling is rising for the second consecutive session. It has not had back-to-back gains since the middle of April. It continues to chop around its trough. It has not closed above $1.36 since breaking below there on May 1. It must get above, and ideally close above $1.3620 to lift the technical tone and signal potential toward $1.3775-$1.3800.

The Australian dollar is consolidating the recent gains that lifted it from almost $0.7400 on May 9 to $0.7565 at the end of last week. There are sizeable options that expire at $0.7500 today and the next couple of sessions. Today, there are A$1.9 bln and tomorrow another A$1.7 bln and Wednesday an option for A$1.2 bln expires. The technical indicators are constructive. A move above $0.7565-$0.7575 could signal scope for another cent advance. The US dollar’s bounce after mixed Canadian jobs data before the weekend ran out of steam near CAD1.2800. The technical indicators seem to favor Canada and initial support for the US dollar is seen near CAD1.2730.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,Featured,Japan Producer Price Index,newslettersent,USD/CHF