Summary: Provided Le Pen and Macron or Fillion make to the second round, the market response to the French election results may be short lived. BOJ, Riksbank and ECB meetings. Spending authorization and some announcement from the White House on tax policy are in focus as Trump’s 100th day in office approaches. The results of the French presidential election will be known prior to the open of the Asian session. No doubt the outcome will spur an initial knee-jerk reaction, but barring an outright victory for Le Pen, which seems highly unlikely, or the left candidate Melenchon coming in second place, which also seems improbable, the market’s reaction will likely be short-lived. While there is, of course, a certain amount of anxiety, especially given the electoral surprises over the past year, investment community seems not overly worried. Large speculators in the currency futures have been amassing what Bloomberg calculates as a record large long euro position. The premium investors demand over Germany is elevated but has not accelerated as the election drew near. Very quickly after the election results are known, the market’s attention will turn to the French parliamentary elections in June.

Topics:

Marc Chandler considers the following as important: EUR, Featured, France, FX Trends, GBP, Italy, JPY, newsletter, U.K., US, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Summary:

Provided Le Pen and Macron or Fillion make to the second round, the market response to the French election results may be short lived.

BOJ, Riksbank and ECB meetings.

Spending authorization and some announcement from the White House on tax policy are in focus as Trump’s 100th day in office approaches.

The results of the French presidential election will be known prior to the open of the Asian session. No doubt the outcome will spur an initial knee-jerk reaction, but barring an outright victory for Le Pen, which seems highly unlikely, or the left candidate Melenchon coming in second place, which also seems improbable, the market’s reaction will likely be short-lived.

While there is, of course, a certain amount of anxiety, especially given the electoral surprises over the past year, investment community seems not overly worried. Large speculators in the currency futures have been amassing what Bloomberg calculates as a record large long euro position. The premium investors demand over Germany is elevated but has not accelerated as the election drew near.

Very quickly after the election results are known, the market’s attention will turn to the French parliamentary elections in June.Neither of the top two presidential candidates, Macron, and Le Pen, have a presentation in the current French parliament. They will need other parties’ support, and the configuration of parliament is just as crucial as the president, if not more so, for French policy going forward vis a vis the EU and EMU.

Many seem to be treating the recently announced UK election as a foregone conclusion. The Tories will increase their majority. While it seems true in a narrow sense, it may be politically naive. The Tory Party, after all, is a coalition. Doesn’t the impact of the election results depend on which Tories win? Some observers linked sterling rally on the announcement to ideas that it could produce a softer Brexit. That seems to be to assume what one must prove. Couldn’t soft Brexit Labour MPs be replaced by harder-line Tories?

Before getting to the national election, local elections will be held on May 4. English, Welsh, and Scottish councils will be chosen, as will the newly created English Regional Mayors. Labour goes into the contest with the most council seats overall (1535 vs. 1136 for the Tories). The results will be scrutinized to see clues into the national contest. A significant loss for Labour, as some are predicting, will likely spur talk of Corbyn stepping down, and demoralize and further weaken the main opposition party.

Not yet on many radar screens, and yet potentially of great importance, is the open primary for Italy’s ruling PD (April 30). Recall the fact that the primary was set in April spurred a fissure in the coalition that makes up the party and the spinning off of part of the left-wing split off. It had accused Renzi of taking the party to far to the right. We have warned that Italy’s election next year may be more of a threat to the EU and EMU than this year’s Dutch, French and German contests.

The outcome of the primary will determine who face the Five-Star Movement (M5S). The PD and M5S are in a statistic draw at the moment. Renzi is likely to win the PD primary, but anything but an overwhelming victory bodes poorly. It will also be important to see if Renzi shifts to the left or tries to peel votes from the M5S.

Fitch reduced its credit rating of Italy to BBB before the weekend from BBB+. There is unlikely to be much material impact. Fitch’s rating had been higher than the other rating agencies that the ECB uses to set terms of loans it makes. Fitch’s rating is now at the same level as Moody’s and DBRS. This is the lowest level of investment grade. Standard and Poor’s is more aggressive and sets it at BBB-.

With a large debt burden, little meaningful progress in reducing it, not to mention a banking sector burdened by bad loans and a challenging profit environment, the risk of losing its investment grade status has increased. A loss of its investment grade status would mean that, without getting on a support program–and the loss of sovereignty that implies–Italian sovereign bonds would no longer be acceptable collateral, which would further squeeze Italian banks. Perhaps, the potential loss of Italy’s investment grade status over the next 18 months is a significantly underappreciated financial stability risk. If it were to happen before next year’s election, it would make for the explosive political climate.

The US political drama is likely to intensify. Congress returns from its two-week recess, and there is expected to be a flurry of announcement about intentions and plans as President Trump’s 100th day in office approaches (April 29). There are three issues, the most important of which is the federal government’s current spending authorization (as opposed to funding it, which relates to the debt ceiling, for which the Treasury Department has already taken steps to minimize the disruption while waiting for Congress to lift it) expires on April 28.

The other two issues, health care reform, and tax reform are not as pressing, and there have been conflicting signals from the White House and Congress. Ahead of the 100th-day anniversary, there was some suggestion that a new vote on replacing the Affordable Care Act could be held, but this seems unlikely. The Freedom Caucus and the Tuesday Group may have been talking, but there is a fundamentally different set of interests. The split also is evident in discussions about tax reform. Around mid-week, President Trump indicated there would be an announcement on tax reform. It is difficult to envision more than a wish list at this juncture. Recently, Treasury Secretary Mnuchin pushed out expectations for tax reform from the August recess to the end of the year.

Trump is right, as was Obama, the 100-day bogey is of little significance. It is the next 1000 days that are important. As a campaign device, Trump had offered a “contract with the American voter” over what he would do in his first hundred days. The importance attached to the fact that practically nothing outside of some executive orders has been achieved beyond the scope of this analysis. However, the important point for investors is that many market participants appear to have downgraded the chances that Trump’s legislative agenda will be delivered, and this seems to be an important factor in what the media has dubbed the unwinding of “Trump trade.”

It is not the media, which the White House says it is at war with, whose judgments are key. The 2018 midterm elections loom on the horizon yet are very present. There is only so much that can be accomplished by executive orders that more the most part call for an investigation of this, or a check on that or study there. A stymied legislative program could weaken the Republican hold of both the House of Representatives and the Senate. This would force the White House to work with the Democrats if it were to pass legislation.

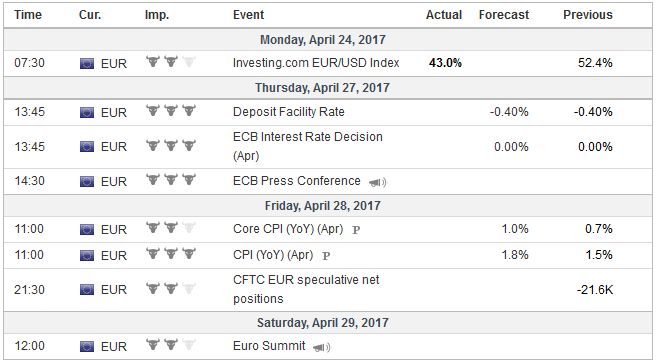

EurozoneThe ECB meets next week. The March meeting elicited a hawkish response from the market. Draghi is likely to try to ensure a more dovish message is heard. His pre-weekend comments sketched his views. He continues to see downside risks to growth and no evidence that inflation is on a rising trend. Draghi reiterated that he anticipates rates will “remain at present or lower levels,” for an extended period. While no policy change is expected, there is scope to adjust the securities lending program to ease pressure on the repo market. Sweden’s Riksbank meets and policy is likely to remain on hold. Its asset purchase program in on track to end in June. The past rise in energy prices may spur the Riksbank to lift its inflation forecast. Ahead of the weekend, the euro make new highs for the year against the Swedish krona. On a trade-weighted basis, the krona has weakened by about 2.5% over the past month. The economic data highlights include the flash HICP measure of inflation for the eurozone and the US and UK initial estimates for Q1 GDP. The eurozone inflation is expected to have ticked up in April after falling in March. The Easter holiday is generating some noise, but Draghi’s assessment seems fair. The headline rate is expected to rise to 1.7% from 1.5%. The core rate can rise to 0.9% from 0.7%. It averaged 0.9% in 2016 and 0.8% in 2014 and 2015. |

Economic Events: Eurozone, Week April 24 - Click to enlarge |

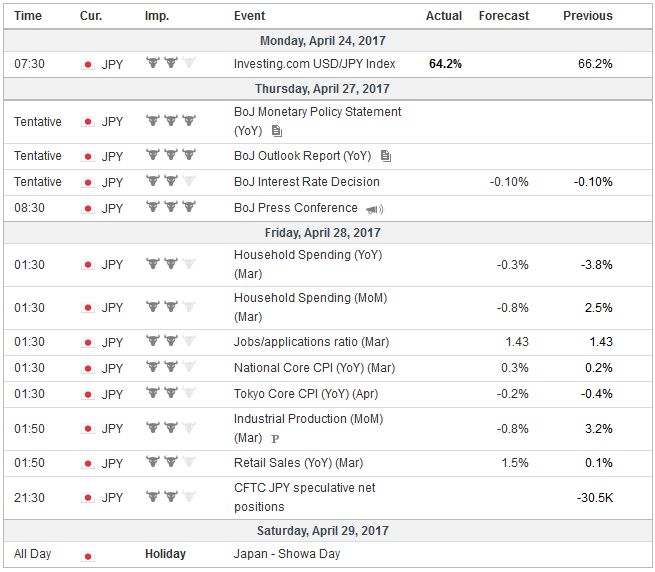

JapanThe Bank of Japan will maintain it current policy stance, and the focus is on its updated economic projections. it will issue its report on Economic Activity and Prices. In January, the BOJ projected that core inflation, which excludes fresh food, will rise 1.5% this fiscal year that began at the start of the month. The core rate had risen by 0.2% in the 12-months through February. It seems to be more an exercise of hope that compelling analysis. The expected inflation on breakevens (6-10-year) is 0.42% and 0.48%. The FY18 inflation forecast stands at 1.7%, and the central bank anticipates FY19 to be near the 2.0%. The take away from what seems like unrealistic forecasts are the signal that the BOJ remains committed to its unorthodox policies. |

Economic Events: Japan, Week April 24 - Click to enlarge |

United KingdomThe UK is expected to have grown around 0.4% in Q1, decelerating from 0.7% in Q4 16. It has averaged 0.5% over the past four, eight and 20 quarters. The market impact is likely to be marginal. The dismal March retail sales report failed to spur a serious pullback in the sterling. Sterling’s sharp advance seemed more about positioning, and the prospects of a softer Brexit, and reduced risk of no agreement rather than economic support. The 10-year gilt yield is hovering a little above 1.0%, the lows since last October. A convincing break gives immediate potential to 90-95 basis points. Similarly, the implied yield of December short-sterling future is near 40 bp, which is also near the least in six months. It has fallen around 15 bp over the past month and is just below the 200-day moving average. |

Economic Events: United Kingdom, Week April 24 - Click to enlarge |

United StatesThe median forecast in the Bloomberg survey puts Q1 US growth at 2.0% annualized. We think the risk of disappointment is palpable, but outside of a knee-jerk reaction, we do not see it impacting the Fed’s forward-looking decision in June. Consumers took the quarter off it would seem after a strong 3.5% rise in Q4. It is difficult to see the other sectors that will offset the pullback in consumption. Still, with income and savings increasing in Q1, and the distortions caused by the warmer weather and lower utility consumption, recession fears are likely exaggerated. For reasons that are not particularly clear, the US economy has typically underperformed in the January-March period since the Great Financial Crisis ended. |

Economic Events: United States, Week April 24 - Click to enlarge |

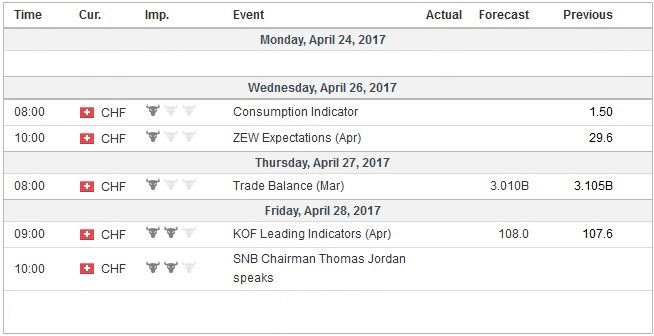

Switzerland |

Economic Events: Switzerland, Week April 24 - Click to enlarge |

Germany |

Economic Events: Germany, Week April 24 - Click to enlarge |

Tags: #GBP,#USD,$EUR,$JPY,Featured,France,Italy,newsletter,U.K.,US