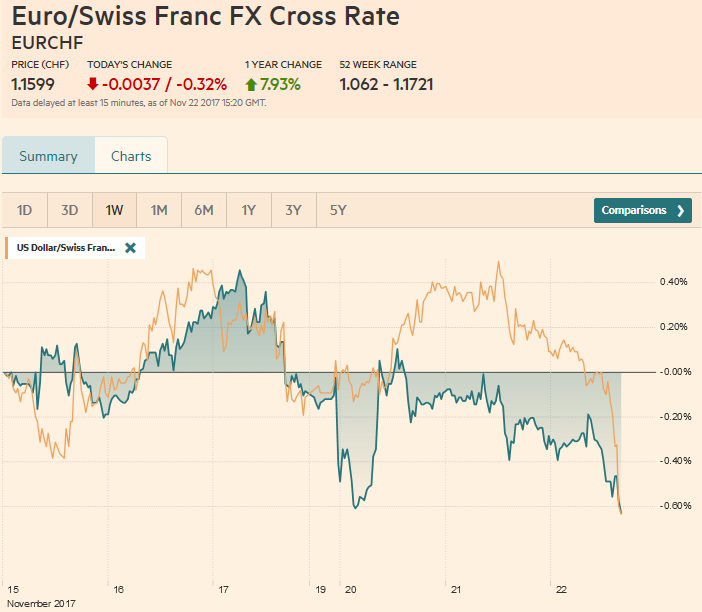

Swiss Franc The Euro has fallen by 0.32% to 1.1599 CHF. EUR/CHF and USD/CHF, November 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Global equities are on the march. US indices shrugged off their first back-to-back weekly decline in three months to set new record highs yesterday. The MSCI Asia-Pacific followed suit and recorded their highest close. The Dow Jones Stoxx 600 is struggling, as the CAC and DAX are nursing small losses. The synchronized global upturn and prospects for continued abundance of liquidity appear to be underpinning sentiment. At a speech in NY late yesterday, Yellen warned against raising rates too quickly and repeated her sense of mystery

Topics:

Marc Chandler considers the following as important: AUD, equities, Featured, Federal Reserve, FX Trends, newslettersent, U.S. Initial Jobless Claims, U.S. Michigan Consumer Sentiment, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has fallen by 0.32% to 1.1599 CHF. |

EUR/CHF and USD/CHF, November 22(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesGlobal equities are on the march. US indices shrugged off their first back-to-back weekly decline in three months to set new record highs yesterday. The MSCI Asia-Pacific followed suit and recorded their highest close. The Dow Jones Stoxx 600 is struggling, as the CAC and DAX are nursing small losses. The synchronized global upturn and prospects for continued abundance of liquidity appear to be underpinning sentiment. At a speech in NY late yesterday, Yellen warned against raising rates too quickly and repeated her sense of mystery over the decline in inflation this year. The US two-year yield softened marginally, and the Fed funds futures rose. At 1.295%, the implied yield of the December Fed funds futures contract is precisely at what we think is fair value assuming a rate hike at the next FOMC meeting. |

FX Daily Rates, November 22 - Click to enlarge |

| There seems to be some confusion over what Yellen means, though she may very well be the most plain-speaking Fed Chair. She is not referring to structural influences. She is referring to the recent decline. Specifically, core CPI fell from 2.3% in January to 1.7%, where it was from May through September before ticking up to 1.8%. The targeted core PCE deflator fell from 1.91% last October to 1.30% in August before rising to 1.33% in September. It is this decline she regards as mysterious but sticks to the working hypothesis that the decline is due to a number of idiosyncratic factors.

Some reports play Yellen’s dovish warning but also accused her of being too hawkish when the Fed last hiked rates in June. Others suspect that her caution against raising interest rates too fast is a signal to her successors at the Fed. Still, others are linking her dovish comments to the risk that the minutes from last months’ FOMC meeting that will be released this afternoon will show some officials concerned about an undershoot of unemployment. Recently there has been some evidence of greater wage increase for employees in some sectors, including what are regarded as blue-collar occupations. |

FX Performance, November 22 - Click to enlarge |

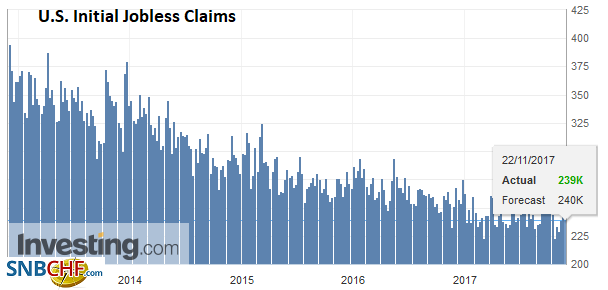

The United StatesThe US reports weekly initial jobless claims and durable goods orders. |

U.S. Initial Jobless Claims, Oct 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

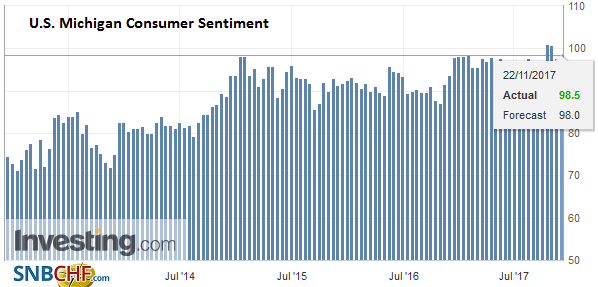

| The latter is unlikely to maintain the strength seen in September, but another solid report excluding transportation equipment is expected (0.5% vs. 0.7% in September). University of Michigan’s Consumer Sentiment survey with its inflation expectations will also be reported. The FOMC minutes are late in the session and will be released in thin market conditions ahead of tomorrow’s US holiday. |

U.S. Michigan Consumer Sentiment, Nov 2017(see more posts on U.S. Michigan Consumer Sentiment, ) Source: Investing.com - Click to enlarge |

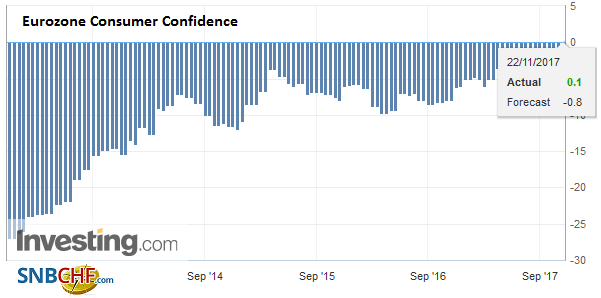

Eurozone |

Eurozone Consumer Confidence, Nov 2017(see more posts on Eurozone Consumer Confidence, ) Source: investing.com - Click to enlarge |

The main event today, however, is in the UK as Chancellor of the Exchequer Hammond delivers his Autumn Budget to parliament. There is much pressure on Hammond to deliver. Former Prime Minister Cameron thought a referendum on the EU would resolve the conflict that was ripping apart the Tory Party. Rather than resolve it, the referendum nationalized it, and the Tories lost their parliamentary majority. The markets may be particularly sensitive to the new forecasts by the OBR. The poor productivity record means weaker growth prospects, which in turn eat away at latitude to provide much fiscal succor. There continues to be the talk of a cabinet reshuffle.

Brexit remains very much front and center. While the UK appears to be signaling concessions on the European Court of Justice to protect the rights of EU citizens after Brexit and is willing to pay more than Prime Minister May initially proposed, it is balking at addressing the Irish border in any fashion. Instead, it continues to insist that the border can only be resolved in the talks about the new trade relationship. Ironically, some officials seemed to have previously thought that a strong Merkel after the election, perhaps tempered by the FDP, would be good for the UK. Now a weakened Merkel is seen as a boon.

Germany’s political outlook is far from clear. After consulting with the German President, the FDP refuses to renew coalition talks. The only other potentially viable alternative is to woo back the SPD. The head of the SPD Schulz has ruled it out; he is not the party. A survey suggested less than half of the SPD favor Schulz to run again for Chancellor after his disappointing campaign. In the CDU, Merkel is supported by 78% to run again. Outside of the left-wing of the SPD which supports Schulz, the SPD may be more frightened by the prospect of another election. It had hoped that a few years in opposition would allow it to rebuild its base. An election now could see its fortunes fall further, and if it were to get less than one in five votes, an existential question would be raised.

On the other hand, joining another Grand Coalition could also put the future of the party at risk. Moreover, it is not clear that the CDU and SPD would be sufficient. Both parties drew the least voters in a generation and together are now polling a little more than 51% vs. 53.4% in September. One scenario has the SPD placing strong demands to re-join. However, one European policy there does not appear to be a significant difference, and on domestic policies, Merkel has often stolen their thunder (e.g., minimum wage and greater daycare provisions).

Elsewhere, the Australian dollar posted a bullish key reversal yesterday, but the lack of follow-through buying today is disappointing. Construction jumped 15.7% in Q3 after an upwardly revised 9.8% (from 9.3%) in Q2. Even this did not help. The construction report was flattered by the LNG facility being imported. The weakness in renovations seemed to local investors more important than the 6% rise in public infrastructure. The Australian dollar met offers in front of $0.7600 and returned to $0.7555 before finding a bid. The recent drip lower in Australia’s two-year yield and increase in the US means that the Australia’s rate is poised to fall below the US for the first time since 2000.

The latest round of NAFTA negotiations concluded. Some progress was reported on telecom, digital trade, and sanitary rules. However, Lighthizer made it clear that the US remained frustrated with the lack of serious engagement in key areas. The hardest issues are also addressed last. There are four areas for which little progress has been seen: domestic content (autos), dairy, dispute panels, government contracts, and the US insistence on a sunset provision (though in public some US officials talk about “periodic reviews”).

There is some chunky option expires to note. There is a 970 mln euro option stuck at $1.750 that will be cut today. There are options (688 mln euros and 825 mln euros) struck at $1.17 and 1.18 respectively. There is a $1.4 bln option struck at JPY112.00 that expires today. Sterling has a strike at $1.3250 for GBP280 mln. Lastly, there is a $980 mln option struck at CAD1.2780 that will be cut today.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$AUD,equities,Featured,Federal Reserve,newslettersent,U.S. Initial Jobless Claims,U.S. Michigan Consumer Sentiment