Italy is big enough to matter (it is the eight largest economy on the planet), but so uneventful that most does not pay any attention to what is going on there. We contend that Italy will, during the next year or two, be on everyone’s radar screen as it has the potential to derail the European project for real. Greece, Portugal and Ireland were mere test subjects for what will come. Spain would have been a challenge, but were narrowly avoided. Italy will drag the whole structure down if it continues on its current trajectory, and there is nothing to suggest it will change course. The main problem for Italy is its stagnating level of nominal GDP, which we refer to as “Japanificaton” of the economy. While people usually think of deflation when they hear “Japan”, that is not an entirely correct observation. It is true that nominal GDP flat lined after the crisis in the 1990s which dragged down revenue. However, if it was truly a deflationary period, expenditures should fall also as prices paid for services rendered would drop concomitantly. This has not been the case and it is more correct to say Japan has been trapped in a revenue / NGDP deflation, hence the perceived need for Abenomics, or in plain English, the creation of a helluva lot of currency units to boost NGDP and revenue and thus reduce the need for bond issuance.

Topics:

Eugen von Böhm Bawerk considers the following as important: Banking, Bawerk, Economics, Europe, Featured, Finance, Japan, newsletter, Politics, Regulation

This could be interesting, too:

Investec writes The Swiss houses that must be demolished

Claudio Grass writes The Case Against Fordism

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Italy is big enough to matter (it is the eight largest economy on the planet), but so uneventful that most does not pay any attention to what is going on there. We contend that Italy will, during the next year or two, be on everyone’s radar screen as it has the potential to derail the European project for real.

Greece, Portugal and Ireland were mere test subjects for what will come. Spain would have been a challenge, but were narrowly avoided. Italy will drag the whole structure down if it continues on its current trajectory, and there is nothing to suggest it will change course.

The main problem for Italy is its stagnating level of nominal GDP, which we refer to as “Japanificaton” of the economy. While people usually think of deflation when they hear “Japan”, that is not an entirely correct observation. It is true that nominal GDP flat lined after the crisis in the 1990s which dragged down revenue. However, if it was truly a deflationary period, expenditures should fall also as prices paid for services rendered would drop concomitantly. This has not been the case and it is more correct to say Japan has been trapped in a revenue / NGDP deflation, hence the perceived need for Abenomics, or in plain English, the creation of a helluva lot of currency units to boost NGDP and revenue and thus reduce the need for bond issuance. As our first chart show, so far it has been modestly successful. Please note that Abenomics have nothing to do with creating real prosperity (no one can be that ignorant), but all about getting the spiraling debt problem under control by jacking up the inflation tax.

Italy is now more or less in the same situation with tax revenue struggling to keep up with current expenditures, id est government consumption. Investments, which can be lowered today without immediate consequences suffer and are now, nominally, at the same level they were in the early 1980s. When revenue flat lines, due to lack of investments, and current expenditures keep rising the shortfall is made up for by debt issuance. The gaping hole between future prospects (a function of bad decisions in the past) and flat lining revenues is fiendishly difficult to plug as it require large sacrifices today, without any payout for years to come.

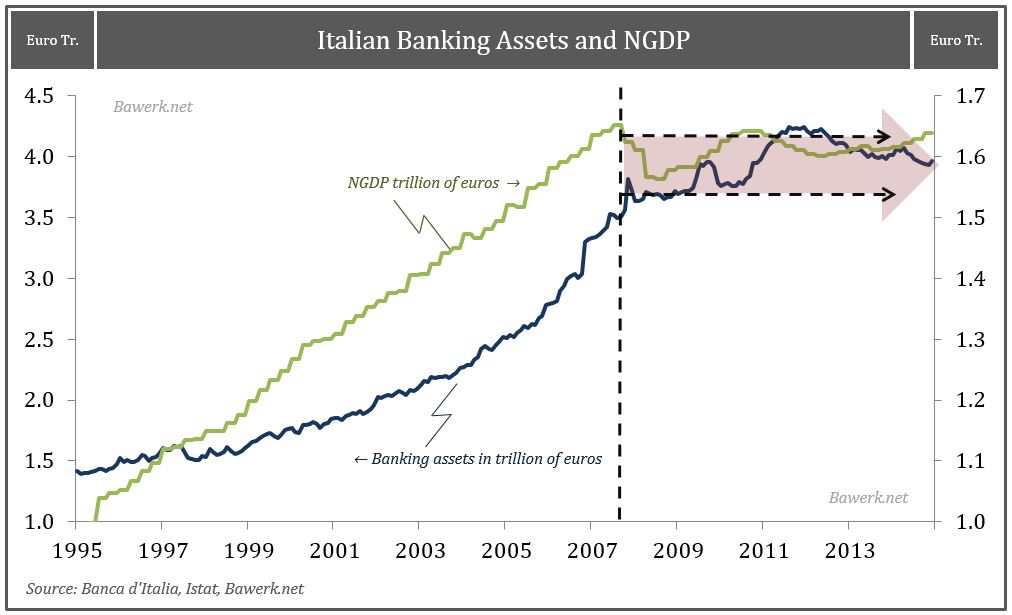

Just as in Japan, Italy is trapped with stagnating nominal GDP versus ever growing debt levels used to pay for current expenditures enshrined into law and politically enforced by an ageing population with a feeling of entitlement. As our next chart shows, there is a sense of inevitability baked into the Italian cake. We all know a day of reckoning will come because the current trajectory is, put bluntly, unsustainable. Something will have to give as the Italian state, just as the Japanese one, uses household savings to fund state consumption while giving the populace the sense of investing their money for the future. In other words, Italian households put their money in the bank or in public pension funds, which is used to fund current retirees, but expected to provide a cash flow for their own retirement. The circularity here is obvious to anyone willing to look. There are NO savings, they are only visible on balance sheet statements, but are so far removed from what constitutes real productive investments as possible.

As productive investments are sucked dry by an ever expanding state and its incessant need to fund current expenditures there is very little the banks can do to spur investments and underpin growth. It is no coincidence that banks assets flat lines alongside nominal GDP. They are both closely interlinked and as banks find no customers willing or able to borrow money and invest, they naturally scale back and so the money supply growth grinds to a halt, either through a falling money multiplier and/or through falling velocity. Either way, nominal GDP stops expanding, while the insatiable need for public spending keeps public debt rising relentlessly.

Note that every action taken by central banks until just recently has been an act, be it ZIRP, forward guidance or QE, to manipulate demand for credit, which obviously failed miserably due to the balance sheet constraints prevalent in both the private as well as public sector. In order to alleviate this, negative interest rates is designed to force supply onto a hapless public by making it too expensive for banks to maintain excess reserves at the central bank. Needless to say, this is a doomed policy to begin with. If there are no credit worthy borrowers willing to borrow money, then forcing banks to push credit to a non-worthy or non-willing public is sheer lunacy; but the desperate need to create NGDP growth runs so deep that it trumps common sense. In this sense it is interesting to note that the sectors with positive loan growth, after the ECB has gone all in, is exactly the unproductive sectors that should deleverage and free up resources to the productive sector. Alas, this is not what is happening.

It should thus come as no surprise that Italian investments are falling behind it’s, admittedly lackluster, peers. According to Eurostat Italian gross investment are lower today than they were in the mid-1990s. Knowing that a capital base depreciate around 20 per cent annually, we would not be surprised to learn that the Italian capital stock is in terminal decline as the current structure of production and Italian consumption pattern cannot be sustained without actually consuming the capital stock.

One piece of evidence substantiating our claim is the fact that labour productivity is falling in Italy. If capital per worker is falling, as it would in a situation where, through depreciation, capital is consumed, one should expect lower output per worker. This is exactly what has been going on for the last 15 years. The process accelerated as investment peaked and fell after the GFC, just as we would expect it to do.

Since policymakers identify the problem as lack of credit, completely missing the point that credit cannot be given to a person, but is something that person already have, policies are naturally focused on increasing credit and by extension money supply and consequently inflation/NGDP. Focus has therefore shifted from what could by now be called conventional monetary policy tools such as QE and liquidity injections through TLTROs to one of negative interest rates and bad debts.

Italian banks are officially swamped with €200bn worth of non-performing loans, while unofficial estimates put it as high as €350bn. At €200bn, it is growing at double digits per year and constitutes more than 12 per cent of NGDP. Non-performing loans in the non-financial corporate part of the portfolio is close to 18 per cent.

While this obviously has to be dealt with somehow, the focus now is for the bad debts to be cleansed from banks balance sheets so they can start to lend money again, which is just an euphemism for creating credit, inflation and “growth”.

The Italian government presented a plan in January that underwhelmed markets as they were essentially constrained by EU regulation on state aid to come up with something that would benefit Italian banks (on behalf of the Italian tax payer we presume). In addition, a clear cut bail-out now comes with new strings attached, essentially forcing bail-in of debt holders and unsecured depositors before any state aid can be handed directly to banks.

So how will the problem eventually be dealt with? We got a clear hint during Draghi’s testimony to the European Parliament when he told his audience that NPLs can be added to asset backed securities which would then be eligible for the ongoing ECB QE program. This would be a win-win situation for the money masters as the ongoing QE program, unlike earlier ECB interventions, actually remove credit risk from banks balance sheets. In addition more ABSs would alleviate the shortage of securities the ECB is currently struggling with. Frankfurt is thus frenetically looking for additional assets to buy in order to avoid the BoJ trap. As of today, less than 5 per cent of Italian banking assets are securitized, while simultaneously ECB’s Asset-Backed Security Program is the least successful with only €18bn purchased so far, compared to €155bn in the third Covered Bond program and almost €600bn in the Public-Sector purchase program.

The underlying solvency issue is obviously not solved by this trickery as credit risk is just moved from the private banking industry to the public sector. And this tells us what is probably glaringly obvious to all, including the men and women in charge, that the only thing that can truly lead to positive change is a real crisis. Only then can we honestly deal with reality through debt write-downs, re-alignment of consumption with production and end the sense of entitlement. The electorate, politicians and most of the bureaucrats running Italy and Europe will always opt for the extend-and-pretend option as long as it is available to them; this is especially true when they have dug themselves so deep into troubles that there are no pleasant way out. In other words, change, real change, will not come until it is absolutely necessary, forced upon them by the ultimate monetary end-game.

While it is true that monetizing bad assets may initially be perceived as the way out for Italy, as banks can once again expand their balance sheet and in the process kick start nominal GDP and get the debt to GDP ratio under control, the fact is more ominous – Italy is a train crash in slow motion. Italian consumption outstrips production, and it has done so for years. The capital base is being eroded, labour productivity is falling (and we haven’t even touched upon its dire demographic situation) and living standards stagnating. The only thing that keeps this thing running is its ability to roll-over and issue debt.

They got dangerously close to being shut out of that window in 2012, and since then nothing has changed. Italy still needs to roll over bonds worth 25 per cent of GDP per year and the slightest hiccup will bankrupt them in no-time. The key is obviously a “healthy” banking system willing and able to keep buying newly issued bonds as old retire.

With debt to GDP ratios over 100 per cent of GDP the interest rate sensitivity grows exponentially. As average interest paid on outstanding debt rose a meagre 40 basis points during the Euro Crisis of 2012, interest expenses as share of GDP rose 80 basis points. And back then, the ECB managed to rid the Italian treasury from roll-over risk quickly enough to save them. Next time, when the Central Bank narrative has changed from one of omnipotence to one of failure they may not be so lucky. If we assume Italian interest rates were at it is 2000 – 05 average of 4.8 per cent, they would today pay 6.5 per cent of their GDP in interest only.

When Italy finally succumbs to reality, this year or next, the European project as they call it will face insurmountable hurdles and collapse on itself. In our view, seeing the parasitical edifice in Brussels disappear can only lead to good things. Maybe the Brits will save us the agony and end it June 23rd. One can only hope.

Appendix – Bonus Charts