Swiss Economicblogs.org

Swiss Economicblogs.org

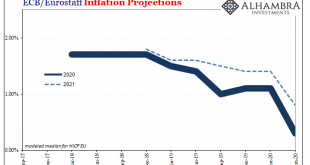

A perpetual motion machine is impossible, but what about a perpetual inflation machine? This is supposed to be the printing press and central banks are, they like to say, putting it to good and heavy use. But never the inflation by which to confirm it. So round and round we go. The printing press necessary to bring about consumer price acceleration, only the lack of consumer price acceleration dictates the need for more of the printing press. It never ends. If you...

Read More »ECB Doubles Its QE; Or, The More Central Banks Do The Worse You Know It Will Be