The Lords of Easy Money: How the Federal Reserve Broke the American Economy by Christopher Leonard Simon and Schuster, 2022 viii + 373 pp. Christopher Leonard’s book brings to mind the familiar line from Faust: “Two souls, alas! dwell in my breast.” Leonard offers a penetrating criticism of the Fed’s vast expansion of the money supply, which has won for him praise from the noted hard-money advocate and friend of the Mises Institute James Grant. Leonard is a well-known journalist and has engaged in extensive research on the Fed, in particular on the papers of Thomas Hoenig, for many years vice president of the Federal Reserve Bank of Kansas City, and the extensive notes in the book show how assiduous he has been in his research. Why, then, do I suggest with my

Topics:

David Gordon considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The Lords of Easy Money: How the Federal Reserve Broke the American Economy

by Christopher Leonard

Simon and Schuster, 2022

viii + 373 pp.

Christopher Leonard’s book brings to mind the familiar line from Faust: “Two souls, alas! dwell in my breast.” Leonard offers a penetrating criticism of the Fed’s vast expansion of the money supply, which has won for him praise from the noted hard-money advocate and friend of the Mises Institute James Grant. Leonard is a well-known journalist and has engaged in extensive research on the Fed, in particular on the papers of Thomas Hoenig, for many years vice president of the Federal Reserve Bank of Kansas City, and the extensive notes in the book show how assiduous he has been in his research.

Why, then, do I suggest with my opening quotation that there is a problem with the book? We can best answer this question by asking another question: What is wrong with the Fed’s inflationist policy? Two responses immediately suggest themselves. Both are correct, and both are endorsed by Leonard. First, inflation disrupts the economy, in particular causing business cycles through bank credit expansion, and the possibility of hyperinflation and the collapse of the monetary system can never be dismissed. Second, efforts by the Fed to revive the economy through inflation usually wind up giving large subventions to rich people whose firms are bailed out because they are “too big to fail.” The Fed thus widens the gap between the rich and the poor

But if both of these answers are right, and both are stressed by Leonard, our question recurs: Why is there a problem with the book? The answer, I suggest, is that Leonard sometimes overemphasizes the second answer at the expense of the first. Sometimes, though fortunately not always, he seems to be suggesting that a government-controlled economy, so long as the “people” through a democratic election support it, is perfectly all right. The real menace is that the rich “fat cats” run monetary policy to their advantage and the common people’s detriment.

Speaking of the New Deal, he says: “The largest burst of fiscal action in U.S. history happened after the Great Depression and the election of Franklin Delano Roosevelt in 1932. Over the following decade, Roosevelt and a Congress with huge Democratic majorities passed a set of sweeping and interlocking laws that came to be known collectively as the New Deal. This is important to consider because of the effect it had on the economy and its arrangement of winners and losers. The New Deal laws empowered labor unions, broke up or regulated big monopolies, created the first transparency laws for Wall Street, and put the banking system on a tight leash. The New Deal was confrontational. It antagonized powerful interests, and it took away their power.”

For Leonard, “fiscal policy” is highly desirable, and the increase of the Fed’s power is bad because it reduces the importance of government spending in controlling the economy. “On one side of the divide there is monetary policy, controlled by the Federal Reserve. On the other side, there is fiscal policy, which belongs to the democratically controlled institutions like Congress, the White House, and state governments. Fiscal policy involves the collection of taxes, the spending of public money, and regulation. America’s ability to conduct fiscal policy deteriorated slowly over the years as the Fed’s ability to conduct monetary policy strengthened. . . . But the one important fact about the deterioration of executive and legislative power is that it was not inevitable. For at least a century or so, fiscal policy led the way in America, and the Fed, with its money- printing power, followed.” It is clear that Leonard longs for a return to those palmary days.

Despite this failing, Leonard’s book contains many insights, and it is easy to see why James Grant praises it. One of the most important of these insights comes from Hoenig, who served on the Federal Open Market Committee (FOMC), which sets targets for the short-term interest rate, under Alan Greenspan and Ben Bernanke. Hoenig favored a restrained course of action, urging “that the Fed should focus on both of the inflation cousins, asset inflation and price inflation. It was true that detecting out-of-control asset inflation was more difficult than detecting price 10 | The Austrian | Vol. 8, No. 3 inflation. And asset inflation was harder to stop without disrupting markets and making prices fall. But the results of asset inflation were devastating. When asset prices eventually corrected, and they always did, it caused massive financial instability.”

This point is especially valuable in response to critics of the Austrian theory of the business cycle, who in past years have said to us, “Where are the rising prices that you say an expansionary monetary policy generates? You have for years predicted disaster, but the boom continues with prices that remain relatively stable.” Paul Krugman and others of his ilk directed such inquiries to us in mocking tones, and they are sufficiently answered by Leonard; the effects of expansion appear in asset inflation. But of late, as prices rise rapidly, the mockers laugh at us no more. Gone are the days when the insanities of Modern Monetary Theory were solemnly treated as live options.

Hoenig’s warning about asset price inflation was set within a larger context. The Fed should take account of “long and variable lags,” rather than act only to cope with a perceived emergency. Expanding the money supply may temporarily avoid a crash, but the long run should not be ignored. This warning is better than nothing, but it misses the fundamental point that the Austrian school emphasizes. The depression is the corrective phase of the business cycle, and the government should allow the market to liquidate the malinvestments caused by bank credit expansion. Of this neither Hoenig nor Leonard has a glimmering.

The limitations of Hoenig’s approach are evident in his reaction to Fed policy during the 2008 crash. Despite it being seemingly contrary to his principles, he supported the Fed’s vast expansion of the money supply. After all, when faced with a sufficiently great emergency, the Fed must act! As Leonard explains, “During the bailouts of 2008, the Fed printed nearly $875 billion. It more than doubled the monetary base in a matter of months …. In just a few months after the stock market crash of September, the Fed’s balance sheet grew by $1.35 trillion, more than doubling the assets it already had on its books. All of this was done with the understanding that these were emergency actions, an extraordinary attempt to confront an extraordinary danger. The financial panic of 2008 threatened to plunge the global economy into a deep depression. . . . The Fed stepped in, as it had been designed to do, and short-circuited the panic. Tom Hoenig voted to support each and every one of these actions when they were presented to the FOMC in a series of emergency meetings. He believed that this was the Fed’s job.”

Hoenig’s differences with Bernanke’s Fed came later. The Fed’s “quantitative easing” continued even though the emergency had passed. Even though Bernanke and his colleagues were well aware of the consequences, it was too difficult for the Fed to end the policy, as doing so would lead to setbacks for those who had come to rely on the Fed’s largesse. Here Hoenig drew the line.

Hoenig is the book’s hero, but he is matched with an antihero. “Jay Powell entered this debate from a position that was quite close to Tom Hoenig’s. Both gave voice to the idea that the Fed was a highly imperfect engine to drive economic growth in America. Hoenig’s critiques drew from his decades of experience at the Fed. Powell’s critiques drew on his decades of experience in private equity, and he used hard data and interviews with his industry contacts to make his critique of QE both specific and alarming. Both men warned about the way that the Fed was stoking asset bubbles as it chased relatively small gains in the labor market. But this was where the similarities ended between Powell and Tom Hoenig. Powell, for all his critiques, never cast a dissenting vote. And Powell, unlike Hoenig, started to soften his criticism, and he ultimately came to embrace the policies he once criticized inside the FOMC’s closed meetings. When this happened, Powell’s star began to rise.” In brief, Powell sold out for “power and pelf,” as Murray Rothbard used to say.

Leonard has depicted very well the Fed’s policy of reckless monetary expansion. But we should not, as he wants, deal with this policy by requiring the Fed to follow strict rules and by subjecting banks to greater federal supervision, meanwhile hoping for a savior in the style of Franklin Roosevelt. We should instead follow Ron Paul, who “was pushing a movement to audit the Fed, giving the public a chance to better scrutinize and govern the central bank.” Dr. Paul’s program can be stated more succinctly and accurately than this: End the Fed!

You Might Also Like

The German Rejection of Classical Economics

The German Rejection of Classical Economics

2022-06-03

The hostility that the teachings of Classical economic theory encountered on the European continent was primarily caused by political prepossessions. Political economy as developed by several generations of English thinkers, brilliantly expounded by Hume and Adam Smith and perfected by Ricardo, was the most exquisite outcome of the philosophy of the Enlightenment.

Carl Menger and the Austrian School of Economics

Carl Menger and the Austrian School of Economics

2022-06-01

What is known as the Austrian School of Economics started in 1871 when Carl Menger published a slender volume under the title Grundsätze der Volkswirtschaftslehre.

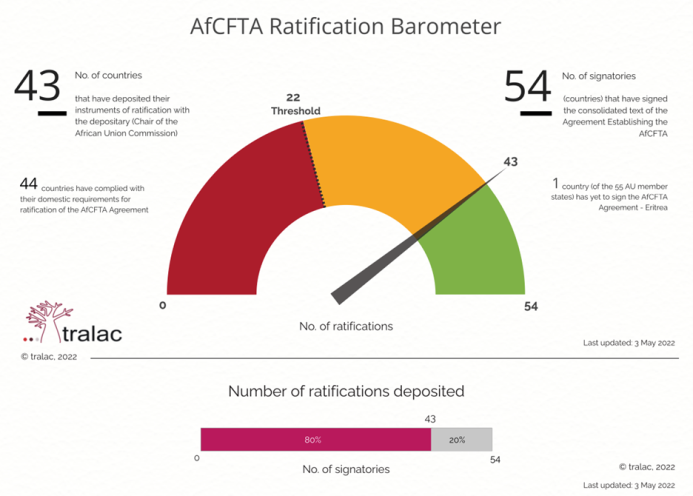

To Succeed, the AfCFTA Must Be about Actual Free Trade, Not Government-Managed “Free Trade”

To Succeed, the AfCFTA Must Be about Actual Free Trade, Not Government-Managed “Free Trade”

2022-05-30

The African Continental Free Trade Area (AfCFTA) is the world’s largest free trade area by the number of countries. It is the most ambitious and, given demographic trends, the most promising free trade project on earth. The AfCFTA matters very much to Africa’s economies separately and to the continent’s collaborative and integrated economic development.

Government Spending Is the Real Tax; Deficits Are a Sideshow

Government Spending Is the Real Tax; Deficits Are a Sideshow

2022-05-27

Many economists believe that during an economic slump government should run large budget deficits in order to keep the economy going with increases in government outlays, with the consequent budget deficit giving individuals more disposable money.

Ludwig von Mises (1881–1973)

Ludwig von Mises (1881–1973)

2022-03-25

One of the most notable economists and social philosophers of the twentieth century, Ludwig von Mises, in the course of a long and highly productive life, developed an integrated, deductive science of economics based on the fundamental axiom that individual human beings act purposively to achieve desired goals.

The West’s Russia Sanctions Could Lead to Many Unpredictable and Unpleasant Outcomes

The West’s Russia Sanctions Could Lead to Many Unpredictable and Unpleasant Outcomes

2022-03-20

Global supply shocks are historically rare events. All the more extraordinary to have two such shocks in quick succession—the second arriving even before the first has entirely faded away. That is what the world now experiences in the form of the Great Pandemic followed by the Great West-Russia economic war. The most visible symptom of the supply disruption is the sky-high price of energy and a range of other commodities.

With Inflation at a 40-Year High, the Fed Is Too Afraid to Act

With Inflation at a 40-Year High, the Fed Is Too Afraid to Act

2022-03-12

Price inflation has been accelerating upward since April of last year. Yet the Fed has done virtually nothing. What’s the Fed waiting for?

Economic Aspects of the Pension Problem

Economic Aspects of the Pension Problem

2022-03-08

On Whom Does the Incidence Fall? Whenever a law or labor union pressure burdens the employers with an additional expenditure for the benefit of the employees, people talk of “social gains.”

Tags: Featured,newsletter