Asset Allocation We believe that robust earnings growth will overcome concerns about rate increases. Within a neutral position on developed-market equities, we believe sectoral rotation will continue and we remain overweight cyclical markets like the UK and Japan. But while we believe the attractiveness of stocks subject to wild valuation swings will fade, we continue to like cash-rich ‘structural grower’ stocks. The rise in the correlation between bonds and equities is underlining the importance of portfolio diversification into alternative assets such as hedge funds. The case for government bonds is being increasingly challenged by growing debt supply and inflation expectations. We are also conscious of the increased sensitivity of corporate credits,

Topics:

Perspectives Pictet considers the following as important: 2.) Pictet Macro Analysis, 2) Swiss and European Macro, Featured, Macroview, Mexico, newsletter, Pictet

This could be interesting, too:

investrends.ch writes Vom Ölschock zum Stromsuperzyklus

investrends.ch writes Pictet steigt in den Schweizer Treuhandmarkt ein – Partnerschaft mit Tretor

investrends.ch writes Die Schweiz an der Schwelle zur digitalen Transformation der Fondsindustrie

investrends.ch writes Pictet setzt bei neuem Hedgefonds auf KI

Asset Allocation

Asset Allocation

We believe that robust earnings growth will overcome concerns about rate increases. Within a neutral position on developed-market equities, we believe sectoral rotation will continue and we remain overweight cyclical markets like the UK and Japan. But while we believe the attractiveness of stocks subject to wild valuation swings will fade, we continue to like cash-rich ‘structural grower’ stocks.

The rise in the correlation between bonds and equities is underlining the importance of portfolio diversification into alternative assets such as hedge funds.

The case for government bonds is being increasingly challenged by growing debt supply and inflation expectations. We are also conscious of the increased sensitivity of corporate credits, particularly US investment grade, to rising market rates. Our preference goes to short duration. We continue to overweight alternative investments (private equity and hedge funds).

Macroeconomy

The UK and US may have delivered single jabs equivalent to 70% of their populations by early May. It may take several months after for the euro area to reach a similar level.

We believe the US could achieve 15% annualised GDP growth in Q2 as con_dence improves and households spend again and we have upped our annual GDP forecast to 6.5% in 2021. Despite improving growth and market pressure, we believe the Fed will refrain from raising policy rates before 2024.

We expect the euro area to experience a consumer-led economic rebound in late Q2/early Q3. Our central GDP forecast for the euro area in 2021 is 4.3%, with the UK set for growth of 5.5%.

While its recovery remains uneven, we expect Chinese GDP to grow 9.3% in 2021. Rising global demand should help Japan to 2.7% growth this year.

Commodities

Despite global re-opening, there are reasons (most notably abundant capacity) to expect the rise in oil prices to moderate as the year progresses. While production discipline is helping prices for now, our year-end target for Brent oil is USD55.

Currencies

Fiscal stimulus and rapid re-opening of the US economy have led to a rise in real interest rates and boosted the US dollar. We still believe that the dollar’s strength could be challenged as the year progresses and the recovery gathers pace in other countries.

Equities

Earnings upgrades continue to support developed-market equities, despite the fast rise in bond yields and elevated multiples. We believe rapid re-opening of economies could stimulate further sectoral rotation and diminish the previous lopsided performance of US stocks, dominated by ‘Big Tech’.

The move away from defensives has been hurting European consumer staple stocks. While falling, the sector still trades at a premium to the overall market. There is potential for consumer staples to pick up momentum later this year should Treasury yields and emerging markets stabilise. Relative valuations have also become more attractive in US consumer staples.

Fixed Income

A fast economic recovery and persistent Fed dovishness mean that we are raising our year-end forecast for the 10-year US Treasury yield to 2.1%. The rise in rates has been hurting US investment-grade credits. We are underweight US high yield, but shorter duration and better quality mean we are neutral its euro equivalent.

Asian Assets

A robust recovery, policy stability and relatively high yields are reasons to consider judicious positioning in Chinese bonds for carry purposes. We also think the Chinese renminbi will remain a powerful anchor for other Asian (ex-Japan) currencies, which are more defensive than other EM currencies. But we are attentive to the impact slow vaccine rollouts and rising US rates have on Asian equities.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars – March 29, 2021

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars – March 29, 2021

2021-03-29

Update March 29 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.2 bn. compared to last week, this means the SNB is selling euros and dollars.

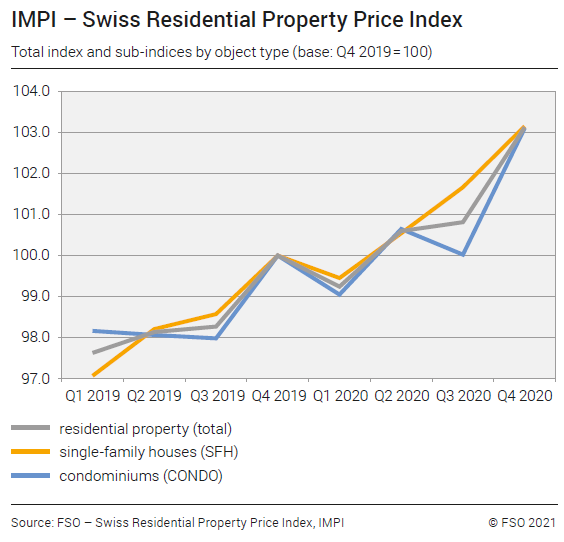

Average annual inflation rate for residential property in 2020 was 2.5 percent

Average annual inflation rate for residential property in 2020 was 2.5 percent

2021-02-16

16.02.2021 – The Swiss residential property price index (IMPI) increased in the 4th quarter 2020 compared with the previous quarter by 2.3% and reached 103.1 points (4th quarter 2019 = 100). Compared with the same quarter of the previous year, inflation was 3.1%. The average annual inflation rate for residential property in 2020 was 2.5%.

FX Daily, February 12: Animal Spirits Start the Weekend Early

FX Daily, February 12: Animal Spirits Start the Weekend Early

2021-02-12

Profit-taking weighs on equity markets, and the dollar is trading higher ahead of the weekend. Most Asia Pacific markets are still closed for the holiday, but Victoria’s snap lockdown dragged Australian shares lower.

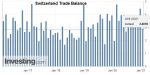

Swiss Trade Balance Foreign trade 2020: historic decline against the backdrop of a pandemic

Swiss Trade Balance Foreign trade 2020: historic decline against the backdrop of a pandemic

2021-01-28

Switzerland’s 2020 foreign trade will bear the brunt of the consequences of the COVID-19 pandemic: exports (-7.1% to 225.1 billion francs) and imports (-11.2% to 182.1 billion) posted a historic decline. Never before have they suffered such a significant quarterly decline as in the second quarter of 2020. Foreign trade has fallen back to its level recorded three years earlier. The trade balance closed the year with a record surplus of CHF 43.0 billion.

House View, November 2020

House View, November 2020

2020-11-10

The upsurge in covid-19 cases will likely hurt global economic prospects in the current quarter. With a Democrat ‘blue wave’ failing materialise in the US elections, hopes of a substantial spending bill have faded and there is risk that US household incomes suffer as existing support measures fade. In the meantime, covid-19 infections continue surge in the US.

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

2020-11-09

The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia.

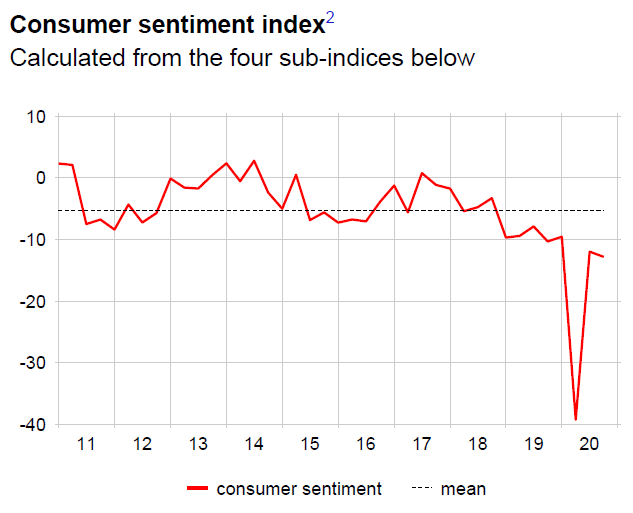

Swiss Consumer sentiment: No further recovery of consumer sentiment

Swiss Consumer sentiment: No further recovery of consumer sentiment

2020-11-05

Consumer sentiment in Switzerland has largely been stagnating since the summer. All sub-indices used for the calculation are still below their long-term average and none have improved significantly compared to this summer’s survey. Economic development and the situation on the labour market are seen as unfavourable.

Weekly View – A sure thing

Weekly View – A sure thing

2020-10-27

Signs from last week’s SURE programme to finance partial unemployment schemes are highly encouraging for the EU’s plans for recovery fund issuance which could start, we believe, in mid-2021. Last week’s SURE issue was close to 14 times oversubscribed at a rate lower than that for French government bonds of comparable duration.

Tags: Featured,Macroview,Mexico,newsletter,Pictet