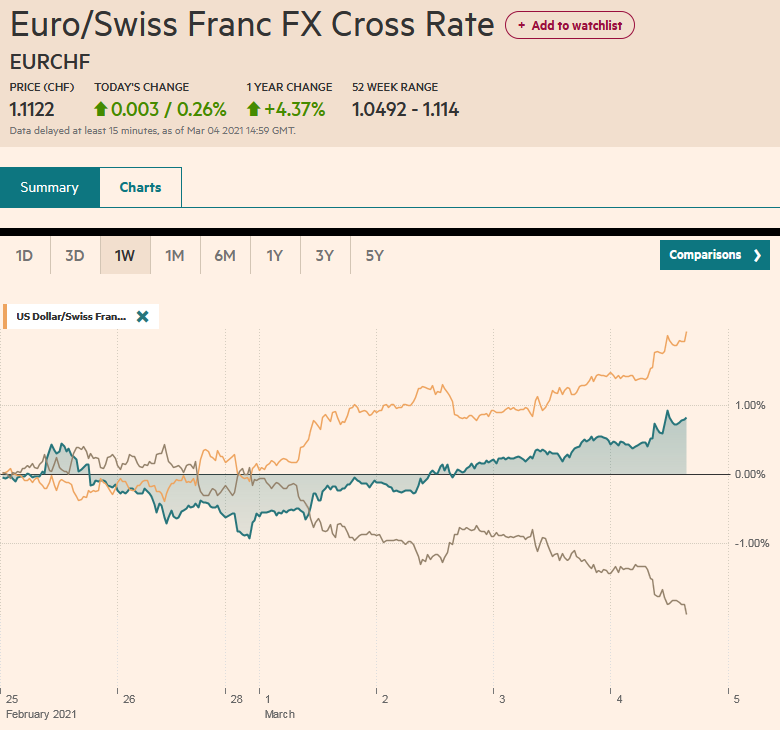

Swiss Franc The Euro has risen by 0.26% to 1.1122 EUR/CHF and USD/CHF, March 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Equities are under pressure following yesterday’s sharp losses in the US. The MSCI Asia Pacific Index suffered its biggest decline of the week today as Japanese, Chinese, and Hong Kong benchmarks slid by more than 2%. The Dow Jones Stoxx 600 Index in Europe is buckling under the pressure and is posting its first decline of the week. US stocks remain soft, but the futures on the major indices are off their lows. The US 10-year yield is around 1.47%, while European yields are 1-2 bp lower. Australia and New Zealand benchmark yields jumped 10-11 bp. The RBA did not step up its bond

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, Chna, Currency Movement, Featured, Federal Reserve, newsletter, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.26% to 1.1122 |

EUR/CHF and USD/CHF, March 4(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Equities are under pressure following yesterday’s sharp losses in the US. The MSCI Asia Pacific Index suffered its biggest decline of the week today as Japanese, Chinese, and Hong Kong benchmarks slid by more than 2%. The Dow Jones Stoxx 600 Index in Europe is buckling under the pressure and is posting its first decline of the week. US stocks remain soft, but the futures on the major indices are off their lows. The US 10-year yield is around 1.47%, while European yields are 1-2 bp lower. Australia and New Zealand benchmark yields jumped 10-11 bp. The RBA did not step up its bond purchases and the 3-year yield, targeted at 10 bp, is near 16 bp. The dollar is mostly firmer. Among the majors, the dollar-bloc currencies are off the least, and within the emerging currency complex, the Mexican peso, Russian ruble, and South African rand are a little stronger. Gold fell to nearly $1700 yesterday and is consolidating in the lower end of yesterday’s range. Oil prices are trading lower ahead of the OPEC+ meeting outcome. Output is expected to rise by 1.2-1.5 mln barrels next month. |

FX Performance, March 4 - Click to enlarge |

Asia Pacific

Australia reported a record trade surplus for January of a little more than A$10 bln, which was about a quarter more than the Bloomberg survey’s median forecast. Exports rose by 6%, doubling from the 3% increase in December and better than expected. Imports fell by 2% after a 1% decline in December. Of note, the export value of commodities fell, except for alumna and natural gas. Iron ore exports fell by 7.1% after a record was set in December. Coal exports were off 7.5%. By destination, shipments to China were off 8.2%, to Japan down 16.6%, and to South Korea off 1.6%. Given the Lunar New Year holiday in China and elsewhere in the region, the February data may see a further decline in exports to the region.

China’s annual “two sessions” began earlier today and runs through March 11. Today is the Chinese People’s Political Consultative Conference ahead of tomorrow’s National People’s Congress. The former US Secretary of State Pompeo appeared to call for regime change in China. The helpfulness of such arguments aside, the Chinese Communist Party has 90 mln members. One commentator noted that it would be the fifteenth largest in the world and well ahead of Germany’s 80 mln people if it were a country.

If China has emerged from the Covid crisis stronger, it is primarily because the US and Europe have not comported themselves particularly well. China appears to have weathered the US tariffs and made adjustments, including the sale of Huawei’s cell phone manufacture business, which once was the world’s largest. China-based producers scramble for chips after the sanctions on Huawei and SMIC, and US pressure on Taiwan’s TSMC not to sell chips to sanctioned companies, even though it has a fabrication facility on the mainland. Huawei used to be one of TSMC’s largest customers.

The National People’s Congress will formally endorse the new Five-Year plan, whose broad strokes are already known to include greater self-reliance, a strong infrastructure initiative, and ambitious environmental goals. Many shake their heads at the “dual circulation” concept but isn’t that really the culmination of the export-oriented development? The export thrust eventually is supposed to give way to stronger domestic consumption as the engine of growth. Of course, there are several mature high-income countries in Europe and Asia that still export 30%-50% of GDP.

Rising US yields continue to overshadow the impact of falling equities on the dollar-yen exchange rate. The dollar has risen above the previous day’s high for the seventh consecutive session today and reached JPY107.35, the highest level since last July. The JPY107.50 area is the next immediate hurdle, but we anticipate a test on the JPY108 area in the near-term. Initial support may be seen around JPY107. The Australian dollar is little changed, around $0.7775. There are two sets of chunky options set to expire today. The first is A$1 bln at $0.7800, and the other is for A$1.3 bln at $0.7825. Today’s high has been $0.7815, while the week’s high is a little shy of $0.7840. Initial support is seen near Tuesday’s low, around $0.7735. The bank models in Bloomberg’s survey were close to anticipating the dollar’s fix today at CNY6.4758. The PBOC drained CNY10 bln in open market operations, and money market rates jumped 29-40 bp. So far this week, the dollar has been confined to last week’s range against the yuan (~CNY6.4460-CNY-6.4830).

Europe

The main strokes of the UK budget were in line with the expectations shaped by media reports. Near-term assistance was extended while raising corporate taxes, especially on large businesses, from 19% to 25% by 2023 were announced. Small businesses (profits less than GBP50k) will still be taxed at 19%. The corporate tax hike is partly blunted by the 130% deductibility of capex. Fast-tracking immigration of highly skilled workers and new green savings bonds for retail investors initiatives were unveiled. A new plan program for businesses (80% underwritten by the government) will replace the current program aimed at helping businesses cope with the lockdowns was also announced. Gilt yields jumped on the news that the Debt Management Office anticipates selling GBP296 bln of bonds this fiscal year, almost 20% more than many economists projected.

The EU is threatening legal action against the UK for violating the trade agreement. Yesterday, the UK government unilaterally declared it will waive customs forms on food entering Northern Ireland until October. The agreement struck with the EU allowed the waiver only until the start of next month. In negotiations, the UK wanted the deadline to be the start of 2023, which the EU summarily rejected.

The euro remains within this week’s range (~$1.1990-$1.2115) and is in less than half of a cent range today. The session low, a little above $1.2025, was set in early European turnover. The upside appears capped, initially around $1.2075, where an option for almost 520 mln euros is set to expire today. There is another option at $1.20 for roughly the same amount that also rolls off today. Sterling, too is well within the recent range (~$1.3860-$1.4000). Today, it found support near yesterday’s low (~$1.3920), which is just below the 20-day moving average. There is an option for GBP550 mln at $1.39 that will be cut today.

America

The battle of the stimulus bills is not completely over, though the Democrats seem to be largely negotiating with themselves. Biden has agreed to narrow the eligibility for the stimulus checks. The previous cap was $100k for individuals $200k for couples. The new cap is $80k and $160k, respectively. The attempt to cut supplemental jobless benefits to $300-a-week from $400 appears to have been rebuffed. The extension is expected to be extended through August (another fiscal cliff?). The Congressional Budget Office will provide its official estimate of the adjusted package cost, and the Senate is expected to vote on it as early as this weekend. The current extra jobless benefits expire March 14, the ostensible deadline for passage of the new stimulus. Meanwhile, the next big battle has begun. Infrastructure. The American Society of Civil Engineers weighed in with its latest assessment. It is estimated that the investment gap stands at nearly $2.6 trillion. This is seen at the low end of what the Biden administration will propose.

The US weekly jobless claims are likely to recover after the large weather-induced drop (-111k) in the week ending February 19. The four-week moving average is around 808k, and before the weather distortions, it was in the 830k area. The US also reports factory orders. The 2.1% increase anticipated by the median forecast in Bloomberg’s survey would be the strongest since last July. Durable goods orders rose 1.4% in January and are subject to revision today.

Yet, today’s highlight is Fed Chair Powell’s economic discussion at a Wall Street Journal function near midday on the East Coast. It is unreasonable to expect a substantial change in his assessment or rhetoric. The US is familiar with jobless recoveries. Despite the surge in growth, there is considerable slack in the labor market, where both Powell and Yellen have suggested that the real unemployment rate is closer to 10%. Fed officials have consistently played down the significance of the rise in yields, suggesting it reflects optimism about the outlook. Still, if officials have expressed concern, is it over the pace of the adjustment. The regulatory uncertainty (the waiver on including Treasury holdings and excess reserves from leverage ratios expires at the end of this month) does not help matters. While some in Congress (e.g., Warren) has opposed an extension, the failure to do so would likely reduce dealers’ appetite for Treasuries while record sales loom. Moreover, as the Fed remains committed to buying $80 bln of Treasuries and $40 bln of Agency MBS a month, excess reserves are set to expand. The interaction of these three forces, inflation expectations, record supply, and the uncertain regulatory environment, is the key to the price action.

For the fourth session, the US dollar has remained within last Friday’s range against the Canadian dollar (~CAD1.2590-CAD1.2750). It has spent most of this week so far on the CAD1.26 handle. More immediately, resistance is seen near CAD1.2680 and support around CAD1.2620. The same observation holds for the US dollar against the Mexican peso, except rather than being confined to last Friday’s range, it is last Thursday’s (~MXN20.37-MXN21.0360). Mexico’s central bank raised its GDP forecast to 4.8% this year from 3.3% and expects inflation to finish the year within its target range. The dollar tested the MXN21.00 level yesterday and is pulling back today. Initial support was found near MXN20.83. A break of MXN20.80 may signal a test on the MXN20.70 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-03-01

Update March 01 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.2 bn. compared to last week, this means the SNB is selling euros and dollars.

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices – February 22, 2021

2021-02-22

Update February 22 2021: SNB intervening. Sight Deposits have risen by +0.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.1 bn. compared to last week.

FX Daily, December 16: Greenback Slides Ahead of FOMC as Optimism Underpins Risk Appetites

FX Daily, December 16: Greenback Slides Ahead of FOMC as Optimism Underpins Risk Appetites

2020-12-16

Overview: The S&P 500 snapped a four-day downdraft helped by optimism over the progress toward fiscal stimulus and some hope that a new trade deal can still be negotiated between the UK and EU. Europe reported better than expected PMIs. Equities are broadly higher, as are interest rates, while the dollar slumps.

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

2020-12-02

The selling pressure that drove the dollar lower yesterday has abated, and the greenback is paring yesterday’s loss, though the dollar-bloc currencies are showing some resilience. EC negotiator Barnier briefed ministers that the same three issues that have bedeviled the trade talks with the UK remain unresolved (fisheries, level playing field, and a conflict resolution mechanism).

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

2020-11-25

The global equity rally appears to be stalling after the US markets rallied strongly yesterday. Chinese, Taiwan, Korean, and Indian indices fell, and the MSCI Asia Pacific Index appears to have posted only its second loss this month. European shares are narrowly mixed, leaving the Dow Jones Stoxx 600 little changed.

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

FX Daily, November 20: US Treasury-Fed Dispute Spurs Handwringing but Immediate Market Impact was Exaggerated

2020-11-20

Overview: News that the stimulus talks between the House Democrats and Senate Republicans was the excuse traders were looking for to extend the US equity gains yesterday, but shortly after the close, confirmation that Treasury was not going to agree to extend several Fed facilities sent stocks reeling.

FX Daily, November 16: Risk-On Despite Surging Pandemic

FX Daily, November 16: Risk-On Despite Surging Pandemic

2020-11-16

Despite the surging pandemic and new restriction measure, risk-appetites appear strong to start the week. Led by 2% gains in the Nikkei and Taiwan’s Taiex, all of the Asia Pacific region’s equity markets advanced. European markets have followed suit and the Dow Jones Stoxx 600 is knocking on last week’s eight-month high.

FX Daily, October 1: Hope Springs Eternal

FX Daily, October 1: Hope Springs Eternal

2020-10-01

Speculation that a new round of fiscal stimulus from the US is possible is encouraging risk-taking today. Many large Asian centers were closed for holidays today, and a technical problem prevented the Tokyo Stock Exchange from opening.

Tags: #USD,Brexit,Chna,Currency Movement,Featured,federal-reserve,newsletter,U.K.