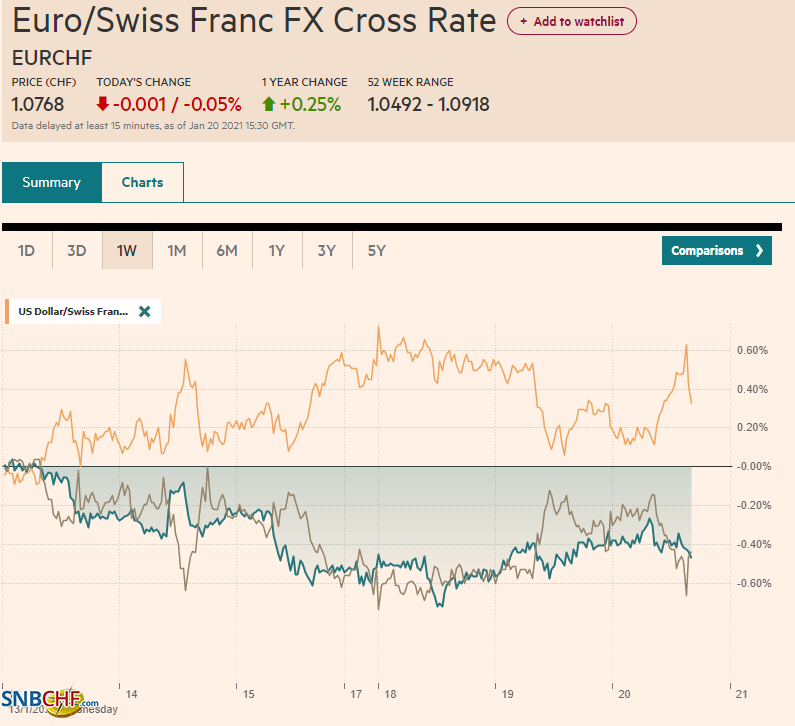

Swiss Franc The Euro has fallen by 0.05% to 1.0768 EUR/CHF and USD/CHF, January 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Global equities are moving higher today. Led by continued strong buying of Hong Kong shares, the MSCI Asia Pacific Index rose to new highs. The Hang Seng is up 6% this year and is approaching the 2019 record high. Australia’s shares set a new record today. Japan and Taiwan bucked the trend. Europe’s Dow Jones Stoxx 600 has recouped yesterday’s 0.2% loss plus some, led by information technology and consumer discretionary sectors. The S&P 500 and NASDAQ futures point to a higher open in the US as the benchmarks probe near record highs. Benchmark yields are little changed today,

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Canada, China, Currency Movement, EUR/CHF, Featured, GBP, MXN, newsletter, Taiwan, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.05% to 1.0768 |

EUR/CHF and USD/CHF, January 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equities are moving higher today. Led by continued strong buying of Hong Kong shares, the MSCI Asia Pacific Index rose to new highs. The Hang Seng is up 6% this year and is approaching the 2019 record high. Australia’s shares set a new record today. Japan and Taiwan bucked the trend. Europe’s Dow Jones Stoxx 600 has recouped yesterday’s 0.2% loss plus some, led by information technology and consumer discretionary sectors. The S&P 500 and NASDAQ futures point to a higher open in the US as the benchmarks probe near record highs. Benchmark yields are little changed today, with the US 10-year near 1.10%. European bond yields are a touch firmer, including Italy after the government survived the confidence vote yesterday. The dollar is mostly softer, but the euro is not participating so much, perhaps a note of caution ahead of tomorrow’s ECB meeting. The Swedish krona is also slightly weaker as one of its central bankers indicated that a return to negative rates cannot be ruled out. We see a greater risk of a small rate cut by the Bank of Canada today than the market. Emerging market currencies are mostly moving higher, and the JP Morgan Emerging Market Currency Index is higher for the third session. The Mexican peso rose to a new 10-month high. Gold has continued to recover after it approached $1800 at the start of the week. It reached almost $1857.50 today to move back above the 200-day moving average ($1845.40). Yet, the intraday technical indicators warn the yellow metal may be topping. March WTI rallied 1% yesterday and is up nearly another 1% today to test the $53.50-$53.70 area. Last week’s high, just shy of $54 a barrel, was the highest since last February. |

FX Performance, January 20 - Click to enlarge |

Asia Pacific

A new outbreak of the virus in China will likely impact plans to celebrate the Lunar New Year. Hundreds of millions of people usually travel during this period. Fewer travelers are expected now. The restrictions directly impact some industries, including oil refineries, and some indirectly via shifting demand expectations.

The nominees for US Treasury Secretary (Yellen) and Secretary of State (Blinken) took tough lines on China during their confirmation hearings yesterday. Particularly noteworthy was that Blinken endorsed the assessment by Pompeo, who labeled Beijing’s treatment of the Uighurs a genocide. The testimony strengthened our conviction that the US confrontation of China is bipartisan and will persist under the Biden administration. Separately, but related, we note that the UK government narrowly (319-308) defeated an amendment that would have pressed UK judges to rule that the Uighurs’ treatment is indeed a genocide, which would allow different types of legal action.

Taiwan reported a 38.3% surge in December export orders to a record $60.6 bln. Another strong rise is expected in January (~44.5%-48.5%). Two key Apple suppliers, Taiwan Semiconductor Manufacturing and Hon Hai Precision Industry, posted record revenue in Q4 20. Although Taiwan officials often seem anxious about the Taiwanese dollar’s appreciation and its impact on exports, we note that the strong export orders were recorded even as the currency rose. The Taiwanese dollar is near its best level in more than 20-years.

The dollar is in a very narrow range against the Japanese yen today. It has barely ventured out of a 10-tick range on either side of JPY103.85. A two-week trendline comes in a little above JPY104.00, and a recent base has been forged near JPY103.50. The Australian dollar set a three-day high near $0.7740 in the local session, but the momentum stalled in Europe. A break now of $0.7720 would boost the chances that a near-term high is in place. Some caution may prevail ahead of the December jobs report to be delivered first thing on Thursday in Australia. Job growth surprised in November, and the median forecast in the Bloomberg survey calls for another 50k increase (after 90k in November). The reference rate for the dollar was set at CNY6.4836, on the strong side of expectations. It kept its loan prime rates unchanged for the ninth consecutive month. Still, the PBOC injected the most liquidity into the financial system in more than three months apparently to protest and relieve the tightness in the money markets, in part caused by tax payments. The US dollar weakened for the second consecutive session against the yuan ending a four-day advancing streak. Around CNY6.4670, the dollar is around the middle of its recent range.

Europe

Italy’s government, led by Prime Minister Conte, secured a victory in the Senate yesterday. It buys Conte more time to solidify support for the government. It managed to survive yesterday’s vote because more than a dozen Senators abstained, making it easier to hold a majority of those that voted. However, the government did not secure an overall majority. To pass key legislation and have a stable government, Conte needs to find more support.

The UK reported price pressure firmed last month and by a little more than economists anticipated. The preferred measure, CPIH, which includes owner-occupied housing costs (which, incidentally, the ECB is thinking of including as well), rose by 0.8% year-over-year. It follows a 0.6% gain in November and compares to the median forecast of 0.7% in the Bloomberg survey. Core prices accelerated to 1.4% from 1.1% in November. Core inflation averaged 1.3% in Q4 for the third consecutive quarter. Separately, producer output prices were also slightly stronger than expected at 0.3%, and the November series was revised to 0.3% from 0.2%, but the year-over-year rate is still negative (-0.4% vs. -0.6%). Input prices were firm and rose to 0.8% in December, which was sufficient to turn the year-over-year rate positive (0.2%), and for the first time since August 2019, it is above zero.

The euro extended its recovery off Monday’s low (~$1.2055) to reach almost $1.2160 in late Asia and was sold a little through $1.2115 in the European morning. While the ECB is not expected to take fresh actions at tomorrow’s meeting, it would not be surprising if a sober economic outlook and disinflationary pressure lead to some bearish pressure. A move above the $1.2165-$1.2200 band would suggest the euro’s downside correction is over. Sterling has been bid to marginal new high just shy of $1.3720 in the European morning. It is the fourth consecutive week that higher highs were recorded. Some demand may have been related to an option for nearly GBP390 mln at $1.3700 that expires today. The intraday momentum indicators are stretched.

America

Biden will become the 46th President of the United States today. There will be a flurry of executive orders, including re-joining the Paris Agreement, canceling the permits for the XL pipeline, extending student loans’ deferment, extending the restrictions on evictions foreclosure, and lifting the ban on immigrants from Muslim countries has been widely tipped.

Yellen’s confirmation hearing was largely as anticipated. She endorsed market-determined exchange rates and showed a determination for others to do the same. Yellen seemed to take the right stance regarding China, where several of its trade and exchange rate practices are not up to the global standards. While she seemed to agree with all of her questioners, she pushed back on fiscal policy, where several Senators expressed reluctance to support another large fiscal package when the $900 bln package last month was not fully implemented. The fiscal support is shaping up to be a key test for the Biden administration. It wants to avoid going down the reconciliation path, which would allow it to just razor-thin majority to pass key legislation instead of finding compromises with the opposition. One tell of how it may go is whether Senate can return to the rules and behaviors that they previously did the last time there was such a balance of power, which means preserving the filibuster (needs 60 votes to overcome).

Outside of the US political spectacle, the market focus is on Canada. First is the December CPI. The headline is expected to be steady at 1.0%. The underlying measures have been firmer but also mostly steady in the 1.5%-1.9% range. Second, and more importantly, the Bank of Canada rate decision is expected. Most anticipated that the overnight target rate will be left at 25 bp. However, the recent string of disappointing data, the pandemic, and official comments raise the possibility of a small rate cut. Governor Macklem has suggested that the zero bound is above zero but below the 25 bp. A mini-cut would take many by surprise and could spur a quick decline in the Canadian dollar.

The US dollar was sold from a little above CAD1.2760 yesterday to CAD1.2690 today, which is a retracement objective the recent bounce (from CAD1.2625 to CAD1.2800). Note that tomorrow there is a large ($1.9 bln) option at CAD1.2715 that expires. On a mini-rate cut by the Bank of Canada, the US dollar could firm toward CAD1.2720-CAD1.2740. The greenback has slipped to a new marginal low against the Mexican peso near MXN19.5865. This is the dollar’s lowest level since last March. The intraday momentum indicators suggest the marginal new low may have exhausted the dollar bears, and a firmer tone may emerge. Initial resistance is now seen in the MXN19.65-MXN19.70 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

2020-08-18

The NASDAQ rallied 1% yesterday to record highs as the Dow Industrials struggled, and the S&P 500 was able to eke out a small gain. The coattails were short, and the strength of the yen may have contributed to a 0.2% loss of the Nikkei. Still, its 6.2% advance this month is the best among the G10.

FX Daily, January 11: Greenback Extends Recovery

FX Daily, January 11: Greenback Extends Recovery

2021-01-11

Julius Ceasar is said to have "crossed the Rubicon" on January 10, 49 BCE, taking the 13th Legion into Rome, defying orders from the Senate, and precipitating the Roman Civil Wat that marked the end of the republic and the birth of the empire.

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

2020-08-26

A consolidative tone has emerged after US equity benchmarks reached new highs yesterday. The MSCI Asia Pacific Index had reached seven-month highs on Tuesday, but Japan, China, and Australian stocks saw modest profit-taking today. European shares are recouping yesterday’s minor loss, and US shares are flat.

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

FX Daily, September 14: UK Presses Ahead, China Strikes Out at German Pork Producers, and Moody’s Weighs on Turkey

2020-09-14

A flurry of deals, including the still-evolving Oracle-TikTok tie-up, helped lift equity markets in the Asia Pacific region. South Korea’s Kospi, and Indonesia, which had been battered last week, led the advance. The MSCI Asia Pacific Index rose for the third consecutive sessions. European bourses are little changed while US stocks are firmer.

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

FX Daily, November 5: The Dollar Slides and the Yuan Jumps

2020-11-05

Overview: The markets did not wait for the final vote count and took stocks and bonds higher while pushing the greenback lower. While it appears Biden will be the next US President, investors seemed to like the fact that his agenda will be checked by a Senate that may remain in Republican hands. Stocks are on a tear.

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

FX Daily, November 25: Risk Appetites Stall Ahead of the US Thanksgiving Holiday

2020-11-25

The global equity rally appears to be stalling after the US markets rallied strongly yesterday. Chinese, Taiwan, Korean, and Indian indices fell, and the MSCI Asia Pacific Index appears to have posted only its second loss this month. European shares are narrowly mixed, leaving the Dow Jones Stoxx 600 little changed.

FX Daily, January 08: Can the Dollar Find Traction Even if the Employment Data Disappoint?

FX Daily, January 08: Can the Dollar Find Traction Even if the Employment Data Disappoint?

2021-01-08

The global equity rally picked up this week as it closed in 2019. The MSCI Asia Pacific Index gained today and is up in nine of the past 10 sessions. It has fallen only in one week since the end of October. South Korea’s Kospi led today’s advance with a nearly 4% rally on the back of talks that were later played down between Hyundai and Apple.

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

FX Daily, January 19: Even When She Speaks Softly, She’s Yellen

2021-01-19

Overview: The animal spirits are on the march today. Equities are mostly higher, peripheral European bonds are firm, and the dollar is mostly softer. After posting the first back-to-back decline this year, the MSCI Asia Pacific Index bounced back today, led by a 2.7% gain in Hong Kong (20-month high) and a 2.6% rise in South Korea’s Kospi.

Tags: #GBP,#USD,Canada,China,Currency Movement,EUR/CHF,Featured,MXN,newsletter,Taiwan,USD/CHF