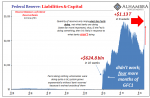

As I’ve said, it is a threefold failure of statistical models. The first being those which showed the economy was in good to great shape at the start of this thing. Widely used and even more widely cited, thanks to Jay Powell and his 2019 rate cuts plus “repo” operations the calculations suggested the system was robust. Because of this set of numbers, officials here as well as elsewhere around the world chose the most extreme form of pandemic mitigations, trusting that the strong economy wouldn’t just immediately buckle. And they were pushed in this direction by absolutely dire estimates for how COVID-19 was going to ravage large swaths of the globe. It hasn’t happened yet and increasingly looks like it never will. Federal Reserve: Liabilities & Capital,

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, Commitment of Traders, commodities, COT, crude stocks, currencies, Dollar, economy, eurodollar system, Featured, Federal Reserve/Monetary Policy, gasoline stocks, GFC1, GFC2, jay powell, Liquidity, Markets, newsletter, oil market, oil prices, steve mnuchin, stimulus, stocks, WTI, wti futures

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

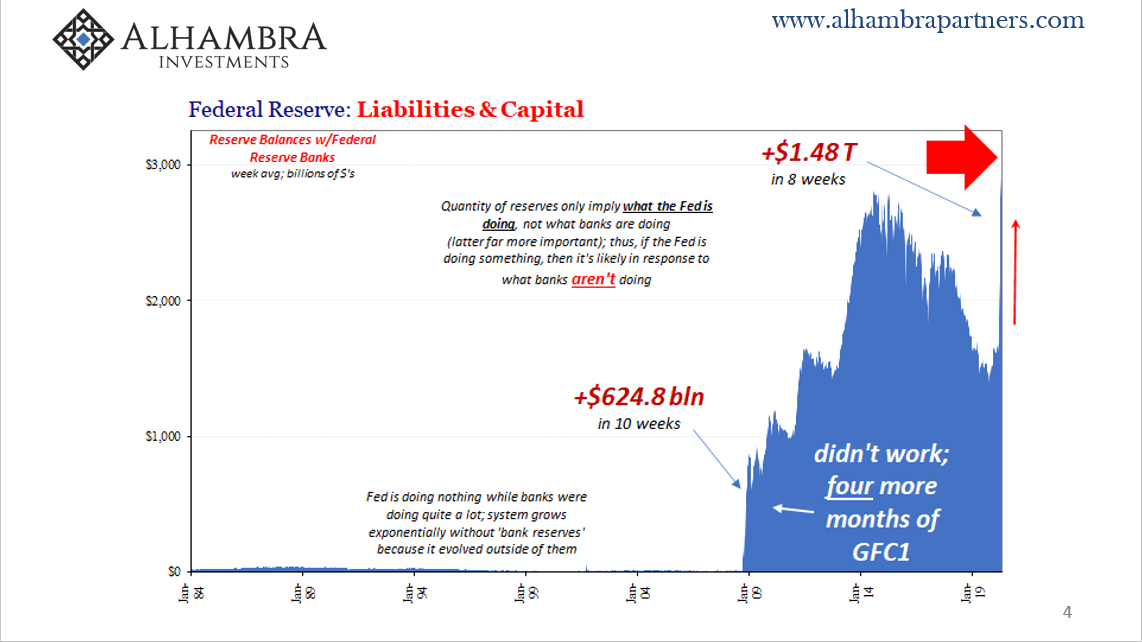

As I’ve said, it is a threefold failure of statistical models. The first being those which showed the economy was in good to great shape at the start of this thing. Widely used and even more widely cited, thanks to Jay Powell and his 2019 rate cuts plus “repo” operations the calculations suggested the system was robust. Because of this set of numbers, officials here as well as elsewhere around the world chose the most extreme form of pandemic mitigations, trusting that the strong economy wouldn’t just immediately buckle. And they were pushed in this direction by absolutely dire estimates for how COVID-19 was going to ravage large swaths of the globe. It hasn’t happened yet and increasingly looks like it never will. |

Federal Reserve: Liabilities & Capital, 1984-2019 - Click to enlarge |

| Having prioritized carpet bombing the economy, now they claim the models are projecting how everything will bounce back quickly. Sure, oh-for-two so far, for the most important period in the world’s history since the 1930’s we should just rely on the same sort of predictive capacities.

Except, the mainstream econometric models aren’t quite that sanguine. These say the economy will bounce back…mostly. And that’s the most optimistic case. Or was. Never mind those, says Treasury Secretary Mnuchin. We can’t rely on any of these stochastic constructions because this is new ground we’re trying to slog over. Instead, his super-secret figures are even more assuring as to how quickly the recovery will happen and how thoroughly we all make it the whole way back. On FoxNews, he told Chris Wallace:

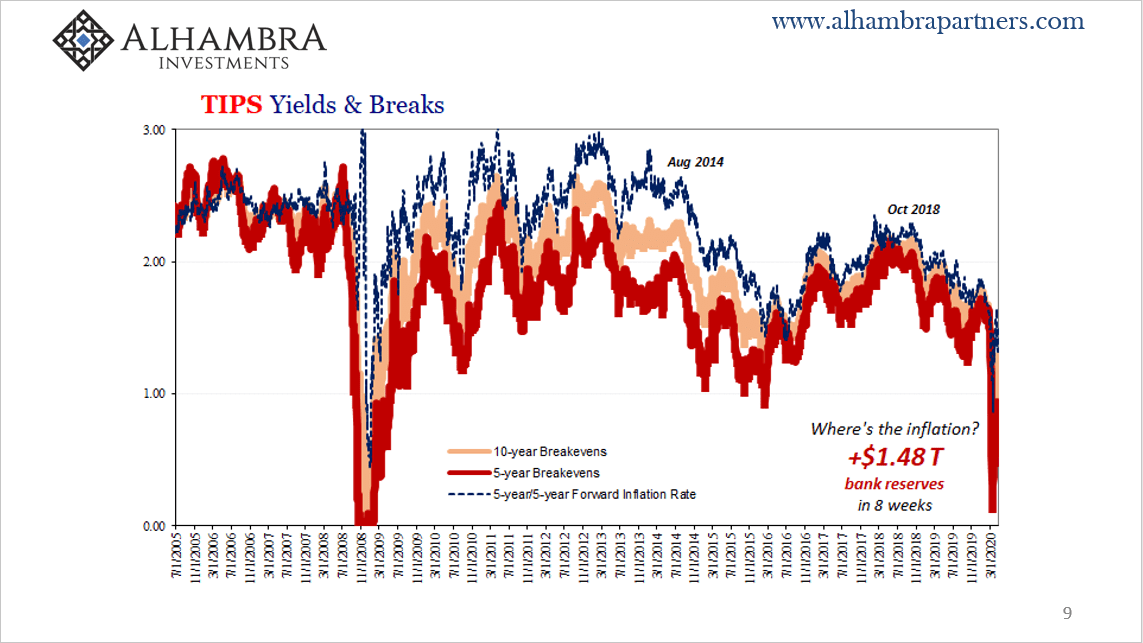

Then he added, “My own opinion is, again, we have unprecedented amount of liquidity in the system.” Oh dear. At least he noted how it is only his opinion as to the monetary system; which, is already an odd sort of development given he’s the damn Treasury Secretary. |

TIPS Yields & Breaks, 2005-2020 - Click to enlarge |

| No offense, Mnuchin, but you may not have noticed the similarities between the last two months and those of 2007-09; when, despite all the same assurances there definitely was a financial crisis because the same kinds of “liquidity” programs being implemented by Jay Powell today so conspicuously failed Ben Bernanke twelve years ago.

This isn’t the Financial Crisis; he’s right. It’s the second one. There is no longer “the” Financial Crisis, there is now GFC1 as well as GFC2. Don’t take the Fed’s word for it; for anything, especially liquidity. Not even the dip buyers on the NYSE are so sure like they once had been. |

|

| There wasn’t a day in late 2019 that didn’t go by when someone made the reference to the “obvious” money printing correlation between size of the Fed’s balance sheet and the direction of share prices in the aggregate. Suddenly, March 2020, “repo” operations and balance sheet expansion aren’t so sexy. |

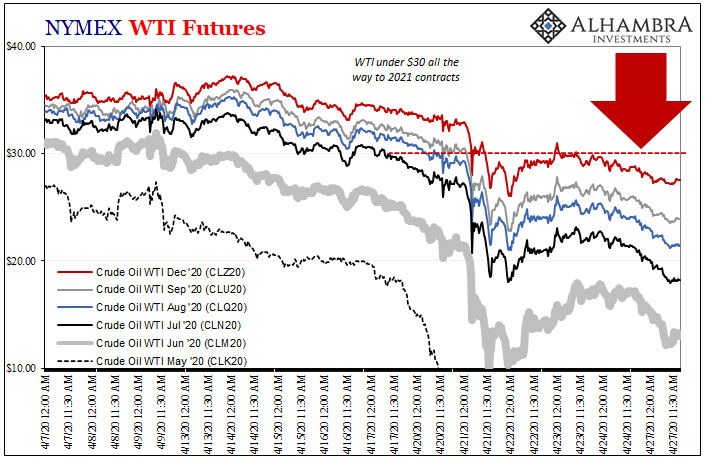

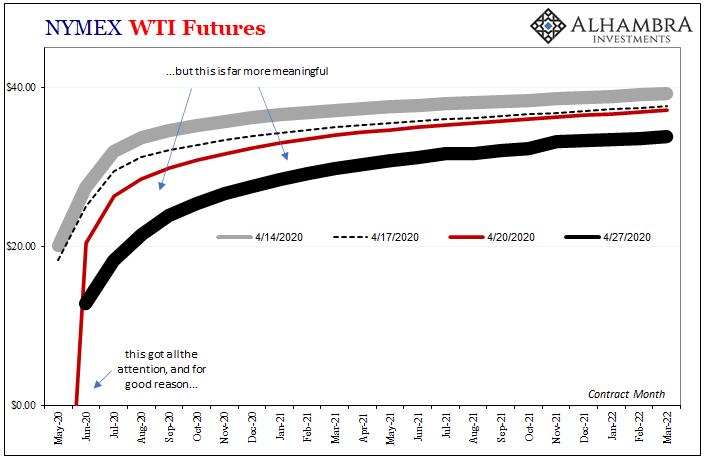

NYMEX WTI Futures, 2020 - Click to enlarge |

| In other markets less devoted to entertainment, situated far more closely to the real economy, what liquidity and stimulus? We are one week removed from oil prices hitting -$36. And while that spoke to short run chaos, it also meant a herd of investors which had come running at the sound of the Greenspan put learning to regret that very thing.

Greenspan’s put was always an empty bowl. |

NYMEX WTI Futures, 2020-2022 - Click to enlarge |

|

Away from oil future’s front month, the real bad news as far as Secretary Mnuchin and Fed Chairman Jay Powell should be concerned is the intermediate WTI curve. Oil prices are now sub-$30 as far as March 2021. Definitely not a statistical model, this real-world market is more aggressively discounting any chance of hitting the “V” shape. |

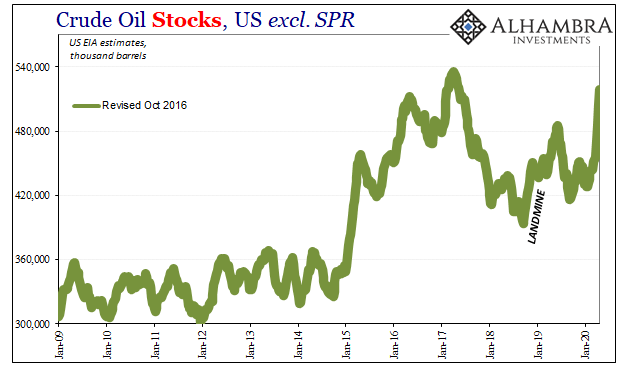

Crude Oil Stocks, US excl. SPR 2009-2020 - Click to enlarge |

| As far as the numbers go in Cushing, we’ve only begun to see product overflow. Crude oil stocks are looking very 2014-ish and it’s only just the start. In gasoline, what should be seasonal flows drawing down levels have instead become record high inventory. |

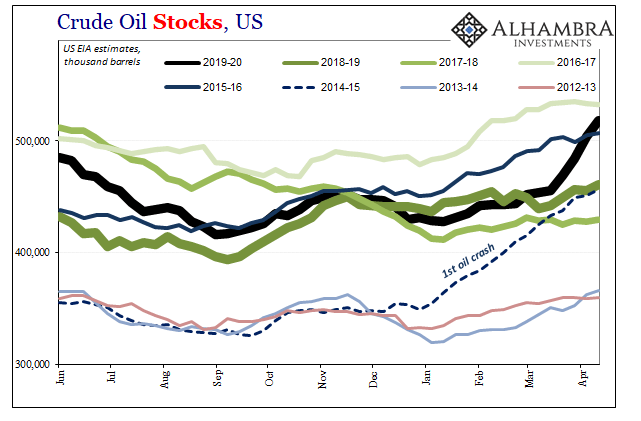

Crude Oil Stocks, US 2012-2019 - Click to enlarge |

Gasoline Stocks, US 2012-2019 - Click to enlarge |

|

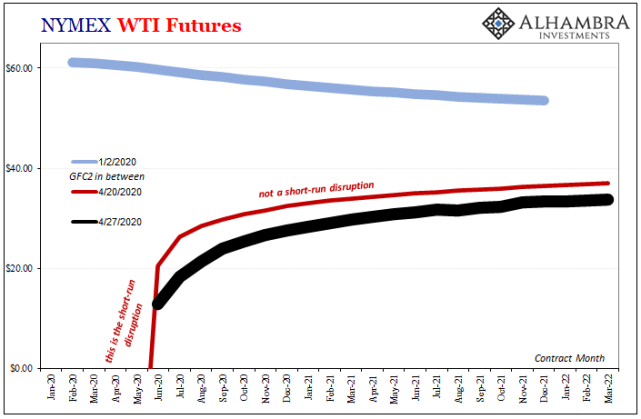

NYMEX WTI Futures, 2020-2022 - Click to enlarge |

|

|

Those results plus the way the WTI curve is shifting are the market pricing an intermediate future that isn’t at all what the Treasury Secretary hopes. The enormous inventories won’t be worked through quickly over the summer, the lack of demand plus the lack of liquidity combining to seriously menace a great many optimistic oil speculators who might be left. |

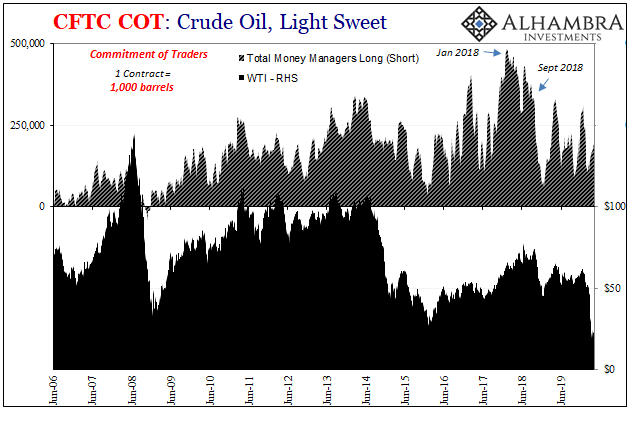

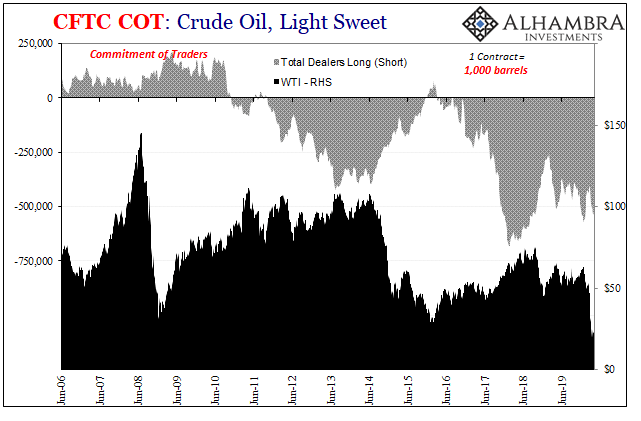

CFTC COT: Crude Oil, Light Sweet, 2006-2019 - Click to enlarge |

| Just who these specs are, it isn’t quite clear yet. The Commitment of Traders (COT) report didn’t show any out-of-character position changes last week. There was a spike in net longs among money managers, but nothing we haven’t seen before and nothing that would indicate large positions being trapped by last week’s highly unusual trading.

Was it everyone betting on Stimulus Steve? |

CFTC COT: Crude Oil, Light Sweet, 2006-2019 - Click to enlarge |

|

In other words, Secretary Mnuchin’s extra-special models forecasting a quick turnaround are grounded by the same thing which forms the basis of all extra-special super-secret prediction methods; the Fed’s imaginary “liquidity” and the assumption of “stimulus.” For a reminder about those, take it away Stan Fischer:

Everything about the current period smacks of GFC, right down to the stupid monetary policies central bankers are using to claim this is not a GFC. |

|

| In oil markets, it’s even worse, much worse GFC2 compared to GFC1.

And this thing is still getting started, with massive crude inventory yet to flow in (May deliveries) standing in for the enduring lack of demand economy-wide. The system which today is scheduled to be bouncing back in July, August, and September the oil market says that in July, August, and September we’ll be hearing how the big, complete rebound is definitely going to happen…in October, November, and December. And then it will be January, February, and March 2021 – for sure, the official modelers all promise. The first two sets of models screwed us, but this third one’s really going to hurt. |

CES: Civilian Labor Force Level, 2007-2020 - Click to enlarge |

You Might Also Like

Is GFC2 Over?

Is GFC2 Over?

Is it over? That’s the question everyone is asking about both major crises, the answer is more obvious for only the one. As it pertains to the pandemic, no, it is not. Still the early stages. The other crisis, the global dollar run? Not looking like it, either.

Three Short Run Factors Don’t Make A Long Run Difference

Three Short Run Factors Don’t Make A Long Run Difference

There are three things the markets have going for them right now, and none of them have anything to do with the Federal Reserve. More and more conditions resemble the early thirties in that respect, meaning no respect for monetary powers. This isn’t to say we are repeating the Great Depression, only that the paths available to the system to use in order to climb out of this mess have similarly narrowed.

An International Puppet Show

An International Puppet Show

It’s actually pretty easy to see why the IMF is in a hurry to secure more resources. I’m not talking about potential bailout candidates banging down the doors; that’s already happened. The fund itself is doing two contradictory things simultaneously: telling the world, repeatedly, that it has a highly encouraging $1 trillion in bailout capacity at the same time it goes begging to vastly increase that amount.

Banks Or (euro)Dollars? That Is The (only) Question

Banks Or (euro)Dollars? That Is The (only) Question

It used to be that at each quarter’s end the repo rate would rise often quite far. You may recall the end of 2018, following a wave of global liquidations and curve collapsing when the GC rate (UST) skyrocketed to 5.149%, nearly 300 bps above the RRP “floor.” Chalked up to nothing more than 2a7 or “too many” Treasuries, it was to be ignored as the Fed at that point was still forecasting inflation and rate hikes.

The Global Engine Is Still Leaking

The Global Engine Is Still Leaking

An internal combustion engine that is leaking oil presents a difficult dilemma. In most cases, the leak itself is obscured if not completely hidden. You can only tell that there’s a problem because of secondary signs and observations.If you find dark stains underneath your car, for example, or if your engine smells of thick, bitter unpleasantness, you’d be wise to consider the possibility.

The Fallen Kings & The Bond Throne of Collateral

The Fallen Kings & The Bond Throne of Collateral

There is no schadenfreude at times like these, no time to dance on anyone’s grave. Victory laps are a luxury that only central bankers take – always prematurely. The world already coming apart because of GFC1, what comes next with GFC2 and then whatever follows it? Another “bond king” has thrown in the towel.

COT Black: German Factories, Oklahoma Tank Farms, And FRBNY

COT Black: German Factories, Oklahoma Tank Farms, And FRBNY

I wrote a few months ago that Germany’s factories have been the perfect example of the eurodollar squeeze. The disinflationary tendency that even central bankers can’t ignore once it shows up in the global economy as obvious headwinds. What made and still makes German industry noteworthy is the way it has unfolded and continues to unfold. The downtrend just won’t stop.

Stagnation Never Looked So Good: A Peak Ahead

Stagnation Never Looked So Good: A Peak Ahead

Forward-looking data is starting to trickle in. Germany has been a main area of interest for us right from the beginning, and by beginning I mean Euro$ #4 rather than just COVID-19. What has happened to the German economy has ended up happening everywhere else, a true bellwether especially manufacturing and industry.

Tags: Bonds,Commitment of Traders,commodities,COT,crude stocks,currencies,dollar,economy,eurodollar system,Featured,Federal Reserve/Monetary Policy,gasoline stocks,GFC1,GFC2,jay powell,Liquidity,Markets,newsletter,oil market,oil prices,steve mnuchin,stimulus,stocks,WTI,wti futures