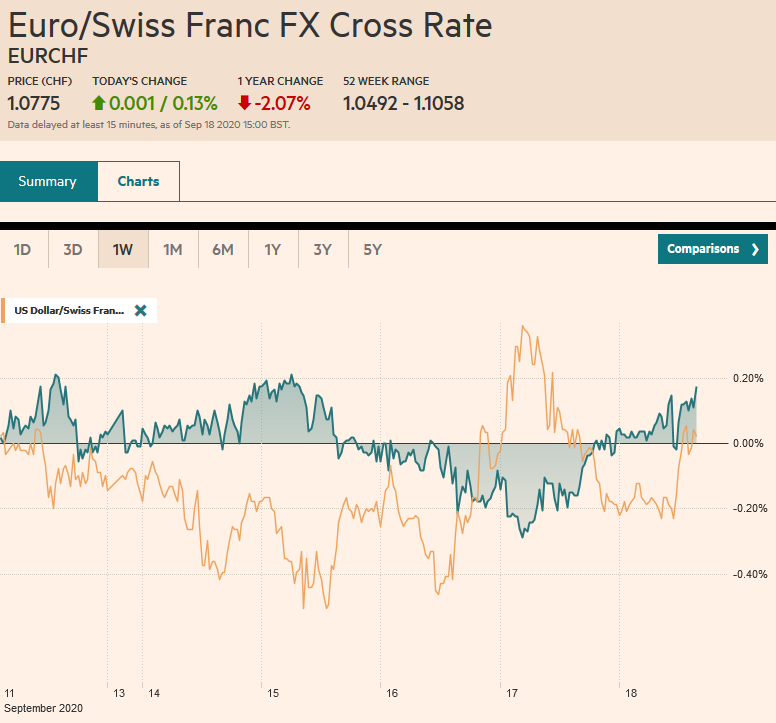

Swiss Franc The Euro has risen by 0.13% to 1.0775 EUR/CHF and USD/CHF, September 18(see more posts on EUR/CHF, USD/CHF, ). FX Rates Overview: Asia Pacific equities have taken the march on the US. Led by a 2% rally in Shanghai, most regional markets but Australia closed the week with gains. A two-week fall in the MSCI Asia Pacific Index has been snapped. European stocks are little changed, and the Dow Jones Stoxx 600 is holding on to its second week of gains. It is in the middle of the 360-380 range that has confined it here in Q3. US shares are also largely flat in Europe, and the S&P 500 is up about 0.5% this week coming into today. Benchmark bonds yields are slightly softer on Europe today, but the real takeaway this week is the nearly flat performance of

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Brexit, ECB, Featured, Federal Reserve, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.13% to 1.0775 |

EUR/CHF and USD/CHF, September 18(see more posts on EUR/CHF, USD/CHF, ) . |

FX RatesOverview: Asia Pacific equities have taken the march on the US. Led by a 2% rally in Shanghai, most regional markets but Australia closed the week with gains. A two-week fall in the MSCI Asia Pacific Index has been snapped. European stocks are little changed, and the Dow Jones Stoxx 600 is holding on to its second week of gains. It is in the middle of the 360-380 range that has confined it here in Q3. US shares are also largely flat in Europe, and the S&P 500 is up about 0.5% this week coming into today. Benchmark bonds yields are slightly softer on Europe today, but the real takeaway this week is the nearly flat performance of the 10-year US Treasury, German Bund, Japanese Government Bond, and the UK Gilt. The dollar is narrowly mixed against the major currencies. Emerging market currencies are mostly higher, led by South Korea, Indonesia, and Taiwan. Mexico and Turkey are nursing small losses. The JP Morgan Emerging Market Currency Index is posting small gains for the sixth consecutive session. Gold is firm and holding on to gains for the second successive week but is near the middle of the $1900-$2000 range. November WTI is firmer. It has risen every day since Monday, and if it holds on to or extends the 9.5% gain this week, it is the strongest performance in three months. |

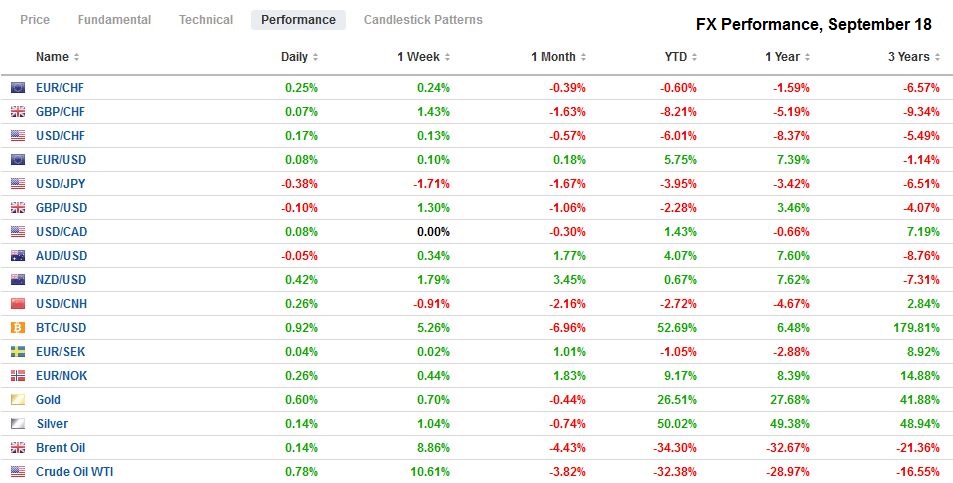

FX Performance, September 18 - Click to enlarge |

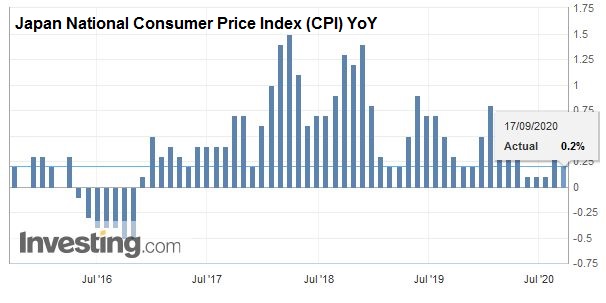

Asia PacificJapan’s August CPI was unsettling. The headline slipped to 0.2% year-over-year from 0.3%, but the challenge was the core, which excludes fresh food. It fell back below zero (-0.4%) for the first time since May. Yet, it will not cause nearly the consternation that the negative reading in the eurozone spurred. The main drag from Japan, like the EMU, was in core services. In Japan’s case, the government-led efforts to promote tourism and help the hospitality industry through discounts seemed to be the main culprit, shaving an estimated 0.3%-0.4% of CPI measures. The report is unlikely to spur fresh action by the BOJ, but we suspect that some additional steps are likely, especially if the new Suga government backs another supplemental budget. |

Japan National Consumer Price Index (CPI) YoY, August 2020(see more posts on Japan National Consumer Price Index, ) Source: investing.com - Click to enlarge |

The Committee on Foreign Investment in the US sent a letter to Epic and Riot (the former owned by China’s Tencent, which also has a 40% stake in the latter) inquiring about the handling of personal data on Americans. Tencent shares sold off today in response. Meanwhile, ByteDance apparently has agreed to have a TikTok Global IPO in the US next year, and reports suggest that Beijing will go along with the deal. This case will likely be studied for years, especially if it becomes a precedent, but even as a one-off, the role of the US government is astounding.

The dollar has not been able to resurface above JPY105 today for the first time since late July. It edged a little closer to that end of July low near JPY104. With the official jawboning about the euro, and Brexit complicating sterling, the yen may have become the preferred way for short-term participants to express dollar bearish sentiment. The dollar has fallen every session this week against the yen, and the roughly 1.6% decline is the most in three months. With the $585 mln expiring option at JPY104.50 neutralized, the next focus could be on the JPY104 strike for $500 mln that is also expiring today. For its part, the Australian dollar has advanced for five consecutive sessions coming into today. It has risen by about 0.3% this week. Initial resistance is seen in the $0.7340-$0.7345 area. Although it has held above $0.7300 so far today, a break could see $0.7280. The dollar is lower against the Chinese yuan, reversing yesterday’s gain. It is the eighth consecutive weekly decline of the dollar. Its 1.1% decline this week is the largest since January 2019. The greenback broke below CNY6.80 this week and is finishing near CNY6.7575, the lowest since April last year. Our point is that it is not simply market forces, China’s current account surplus, and attractive yields. Chinese officials are not resisting strongly. They must see it in their interests to have a stronger yuan.

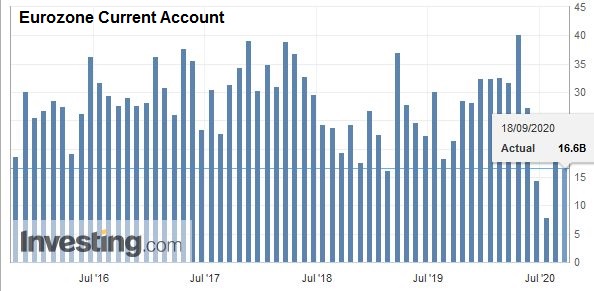

EuropeThere are two developments to note from the eurozone. First, three-month Euribor dipped below the ECB’s deposit rate (-0.5%), which should serve as the floor for short-term rates. However, those who do not have access to the ECB can be charged a premium and can drive down what banks are willing to lend to each other. There is also the expectation that the ECB decides to cut the deposit rate again later next year. The last time that three-month Euribor trade below the deposit rate was in August 2019 as the market anticipated a rate cut by the ECB to boost growth and inflation. Incidentally, for those who monitor the euro’s exchange rate closely, like the ECB, it was trading around $1.11-$1.12 then. Another consideration is the there has been a dearth of euro-denominated commercial paper that could have absorbed the excess liquidity, which has been compounded by the ECB’s 1.3 trillion euro in loans at a rate as low as 100 bp. That TLTRO accounts for more than a third of the estimated 3 trillion excess liquidity in the eurozone banking system. |

Eurozone Current Account, July 2020(see more posts on Eurozone Current Account, ) Source: investing.com - Click to enlarge |

Those banks that don’t seem to know what to do with their liquidity are being given more. Exercising its discretionary regulatory authority, the ECB declared exceptional circumstances to exclude central bank exposures from the leverage ratio calculations. This shaves the leverage ratio by about 0.3% to 5.36%. It does not sound like much, but it frees up an estimated 73 bln euros, which is a little bit more than what the ECB’s balance sheet has grown in the four-weeks through September 11. Many observers that talk about central bank policies being exhausted did not anticipate a TLTRO with a yield well below the deposit rate, nor do they consider the range of regulatory forbearance.

The Bank of England took another step to prepare for the possibility of negative interest rates. It will begin talks with Prudential Regulatory Authority in Q4 to see how negative rates may work. Sterling dropped a cent amid broad dollar gains to support near $1.2865. It rebounded against the dollar to approach $1.30 as the greenback shed it post-FOMC gains. It seems clear that if the BOE eases at its next meeting in November, it will not be ready to adopt negative interest rates, which just last month express concerns about the unintended negative consequences. Instead, a symbolic cut in the base rate from 10 bp to zero and more Gilt purchases are more likely.

The UK reported a 0.8% increase in August retail sales after a 3.7% increase in July. It is the fourth month that sales have increased. Excluding gasoline, retail sales rose by 0.6%. The government unveiled initiatives to encourage people to resume some of their usual activities. Of note, online purchases increased by 47%. There are two hurdles going forward. The first is the new outbreak of the virus. The second is the end of the furlough program that is scheduled to end next month.

The euro recovered impressively from yesterday’s post-FOMC drop to its lowest level in a month (~$1.1740) and set new highs late in the session a cent higher. It reached almost $1.1870 today. There is an option for one billion euros at $1.19 that rolls off today. When everything is said and done, the euro remains rangebound mainly as it has, for the most part, since the end of July between $1.17 and $1.19. Sterling also recovered smartly from the push to $1.2865, and it managed to reach almost $1.30 in the US afternoon. It is remains stalled near $1.30 in Europe today. A break of its looks likely and this would set up an immediate test on $1.3040. A move beyond that would target $1.3125.

America

The Fed’s balance sheet jumped by nearly $54 bln last week to $7.06 trillion, its largest since the end of June. Recall that it is buying roughly $20 bln a week of Treasuries and $10 bln a week of mortgage-backed securities. As others have noted, the Fed now owns more Treasuries than the other central banks put together, which is also true of the BOJ and JGBs. Foreign officials also bought around $7 bln of Treasuries last week, held in their custody accounts for foreign central banks. There is much talk in some circles about Asian central banks intervening in the foreign exchange market, and that is what it appears from one point of view.

On the other hand, foreign central banks had drawn down their Treasury holdings during the March-April chaos and have gradually moved to rebuild. The 10-year average holdings in the Fed’s custody account is $3 trillion. It is where it was at the end of February and is again approaching that now. Surely sovereign countries ought to be able to decide for themselves the level of self-insurance for which they are comfortable. Separately, reports suggest that the Federal Reserve will decide over the next two weeks whether to extend the cap on large bank dividends and share buybacks. These are not popular measures, of course, on Wall Street.

| The US reports leading economic indicators, the Q2 current account balance, and the University of Michigan’s preliminary September reading on consumer sentiment and inflation expectations. It will be the first survey of inflation expectations since the Fed’s new average inflation regime, which, as we have noted, seems to be akin to Volcker’s emphasis on the money supply. It gave Volcker cover to do what he wanted, which was to hike rates despite elevated unemployment. Similarly, the Powell Fed adopted the average inflation target to do what it wanted and to drive that message home that there will not be a rate hike any time soon. The Fed’s forecast no change in rates through 2023. The current account is expected to have deteriorated sharply from $104 bln in Q1 to around $160 bln in Q2. We anticipate the return of the “twin deficit” meme next year that in the past has been dollar negative. |

U.S. Current Account, Q2 2020(see more posts on U.S. Current Account, ) Source: investing.com - Click to enlarge |

Canada reports July retail sales. A gain of 1% is expected after the 23.7% surge in June. The risk may be on the downside. The greenback is virtually flat against the Canadian dollar, though it has slipped lower in four of the past five sessions coming into today. Recall that the US dollar snapped an eight-week slide against the Canadian dollar last week by rising almost 1% and finished near CAD1.3180. It is just below there now. Support has been carved in the CAD1.3120-CAD1.3130 area. A cap has been formed around CAD1.3240-CAD1.3250, which was successfully tested yesterday. The US dollar broke below MXN21.00 on Tuesday. It straddled that level yesterday and remains below it today. A weekly close below MXN21.00 would likely signal additional losses next week. On the topside above there, resistance is seen around MXN21.16.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, September 16: Dollar Eases Ahead of the FOMC

FX Daily, September 16: Dollar Eases Ahead of the FOMC

Overview: The dollar has been sold against nearly all the world’s currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors.

FX Daily, July 21: Europe and Tech Lift Risk Appetites

FX Daily, July 21: Europe and Tech Lift Risk Appetites

Overview: The continued domination of the tech sector and Europe’s tentative agreement are lifting equities and risk assets more generally today. Australia and Hong Kong’s 2.3%-2.5% rally led Asia Pacific markets. The Dow Jones Stoxx 600 is higher for a third session and above its 200-day moving average for the first time since February.

FX Daily, July 27: Dollar Slide Continues, while Gold Soars

FX Daily, July 27: Dollar Slide Continues, while Gold Soars

The US dollar’s dramatic sell-off continues. It is off against nearly all currencies. Among the majors, the Swedish krona and Japanese yen are leading the money, and the euro surged through $1.17. Emerging market currencies are fully participating, with the JP Morgan Emerging Market Currency Index posting its fifth gain in six sessions.

August Survey Data and Beyond

August Survey Data and Beyond

Economists are often lampooned because of their inability to forecast changes in the business cycle. But the pandemic helped them overcome the challenge this time. A record contraction in Q2 was anticipated before in March. Similarly, economists generally expected the recovery after the March-April body blow.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

News that the AstraZeneca Phase 3 test had to be stopped to study the adverse reaction of one subject added to the uncertainty of investors amid one of the more significant reversals of risk appetites since March. Equities continued to slump in the Asia Pacific region, with many large markets off more than 1%, led by Australia’s more than 2% decline.

FX Daily, September 11: Still Reluctant to take Euro above $1.19 but Sterling Remains Unloved

FX Daily, September 11: Still Reluctant to take Euro above $1.19 but Sterling Remains Unloved

Yesterday’s roller-coaster price action has not had much impact on today’s activity. The slide in US equities after early gains failed to prevent Japanese, Chinese, and Hong Kong equities from advancing, though other markets in the region were not as resilient.

FX Daily, September 17: Powell Lets Steam Out of Equities and Spurs Dollar Short-Covering

FX Daily, September 17: Powell Lets Steam Out of Equities and Spurs Dollar Short-Covering

Profit-taking after the FOMC meeting saw US equities and gold sell-off. The high degree of uncertainty without fresh stimulus did not win investors’ confidence. The Fed signaled rates would likely not be hiked for the next three years, and without additional measures, that appears to be the essence of the switch to an average inflation target.

Tags: #USD,$CNY,Brexit,ECB,Featured,federal-reserve,newsletter