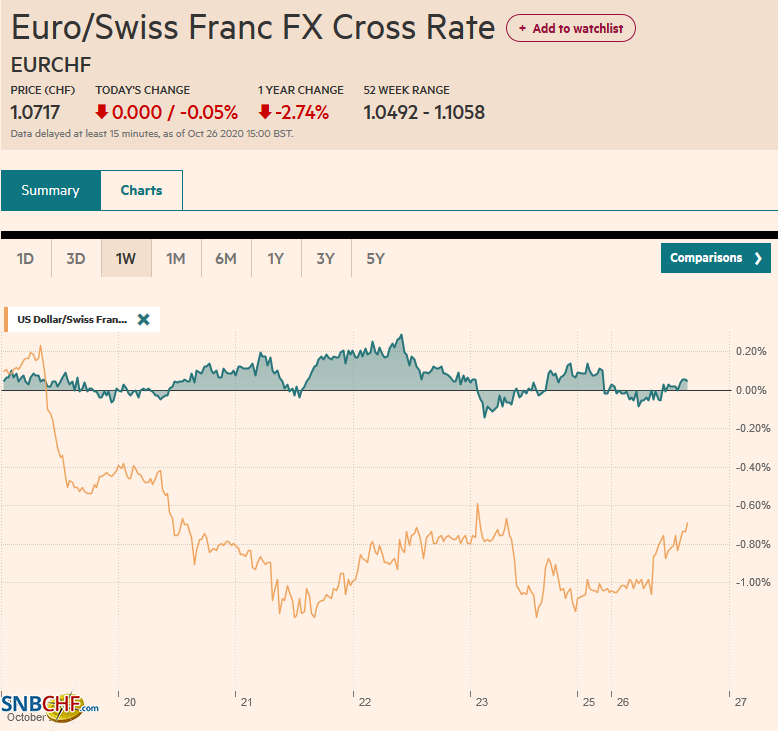

Swiss Franc The Euro has fallen by 0.05% to 1.0717 EUR/CHF and USD/CHF, October 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The surging virus ravaging large parts of Europe and the United States is fanning concerns over the economic implications as new social restrictions and curfews are announced in several countries. US additional fiscal support remains elusive as aid for states and local governments remains a bone of contention. Equities are under pressure. Most bourses in the Asia Pacific region fell, and a good part of last week’s gains have been given back. In Europe, the Dow Jones Stoxx 600 is off a little over 1% in late morning turnover after falling for the past two weeks. US shares are

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, Brexit, China, Currency Movement, Featured, Italy, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.05% to 1.0717 |

EUR/CHF and USD/CHF, October 26(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The surging virus ravaging large parts of Europe and the United States is fanning concerns over the economic implications as new social restrictions and curfews are announced in several countries. US additional fiscal support remains elusive as aid for states and local governments remains a bone of contention. Equities are under pressure. Most bourses in the Asia Pacific region fell, and a good part of last week’s gains have been given back. In Europe, the Dow Jones Stoxx 600 is off a little over 1% in late morning turnover after falling for the past two weeks. US shares are lower, too, and the S&P is around 0.7% lower. Declining equities and growth concerns are pushing yields lower. The US 10-year benchmark yield is off about three basis points to 0.81%. European peripheral yields are off 2-6 basis points, while the core is off 1-2 bp. The dollar is bid against most currencies today. Even the yen is weaker despite the risk-off mood. The decline in emerging market currencies is led by the 1% decline in the Turkish lira, against which the US dollar is at a new record high around TRY8.05. Gold continues to act as a risk asset and is struggling to maintain a foothold above $1900. Both supply and demand concerns are seen as negative for oil prices, and the December WTI contract, which tumbled 3% last week, is off another 3% today (~$38.70). |

FX Performance, October 26 - Click to enlarge |

Asia Pacific

As will likely be confirmed later this week, BOJ monetary policy will not change in the near-term, though officials will likely need to extend their emergency measures at some juncture in the coming months. Meanwhile, Prime Minister Suga is expected to signal a third supplemental budget next month, perhaps after Q3 GDP is reported (November 16). Talk is of a JPY10 trillion (~$95 bln) effort. However, there is still an estimated JPY7 trillion of undistributed funds from the earlier budget. These can be bundled into part of the new supplemental budget.

Before the weekend, the Trump administration claimed that China had met 71% of the agriculture purchases it had committed to in the Phase 1 trade deal. Many suspect a very generous view to tout success. It includes orders and shipments, which seems reasonable to the spirit of the agreement, if not the letter. Moreover, the government’s estimate apparently flattered by a multiplier to adjust for the fact that export sales account for about 80% of agriculture good exports. Separately, Bejing announced new unspecified sanctions on Boeing, Lockheed Martin, and Raytheon in retaliation for new arms sales to Taiwan.

Since the middle of last week, the dollar has not been above JPY105, but it looks poised to in North America today. That said, there is an option for almost $920 mln struck there that expires today. A little higher, in the JPY105.32-JPY105.35 band, another set of options for closer to $1 bln also expire today. Reports of the bottler Coca-Cola Amatil’s sale for A $ 9.23 bln may have blunted some of the pressure on the Australian dollar today, which is trading just inside the pre-weekend range. Support at $0.7100 held. There is an option for A$670 mln there that expires today. The dollar is rising against the Chinese yuan for the third session and briefly poked above CNY6.7 for the first time in a week. The PBOC set the dollar’s reference rate at CNY6.6725, roughly 1/1000 of a yuan stronger than most of the bank models anticipated.

Europe

There is some optimism over the UK-EU trade negotiations. The Irish Prime Minister and even the EU’s chief negotiator Barnier sounded upbeat. Macron recognized that French fishers will have less access to UK waters. Even if a last-minute agreement is struck, British industry and truckers still woefully unprepared. The magnitude of the disruption may be correlated with the decibel of the mutual recriminations by business and the government.

S&P affirmed at BBB the sovereign rating for Italy, one notch above Moody’s and Fitch’s assessment. It cited the pro-growth dynamics and ECB bond-buying. A year ago, some of the doomsayers claimed that only the ECB was buying Italian bonds. If it was true, then is it not true now. Japanese institutional investors were buying record amounts of Italian bonds over the summer. Italy has been running primary budget surpluses (excludes debt servicing costs) and has starved. Government fiscal efforts are earmarking health care and support for families. Ironically, S&P seems a little more optimistic than the government. S&P warns the economy may contract 8.9% this year and expand by 6.4% next year. The government’s baseline projection is for a 9% contraction, followed by a 6% expansion.

The German IFO survey results reflected the concerns about the second wave of the virus. Expectations softened to 95.0 from a revised 97.4 (initially 97.7), while the current assessment edged higher (90.3 from 89.2). This left the overall assessment of the business climate softer at 92.7 from 93.2 (initially 93.2). It is the first decline since April. At the end of last week, Markit reported that Germany’s preliminary composite PMI slipped to 54.5 from 54.7, as services, which moved below the key 50-level even while manufacturing expanded. While many critics of China note that its large trade surplus means that it is taking the aggregate demand of others, it does not apply to Germany, which exports to China appear robust.

The euro is heavy within the range seen before the weekend. Then it recovered from nearly $1.1785 to close near session highs around $1.1860. There has been no follow-through buying, and it found some support in early European turnover in front of $1.1800, where an option for around 525 mln euros will expire today. For its part, sterling remains in the range set in the middle of last week (~$1.2940-$1.3175) as UK-EU talks formally resumed. Sterling traded below $1.30 for the first time in three sessions today and found some bids in the European morning. The euro-sterling cross is attracting much interest. The euro is being pushed lower after testing the GBP0.9100 at the end of last week and today. An option for about 565 mln euro rolls at GBP0.9100 rolls off today. There are options for around 3 bln euros in the GBP0.9000-GBP0.9018 area that also expire today. Initial support is sen in the GBP0.9040-GBP0.9060 area.

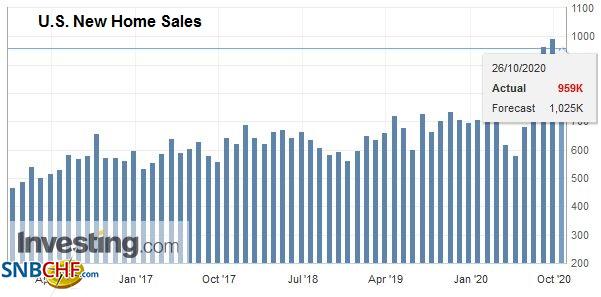

AmericaThe week’s highlight is the first report of Q3 GDP, which is widely touted to have surged after the collapse in Q2. However, today the US reports existing home sales. Housing has recovered sharply. New home sales were reported last week and are at their best level since 2006, rising more than economists anticipated. The US reports the Chicago Fed’s national economic activity indicator. It is not typically a market mover, but it is expected to be consistent with other data pointing to a slowing here in Q4 after historic Q3 activity. There are two highlights of the Canadian economic diary this week. The first is the Bank of Canada’s meeting on Wednesday. No change of monetary policy is expected, and it has already tempered some of its emergency efforts as market conditions have stabilized. Ahead of the weekend, Canada will report August GDP. The pace seen in July (3.0%) will not be duplicated, but a monthly increase of a little less than 1% is consistent with a strong Q3 performance (~45% at an annualized rate after contracted almost 39% in Q2). Separately, note that the NDP, which has given support to Trudeau’s minority Liberal government, extended its hold on British Colombia in weekend elections. Separately, Alberta is planning on ending the reduction of its oil output. |

U.S. New Home Sales, September 2020(see more posts on U.S. New Home Sales, ) Source: investing.com - Click to enlarge |

Mexico reports its September trade balance tomorrow. The record trade surpluses of July and August are unlikely to be repeated. At the end of the week, Q3 GDP is due. The median forecast in the Bloomberg survey calls for nearly 12% quarterly expansion after a 17.1% contraction in Q2. While the peso is up a little more than 5% this month, the Brazilian real is virtually flat. The central bank meets this week and is not expected to change the Selic rate. At 2%, it is already below measured inflation. The real is the weakest currencies in the world this year. It is off a little more than 28%, about two percentage points more than the Turkish lira and about five percentage points more than the Argentine peso. The Mexican peso, in contrast, has a net loss of a little less than 10%.

The much-awaited US Treasury report about the currency and trade practices of other countries will be delayed until after the election. It was roughly on an April and October respected mostly in violation, so a delay is not really surprising. From 1994-2019, the US did not cite a country as a currency manipulator. China was cited last year, though even many critics of Bejing did not think it was appropriate, and earlier this year reversed itself. Ironically, a few months on, and despite the steady appreciation of the yuan, the inability to reconcile the Chinese balance of payments data has prompted new concerns that it is manipulating its currency. More broadly, the policy has not proven effective, though it has not stopped efforts to implement and enforce it. Nearly a third of the G20 and two of the G5 are on the Treasury’s watchlist. The US Treasury cites Germany and Ireland, but they share a common central bank and currency policy as the other 17 members of the monetary union because of their external surpluses. As the Commerce Department is using a Treasury-developed model of exchange rates to determine the subsidy Vietnam gives to tire makers. Vietnam is a beneficiary of the US-China trade tensions as some production has moved there. Vietnam is a very poor country. Its GDP per capita is 1/25 of the US. It bought about $10 bln of Treasuries last year. Surely that did not add in any measurable way to the low-interest rate or disinflationary forces on the $21+ trillion economy.

The US dollar drifted lower against the Canadian dollar last week but is recouping it today as it approaches CAD1.3200. It is above this month’s downtrend that comes in today around CAD1.3160. The near-term potential extends toward CAD1.3240. The greenback closed on its lows against the Mexican peso ahead of the weekend (~MXN20.8550) but has popped back today and is knocking on the last session’s high near MXN21.04. The risk-off environment and the firm US dollar could see MXN21.10-MXN21.20.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, September 16: Dollar Eases Ahead of the FOMC

FX Daily, September 16: Dollar Eases Ahead of the FOMC

Overview: The dollar has been sold against nearly all the world’s currencies ahead of what is expected to be a dovish Federal Reserve, even if no fresh action is taken. The Scandis and Antipodean currencies are leading the majors.

FX Daily, October 9: Animal Spirits Return

FX Daily, October 9: Animal Spirits Return

Overview: The on-again-off-again fiscal stimulus in the US is back on as the White House now supports a broad stimulus program, but not as big as the Democrats $2.2 trillion package. It is the narrative being cited as the rebuilding of risk appetites is the wobble earlier in the week.

FX Daily, October 14: UK Blinks on Threat to Walk Away on Eve of EU Summit

FX Daily, October 14: UK Blinks on Threat to Walk Away on Eve of EU Summit

Overview: Turn around Tuesday saw the dollar bounce, particularly against the Australian dollar and European currencies, among the majors. Sterling pared earlier losses on reports that the UK would not walk away from the talks just yet, while the euro remains on its back foot.

FX Daily, October 15: Markets Shake and Dollar Goes Bid

FX Daily, October 15: Markets Shake and Dollar Goes Bid

A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off.

FX Daily, October 20: Narrowly Mixed Markets as Clearer Direction Sought

FX Daily, October 20: Narrowly Mixed Markets as Clearer Direction Sought

The capital markets lack a clear direction today. This is reflected in narrowly mixed equities, bonds, and currencies. The spreading contagion is giving rise to new economic concerns, among other things, and the UK-EU talks are struggling to resume, while Pelosi-Mnuchin talks in the US continue to drag.

FX Daily, October 22: Greenback Stabilizes

FX Daily, October 22: Greenback Stabilizes

Two sets of talks have riveted attention, and both appeared to have made progress yesterday. After some words, the EC, recognizing the importance of UK sovereignty, UK Prime Minister Johnson signaled a resumption of trade talks.

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

FX Daily, July 22: Pang of Uncertainty Spurs Profit-Taking

The optimism among investors appears to have evaporated in the face of new US-Chinese tensions, possible delays in the next US fiscal stimulus, and new record virus infections in Australia and Hong Kong. US stocks had pared early gains yesterday, and the high-flying NASDAQ finished lower after setting new record highs.

Tags: #USD,$CNY,Brexit,China,Currency Movement,Featured,Italy,newsletter