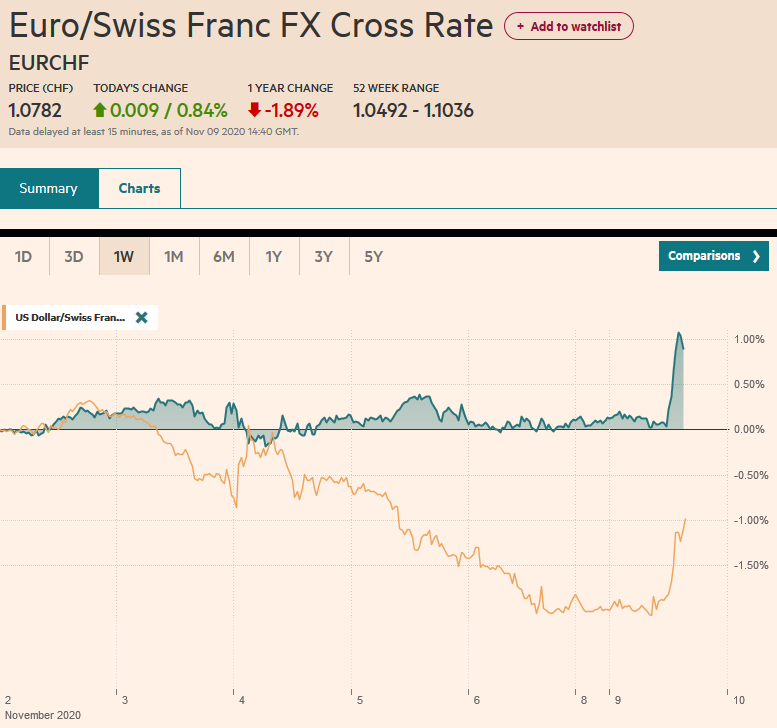

Swiss Franc The Euro has risen by 0.84% to 1.0782 EUR/CHF and USD/CHF, November 9(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge Overview: The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia. The Nikkei, which posted its highest close before the weekend in almost 30 years, rallied another 2.1% today. The Dow Jones Stoxx 600 in Europe is up around 1.5% today, led by the information technology, industrials, and consumer discretionary sectors. US stocks are firm, and the S&P 500 is poised to gap higher. Benchmark 10-year yields are lower. The 10-year

Topics:

Marc Chandler considers the following as important: $CNY, $TRY, 4.) Marc to Market, 4) FX Trends, China, Currency Movement, EU, Featured, Mexico, newsletter, Turkey, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.84% to 1.0782 |

EUR/CHF and USD/CHF, November 9(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

| Overview: The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia. The Nikkei, which posted its highest close before the weekend in almost 30 years, rallied another 2.1% today. The Dow Jones Stoxx 600 in Europe is up around 1.5% today, led by the information technology, industrials, and consumer discretionary sectors. US stocks are firm, and the S&P 500 is poised to gap higher. Benchmark 10-year yields are lower. The 10-year Treasury yield is softer at about 0.80%. European yields are mostly 1-3 bp lower, though Moody’s upgrade of Greece before the weekend has seen Greek bonds rally strongly. The 10-year yield is off 7 bp to 0.73%. Its two-year yield is minus seven basis points. China’s 10-year yield rose a few basis points to nearly 3.23%, a new high for the year. The dollar was weaker against nearly all the world’s currencies, but the gains against the European complex and the yen have been unwound. The Antipodeans and Scandis lead the major currencies, while the new central banker in Turkey has seen the lira rally strongly. JP Morgan’s Emerging Market Currency Index is up for the fifth consecutive session. Gold is extending last week’s nearly 4% advance. It is consolidating at reaching $1965. Crude oil is firm, perhaps underpinned by the softer greenback, but it remains inside the pre-weekend range. |

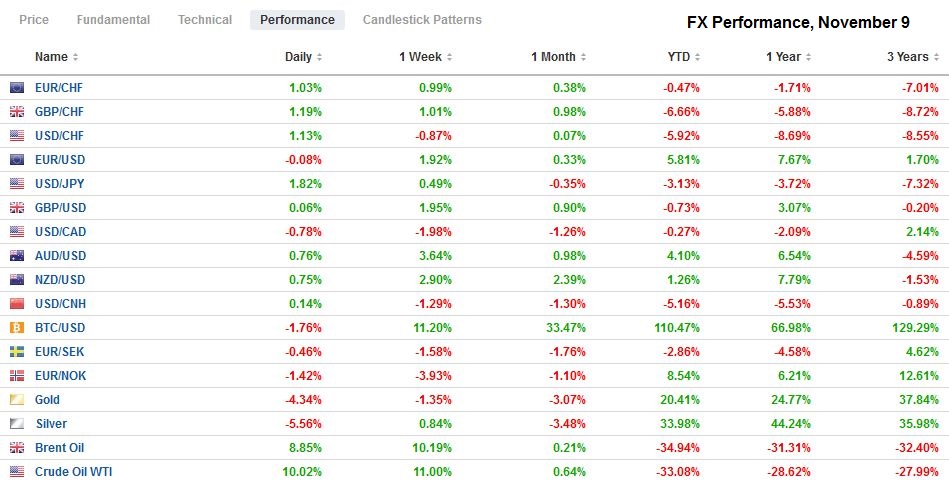

FX Performance, November 9 - Click to enlarge |

Asia Pacific

China reported its October trade and reserve figures over the weekend. Exports surged, and imports plunged, resulting in a larger trade surplus. Exports rose the fastest in 19 months. The 11.4% year-over-year increase follows the 9.9% increase in September. A Reuters poll found a median forecast for a 9.3% gain. Imports slowed to 4.7% year-over-year, half of what was expected in the Reuters survey and down from 13.2% in September. As a result, the trade surplus jumped to $58.4 bln from $37.0 bln. Despite the overall decline in imports, China boosted the import of US goods (32.9%) ostensibly to fulfill its obligations under the Phase 1 trade deal. Exports to the US have increased by 22.4%. The war camp that objects to nearly everything China does, including when they release their data, argues that the trade surplus means that China is “stealing” the aggregate demand of others. China imports $2 trillion of the world’s product, and many emerging market countries and industries rely on it. But look at its exports too. The largest increase this year was medical gear (43%). Here China is not hurting world growth. It is not replacing Europe, the US, or others’ domestic output. That train left the station many years ago. It is now providing medical devices and medicines that Europe and the US no longer produce. Electronic exports, including the new iPhone, also increased. Many foreign producers use China as an export platform. China suffered a large protein shortage. Its meat imports have risen by 75%, and grain imports are up over a fifth. Cosmetic and toiletry imports rose by more than a quarter.

Taiwan also reported strong trade figures. Its October exports rose 11.2% from a year ago, well above the median Bloomberg forecast anticipated after a 9.4% increase in September. Imports were off 1%, less than half the decline expected, and follows a 5.4% decline in September. The overall trade balance rose to nearly $7.5 bln, a new record, from $7.1 bln. Export to China and Hong Kong rose almost 17%, while exports to the US rose by 21.4%. Electronic exports were stronger though officials said that the delayed launch of the iPhone helped boost exports. Taiwan Semiconductor Manufacturing Company said it was struggling to meet demand. The new 5G smartphones require 30%-40% more chip content than 4G phones. We note that South Korea also report strong exports in October, helped by autos and semiconductor chips.

The dollar held the pre-weekend low just below JPY103.20 against the yen and recovered to test the pre-weekend high near JPY103.75. Tomorrow, there is a $1.5 bln option at JPY103 and another for $1.1 bln at JPY103.75 that expire. The intraday bounce appears to have stretched the momentum indicators. A week ago, the Australian dollar slipped below $0.7000, and today it briefly traded at $0.7300 for the first time since late September. Support is now seen in the $0.7240-$0.7250 area. The PBOC set the dollar’s reference rate at CNY6.6123, which was slightly weaker than expected. The greenback gapped lower and fell to CNY6.5640 before stabilizing around CNY6.58. Softening of Hong Kong’s interbank rate (one-month HIBOR is at its lowest level since 2011), reducing its premium over the US (~ four basis points) to the narrowest in a year appears to be helping take pressure off the Hong Kong dollar, after the authorities have spent almost $50 bln to cap it against the US dollar.

Europe

Faced with a collapsing currency, Turkey’s President Erdogan fired his handpicked central bank governor and appointed a new one, Naci Agbal, who has been heading up the President’s budget office. Agbal is a critic of the policies of Albayrak, the Treasury and Finance Minister, who is Erdogan’s son-in-law. Erdogan’s only concession appears to have made is to allow Albayrak an ostensible face-saving gesture or resigning for health reasons. A driving force behind the lira’s 30% devaluation is the central bank’s politicization and unorthodox monetary policy. The previous CBRT governor Uysal was about 16 months into what was a four-year term. Ironically, the fact that he was fired by Erdogan further validates the bear’s argument. Still, the bears fear that a new policy regime will be announced, and the lira jumped around 2% in early Asia and extended the gains in the European morning. After settling before the weekend near TRY8.5150, the dollar fell to almost TRY8.07 in European turnover. Credit default swap prices also fell. The central bank meets next on November 19.

Before the weekend, Moody’s affirmed Italy’s sovereign credit rating at Baa3, which is equivalent to Fitch’s BBB- and one notch below S&P’s BBB assessment. It was not surprising. However, what may catch some off-guard was Moody’s increase in Greece’s rating to Ba3. That is the same now as S&P’s BB- and one notch below Fitch’s. Greece’s upgrade conveys little new information as Moody’s was the outlier previous.

The EU trade ministers meet today and were expected to go forward with putting tariffs on $4 bln of US goods that allowed by the WTO for improper assistance to Boeing. A wide range of industrial and consumer goods are targeted. The US, which has not used the full authority that the WTO granted it ($7.5 bln), has threatened to retaliate if Europe went forward. This will deliver President-elect Biden a fait accompli. It poses a hurdle to resolve this two-decade-old problem. It underscores our argument that despite the apparent rancor, there seems to be bipartisan displeasure with Europe on a range of issues: Nord Stream, II pipeline, the digital tax that France says it will begin collecting next month, contributions to NATO, the large and sustained current account surplus, and the unwillingness to confront China more forcefully. Germany is advocating delaying the decision as an act of good faith.

The euro reached almost $1.19, where a 3.1 bln euro option is set to expire today. It is consolidating at little changed levels (~$1.1875) in the European morning. Nearby support is in the $1.1850-$1.1860 area. It had gained in the last four sessions last week, which ended a six-session slide. Through November 9, the speculators in the futures market had reduced the net long euro position for the sixth consecutive week by a cumulative 50k contacts or nearly a quarter. Sterling showed a similar pattern. Its recent gains were extended to almost $1.32, its best level in two months, but has also stalled in the European morning. Support is seen near $1.31, where a GBP460 mln option will roll-off today. The UK-EU trade talks resume today. The EC President von der Leyen and UK Prime Minister Johnson spoke over the weekend and reaffirmed the November 15 deadline.

America

Even though Biden was projected to be the winner, the subsequent legal drama is commanding attention. The markets seemed to have assumed this ahead of the weekend. The Democratic Party has won the popular vote in seven of the last eight presidential contests. However, the general takeaway seems to be that Trump was defeated, but the Republican Party did better than the President. It won back seats in the House of Representatives, which it had lost in 2018. The Republicans also won in many state legislatures, which will impact the redrawing of districts following this year’s census.

With last week’s FOMC meeting done and dusted, we will hear from a number of Fed officials this week. Mester and Kaplan get the ball rolling today, but the week’s highlights include Governor Brainard tomorrow, who is widely seen as a candidate for Treasury Secretary in a Biden administration, and Chair Powell, who speaks at an ECB’s confab on Thursday.

The US economic calendar is light until Thursday’s CPI report. However, tomorrow’s JOLTS report will shed more light on the labor market after the October employment report was stronger than expected. Canada has a sparse economic calendar this week. Mexico is a different story. Today’s CPI report is expected to show a small gain on the year-over-year rate, inching further above the 2-4% target range. September industrial production figures are due in the middle of the week, ahead of the central bank meeting on November 12. The peso’s strength and lack of much fiscal support put more of the burden on monetary policy, and Banxico is expected to deliver a 25 bp rate cut on Thursday that would bring the overnight target to 4.0%.

The greenback fell by 2% against the Canadian dollar last week. It was the largest decline in five months. There has been follow-through selling today, and it is within spitting distance of CAD1.30. The September 1 low was a smidgeon lower. The low for the year was set on January 7, near CAD1.2955. The intraday technicals warn of the risk of some consolidating in North America, especially in the early going. The US dollar fell 2.7% against the Mexican peso last weekend, and follow-through selling saw it fall below MXN20.50 today for the first time in eight months. That area should now serve as resistance. The next important technical target is MXN20.00.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 28: Dollar Bounces, Gold Slips, while Equities Hold Their Own

FX Daily, July 28: Dollar Bounces, Gold Slips, while Equities Hold Their Own

The main development in the capital markets today is the firmer dollar against nearly all the major and emerging market currencies. Among the majors, the New Zealand dollar and Swedish krona are the heaviest (~-0.4%), while the Swiss franc and yen are marginally lower.

FX Daily, October 19: Sterling Sparkles in Dollar Setback

FX Daily, October 19: Sterling Sparkles in Dollar Setback

Investors have not let the surge of the virus or uncertainty over the UK-EU talks or US fiscal stimulus to stand in their way. Sterling is leading the major currencies higher, returning to the $1.30 area, while global equities are trading higher.

FX Daily, October 27: Markets Take Collective Breath and Beijing Tweaks Fixing Mechanism

FX Daily, October 27: Markets Take Collective Breath and Beijing Tweaks Fixing Mechanism

The surging pandemic sapped the risk-taking appetites as some investors hunker down for what could be a volatile period ahead. The S&P 500 lost nearly 3% at its lows before rebounding 1% in late dealings.

FX Daily, May 11: Quiet Start to New Week

FX Daily, May 11: Quiet Start to New Week

Overview: The new week begins slowly in the capital markets. Many markets in the Asia Pacific region, including Japan, Hong Kong, and Australia, gained over 1%, but European and US shares are heavier. Benchmarks off all three regions rallied by 3.4%-3.5% over the past two weeks. Bond markets are also little changed, with the US 10-year benchmark just below 70 bp ahead of this week’s record refunding.

FX Daily, July 15: The Dollar Slumps and EU Court Rules in Favor of Apple

FX Daily, July 15: The Dollar Slumps and EU Court Rules in Favor of Apple

A recovery in US stocks yesterday, coupled with optimism over Moderna’s vaccine, is providing new fodder for risk appetites today. Equities are being driven higher, and the dollar is under pressure. Most equity markets in Asia advanced. China and Taiwan were exceptions, and, in fact, the Shanghai Composite fell for the second consecutive session for the first time in a month.

FX Daily, July 20: Markets Yawn, Deal or No Deal

FX Daily, July 20: Markets Yawn, Deal or No Deal

Overview: While there are signs that Europe has reached a compromise on the grant/loan issue, the spillover into the markets is quite limited. China, with Shanghai’s 3.1% gain, led a few markets in the Asia Pacific region higher, including Japan and India. Most markets were lower, and Europe’s Dow Jones Stoxx 600 is a fractionally firmer, recovering from initial losses.

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, September 24: Darkest Before Dawn

FX Daily, September 24: Darkest Before Dawn

The two recent market developments, push lower in stocks, and higher in the dollar is continuing. Tuesday’s gains in the S&P 500 and NASDAQ were unwound on Wednesday and this is helping drag global markets lower. The MSCI Asia Pacific Index fell for the fourth consecutive session today and many markets (India, Shenzhen, Taiwan, and Korea) fell more than 2% and most others were off more than 1%.

Tags: #USD,$CNY,$TRY,China,Currency Movement,EU,Featured,Mexico,newsletter,Turkey