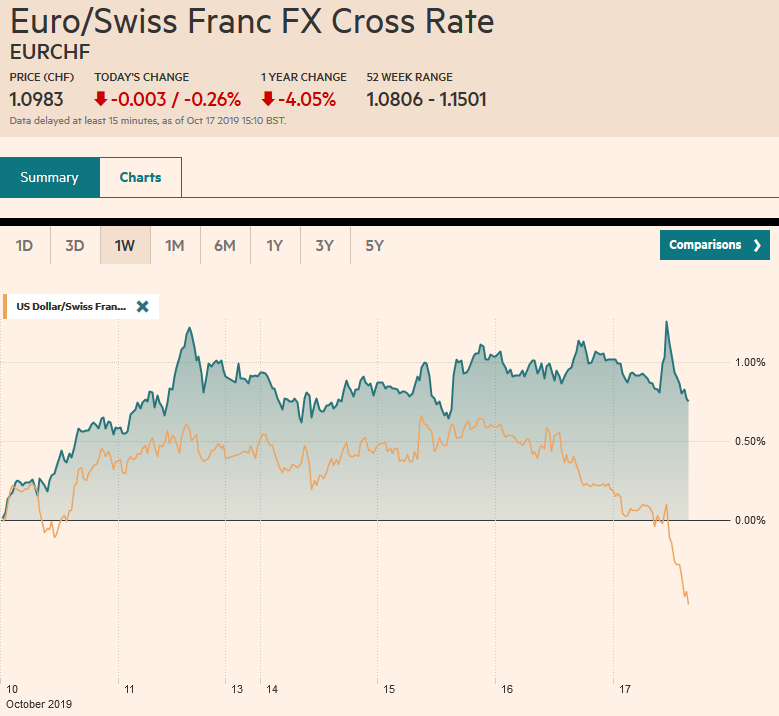

Swiss Franc The Euro has fallen by 0.26% to 1.0983 EUR/CHF and USD/CHF, October 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: A Brexit deal between the UK and the EU has been struck. Whether it can win Parliament’s approval is a horse of a different color. Meanwhile, US-Chinese relations continue to sour. The capital markets are narrowly mixed as investors await further developments. The MSCI Asia Pacific is consolidated after gaining for the past four sessions. Following a better than expected jobs report, that seemed to make a rate cut next month less likely, the Australian equities fell by 0.75% to lead the regional decline. European and US shares are little changed but slightly firmer. Benchmark

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brexit, Currency Movement, EUR/CHF, Featured, FX Daily, newsletter, U.S. Housing Starts, U.S. Industrial Production, U.S. Initial Jobless Claims, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.26% to 1.0983 |

EUR/CHF and USD/CHF, October 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A Brexit deal between the UK and the EU has been struck. Whether it can win Parliament’s approval is a horse of a different color. Meanwhile, US-Chinese relations continue to sour. The capital markets are narrowly mixed as investors await further developments. The MSCI Asia Pacific is consolidated after gaining for the past four sessions. Following a better than expected jobs report, that seemed to make a rate cut next month less likely, the Australian equities fell by 0.75% to lead the regional decline. European and US shares are little changed but slightly firmer. Benchmark 10-year yields rose in Asia and are mixed in Europe. UK Gilt yields have pushed lower, while Spanish bonds continue to underperform amid elevated political risk following the sentencing of rebels from Catalonia. That said, Spain’s 10-year bond auction was oversubscribed by the most since early last year (2.45x vs. 1.39x previously). Australia and New Zealand dollars are leading a move against the US dollar, though sterling is extending yesterday’s surge, and the euro has punched through $1.11. The Norwegian krone is extending its loss into record territory against the euro. Most emerging market currencies are edging higher against the greenback. Gold is little changed, while oil prices are unwinding most of yesterday’s gains following a surge in US inventories (10 mln barrels) estimated by API. |

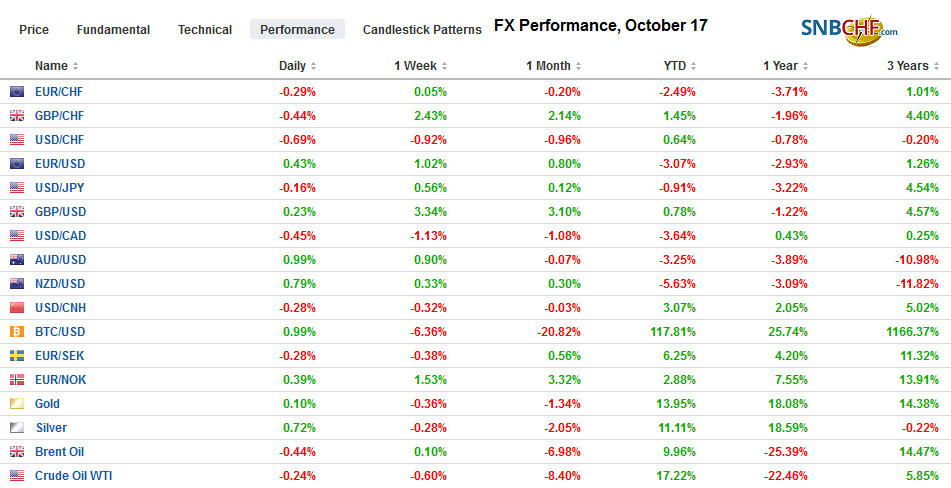

FX Performance, October 17 - Click to enlarge |

Asia Pacific

Australia reported a sufficiently strong employment report to give the market pause after moving to largely discount a rate cut next month. Job growth in September was close to expectations at 14.7k, but full-time positions rose 26.2k. The unemployment rate slipped to 5.2% from 5.3%, though there seemed like a function of the decline in the participation rate (66.1% vs. 66.2%). That said, underemployment and underutilization also eased.

Japanese press reports that the government will downgrade its overall economic assessment this month. It may be reluctant to blame the sales tax increase, but the destruction of the typhoon gives ample cover. This underscores the likelihood that the BOJ eases policy at the meeting at the end of the month, and Prime Minister Abe is likely to offer a supplemental budget.

The “fighting and talking” characterization of the US-China’s relations appears to be more the former and less the latter. Apparently, China, which the US claims needs a trade agreement more than it, has yet to invite Treasury Secretary Mnuchin to Beijing to lay the groundwork to finalize the “handshake” deal that the US dubbed “phase 1”. The US continues to find new ways to antagonize China. The latest moves include requiring Chinese officials to give prior notification of plans to universities, research centers, and local governments, which is what US officials are often required to do in China. The US Commerce Department has initiated a probe into glass container imports from China. The US Senate has indicated it will take up the bill that passed the House of Representatives that require annual confirmation that Hong Kong’s autonomy remains intact to ensure its special trade privileges (not subject to the tariffs that exports from the mainland face).

The dollar has been confined to less than a quarter yen range through the European morning. It continues to knock on the JPY109 level for the third consecutive sessions without penetration. The market appears to be absorbing the offers near there. Except for one spike on August 1, the dollar has held below JPY109 here in H2 19. The dollar is holding above yesterday’s low a little below JPY108.60. The 200-day moving average is a touch above JPY109.05, and the greenback has not traded above it in five months. The Australian dollar is up nearly 2/3 of a percent to test the upper end of its four-week range around $0.6800. It posted one leg up in response to the employment data and then took another step higher in the European morning. It appears to be running to option-related offers (real or anticipated) with some chunky expirations today. At $0.6800, there is an A$1.6 bln option, and at $0.6815, there is another A$1.1 bln option. On the downside, at $0.6775, a third option for A$1.3 bln also expires today.

Europe

Brexit remains the main talking point. A deal with the EU has been achieved. Northern Ireland will be allowed to scrap the border arrangement four years after the transition period, with a two-year notice of a new system. However, the Democrat Unionist Party from Northern Ireland, whose support some Tory MPs have said is essential for their support, has balked. The DUP had previously blocked efforts to put a hard border (i.e., customs check) between it and the rest of the UK. It is not clear Prime Minister Johnson will succeed in securing Parliament’s approval on a deal that seems likely to be struck with the EU. Although the path is not clear, we do not see how an extension past the end of the month can be avoided. PredictIt.Org shows only about a 20% chance that the October 31 deadline is respected.

Separately, the UK reported slightly better than expected September retail sales. The unchanged month-over-month headline figure beat the median forecast in the Bloomberg survey of a 0.2% decline, following the revised 0.3% fall in August (initially -0.2%). The year-over-year rate rose to 3.1% from 2.6%. Excluding petrol, retail sales rose 0.2% for a 3.0% year-over-year pace, up from 2.2% previously.

The euro broke above a four-month downtrend last week and come back to test it on Tuesday, near $1.0990. It recovered yesterday and is extending those gains today to push through $1.11 for the first time in a month. The next target is near $1.1145, which is also the (50%) retracement of decline since June. A move above $1.1210 area that houses the (61.8%) retracement and the 200-day moving average is needed to boost confidence that a low of some import is in place. Sterling has surged toward $1.30. The next important chart point is near $1.32. On the other hand, doubts that Parliament will approve the deal is encouraging some interest in selling into this rally.

AmericaWhat we are interested in is the strength of the US economy. That directs us to the consumer. Retail sales in September were softer than expected. They fell by 0.3% to post the first decline since February’s 0.5% drop. While we see the economy slowing, we would not want to read too much into the retail sales report, which covers a little more than 40% of US consumption and can be distorted by changing prices. There is only a modest correlation (<0.37) between the monthly change in the two time-series over the last several years, and it is clear from the Bloomberg chart here that retail sales tend to exaggerate the changes in consumption (month-over-month change in retail sales yellow line and change in personal consumption expenditures is the white line). Although some economists revised down Q3 GDP forecasts after the report, the retail sales provided fundamental cover for what they wanted to do in any event. The material basis for consumption remains strong. The two drivers of consumption, wealth, and income, continue to bode well. House and equity prices have risen, and more people are working and getting paid a little more. Consumer confidence is also elevated though off its peak. |

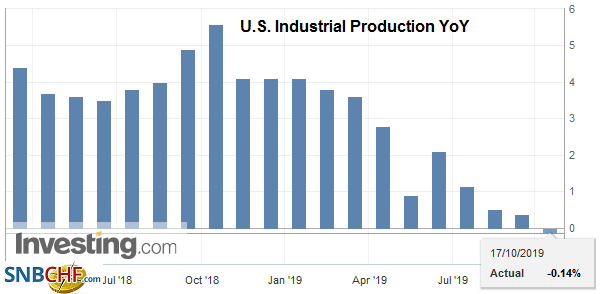

U.S. Industrial Production YoY, September 2019(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

| Repo market pressure was evident on Tuesday, and the Fed’s repo operation on Wednesday was oversubscribed for the first time since September 25. The demand for repo funding was greater than the supply the banks provided, perhaps due to the settlement of the Treasury’s recent auctions and the unwinding of trade positions after the three-day weekend. The demand for repo funding is not the same as demand for the dollar itself, which traded lower on Wednesday against most major end emerging market currencies. The Fed’s previously announced T-bill purchase plan was formally launched yesterday with a $7.5 bln buy. Some observers feared that there would not be sufficient sellers, but the banks offered to sell the Fed nearly $32.6 bln of bills. It is to buy $60 bln of bills by the middle of next month. We are concerned that increasing excess reserves may not be in itself sufficient to increase repo interest by the banks, which have moved away from it. A standing repo facility, the standing reverse repo facility, still remains likely. In addition to new offers for overnight repos, the Fed will conduct a term (15-day) operation today as well. |

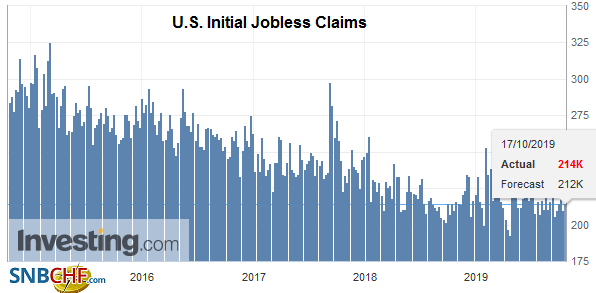

U.S. Initial Jobless Claims, October 2019(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

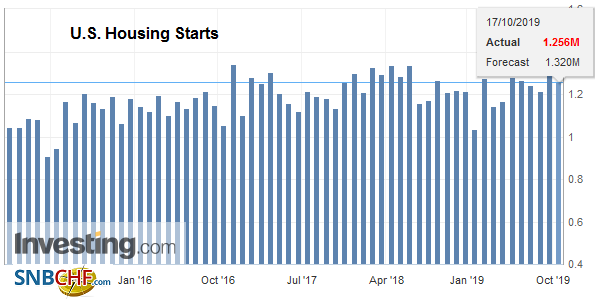

| The US economic calendar features housing starts and permits, industrial and manufacturing output, and the October Philadelphia Fed survey. All the reports are expected to show weakness sequentially. Barring significant upside surprises, the conclusion drawn from the softer inflation and expectations readings from last week, coupled with the disappointing retail sales report yesterday, solidify expectations for another Fed cut at the end of the month. |

U.S. Housing Starts, September 2019(see more posts on U.S. Housing Starts, ) Source: investing.com - Click to enlarge |

| After yesterday’s Canadian CPI figures, the market feels comfortable with the Bank of Canada’s neutrality, and today the softer US dollar tone is allowing the Canadian dollar firm to its best level in a month. The greenback is trading near CAD1.3160 and is approaching last month’s low near CAD1.3130. The dollar closed below its 200-day moving average against the Mexican peso on Tuesday (~MXN19.2570) for the first time in two and half months and has continued to move lower. The high real and nominal yields continue to attract carry plays, especially given the yen’s weakness. A break of MXN19.15 leaves little technical obstacles in front of MXN19.00. |

US Personal Consumption Expenditures Nominal - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,Currency Movement,EUR/CHF,Featured,FX Daily,newsletter,U.S. Housing Starts,U.S. Industrial Production,U.S. Initial Jobless Claims,USD/CHF