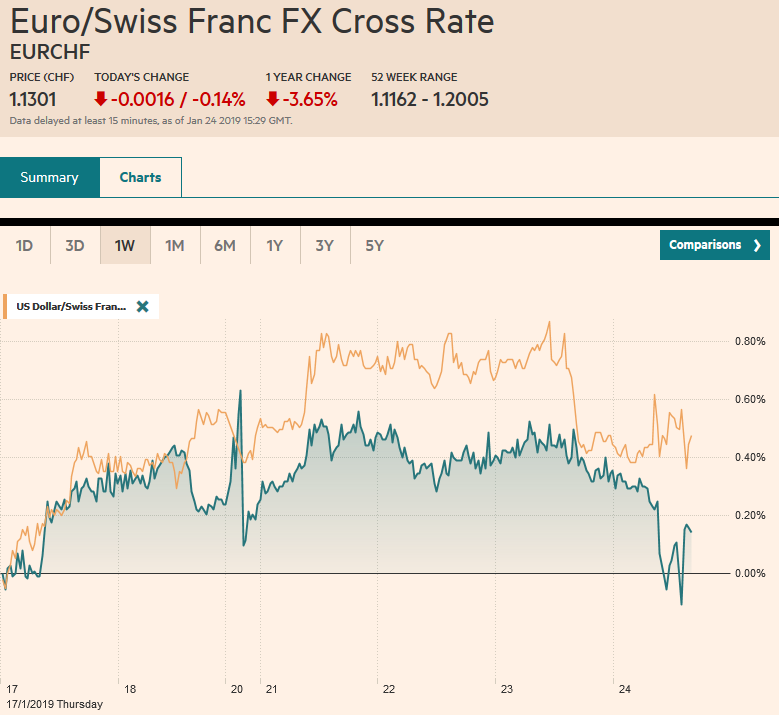

Swiss Franc The Euro has fallen by 0.14% at 1.1301 EUR/CHF and USD/CHF, January 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The eurozone’s preliminary composite PMI for January fell to its lowest level since July 2013. It reinforces expectations for a dovish Draghi press conference and saw the euro unwind yesterday’s gains. The US dollar is firmer against all the major currencies. Asian stocks gained, and the MSCI Asia Pacific Index snapped a two-day fall with the help of chipmakers, as SK Hynix boosted its dividend, Lam announced a share buyback program, and Xilinx forecast stronger sales. European bourses are also moving higher, trying to end a

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, Featured, GBP, JPY, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.14% at 1.1301 |

EUR/CHF and USD/CHF, January 24(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The eurozone’s preliminary composite PMI for January fell to its lowest level since July 2013. It reinforces expectations for a dovish Draghi press conference and saw the euro unwind yesterday’s gains. The US dollar is firmer against all the major currencies. Asian stocks gained, and the MSCI Asia Pacific Index snapped a two-day fall with the help of chipmakers, as SK Hynix boosted its dividend, Lam announced a share buyback program, and Xilinx forecast stronger sales. European bourses are also moving higher, trying to end a three-day drop, helped by information technology and financials. European benchmark 10-year yields are lower led by a three-four basis point decline in the periphery and one-two basis points in the core. US bonds and equities are slightly firmer. |

FX Performance, January 24 - Click to enlarge |

Asia Pacific

Japan’s flash manufacturing PMI fell to 50.0 from 52.6. It is the lowest reading since at least August 2016. The silver lining to the disappointing news is that it appeared to bolster demand at the 20-bond auction, which saw the bid-cover jump to 4.57x, the most since last summer. After contracting in Q3 18, mostly due to disruptions caused by natural disasters, the recovery in Q4 seemed lackluster, and 2019 is off to a soft start.

After hiking rates last November, Korea’s central bank left rates on hold (1.75%), but trimmed this year’s growth forecast (2.6% vs. 2.7%) and cut the CPI forecast to 1.4% from 1.7%. The central bank seemed to signal a reluctance to reduce rates, implying perhaps a reliance on fiscal policy.

Australia reported it grew 21.6k jobs in December, a bit more than expected and the unemployment rate ticked back down to 5.0%. However, this is where the good news ends. Full-time jobs fell by 3k after a 7k fall in November. This is the first back-to-back decline in August-September 2016. The participation rate slipped to 65.6% from 65.7%. The CBA manufacturing PMI rose (54.3 vs. 54.0), but the services fell (51.0 vs. 52.7). The composite dropped to 51.5 (from 52.9), which is the lowest since at 2.5 years. On top of this, one of Australia’s largest banks raised the variable mortgage rate (~12-16 bp), matching what the other major banks did at the end of Q3 18.

The dollar rose to JPY110 yesterday, the highs for the year. It is consolidating today. There is a JPY110 option for about $400 mln that expires today and nearly $1 bln at JPY109.40-JPY109.50. Above JPY110, there is a retracement target near JPY110.30. The Australian dollar is posting a big outside down day (trading on both sides of yesterday’s range) and breaking below $0.7100 for the first time since January 4. An option struck there (~A$540 mln) that expires today is still in play. The next technical target is near $0.7050. The Chinese yuan is virtually unchanged with the greenback near CNY6.79.

Europe

The ECB meeting is the main focus. After the disappointing flash PMIs, there is more talk about Draghi more formally recognizing that the balance of risks has shifted to the downside. We are still are reluctant to go that far. The ECB has only changed its risk assessment with fresh staff forecasts. A changed risk assessment would also seem to require a policy response. It is not clear that the Executive Board is prepared to do so quite yet. The euro fell every day the ECB met last year except in September. Draghi is expected to be dovish and much seems to have been discounted. As we have suggested, we look for the market’s focus to shift from the ECB to the US, where next week the FOMC meets (patient and flexible–i.e. not rate hike until at least mid-year and no predetermined course) and jobs data at the end of the week that “normalizes” after the large jump in December). We expect the euro to begin recovering from the lower end of its two-three month range.

The PMIs were poor. German manufacturing PMI slipped below the boom/bust 50 level (49.9 from 51.5). The service PMI rose to 53.1 from 51.8. This allowed the composite to edge higher and at 52.1 is a two-month high. France was the opposite. Manufacturing rose improved from 49.7 to 51.2. This was more than offset by the slump in services to 47.5 from 49.0. The composite fell to 47.9, a four-year low. Outside of the two largest economies, the Markit survey found output growth slowed to its lowest level since November 2013. Italian figures won’t be out until early February, but it plays on fears that the Italian economy may have contracted in Q4 18 after slumping in Q3. For the euro area as a whole, both manufacturing and services fell, and the composite eased to 50.7 from 51.1, the lowest since July 2013.

Growing confidence that Brexit will be delayed from the end of March saw sterling approach $1.31 today after shooting above $1.30 yesterday. News that the government’s International Trade Secretary Fox, one of the cabinet’s leading Brexiters signaled a potential delay was seen as a sign that Prime Minister May is also moving in that direction. Apparently, Labour and other opposition parties already have done so. While a postponement eases the sense of urgency, some fear it extends the uncertainty, which weighs on the economy.

Norway’s central bank left rates steady at 75 bp. Although it signaled it may still raise rates again, as early as March, it recognized the high degree of uncertainty. The market is pricing in one hike for the Norges Bank this year, while policymakers seem to signal two. The next monetary report will be delivered on March 21. Economic forecasts will be updated then. The krone strengthened against the euro to its best level since mid-December.

It is the third session that the euro has not risen above $1.14. There are almost 2 bln euros in options at $1.1400-$1.1405 that expire today. The euro is holding above this week’s low near $1.1335. The low for this month has been about $1.1310, which is where the lower Bollinger Band (two standard deviations for the 20-day average) is found. We had thought last week’s high for sterling ($1.30) had exhausted the move, but it reached almost $1.3100 yesterday and is consolidating today. Although $1.30 was resistance, it is unlikely to act as much support. There is an option for GBP433 mln struck there that expires today. The euro slipped below GBP0.8700 for the first time since mid-November today, and the downside momentum eased. Initial resistance is seen near GBP0.8720.

North America

Two votes in the US Senate ostensibly that could lead to the end of the partial government shutdown will be held today. The biggest risk is that neither bill passes. There might be some response to the headline, but the failure of both bills would indicate there is not a majority for either “extreme” position and it would point in the direction of a compromise.

Separately, Markit reports its flash PMI readings for the US. They are expected to be a little softer. The Leading Economic Indicator for December is expected to have slipped by 0.1% after a 0.2% increase in November. The partial government shutdown is shaving US growth by a little more than 0.1% a week according to most estimates.

Canada’s larger than expected fall in retail sales yesterday (-0.9%), the largest decline since April fans fears that the economy may have contracted in November. The November GDP will be reported next week. Monthly GDP contracted in September before recovering in October. The US dollar is testing yesterday’s high near CAD1.3355, which is also the greenback’s best level since January 7. The CAD1.3365 area corresponds to a retracement objective and the 20-day moving average. A move above there would target CAD1.3420-CAD1.3450.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,$AUD,$CAD,$EUR,$JPY,Featured,newsletter