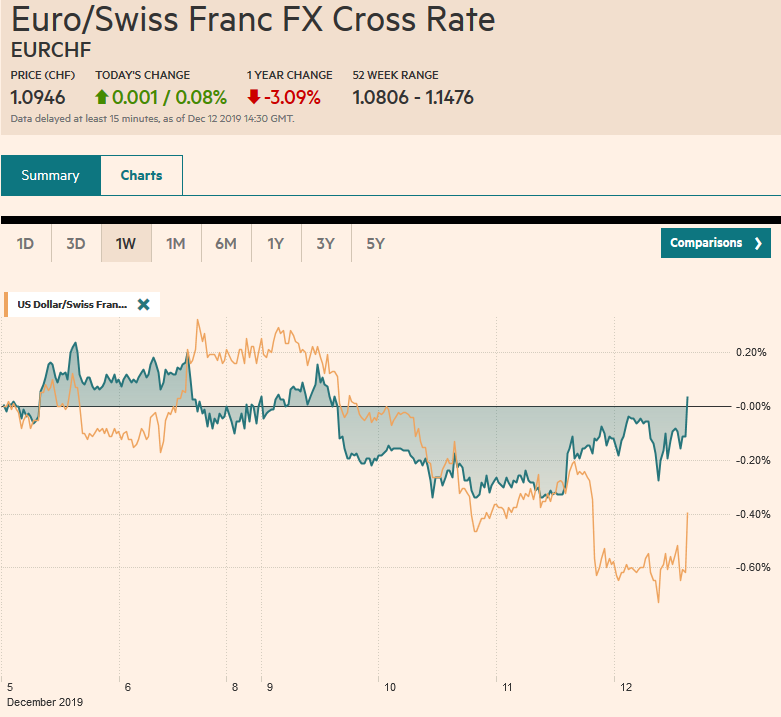

Swiss Franc The Euro has risen by 0.08% to 1.0946 EUR/CHF and USD/CHF, December 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.comeur - Click to enlarge FX Rates Overview: With the FOMC meeting delivered no surprises, attention turns to the ECB meeting as the UK go to the polls. Lagarde will hold her first press conference as ECB president today, and it will naturally command attention. Equities are advancing today, and tech appears to be leading the way. In Asia Pacific, Taiwan and South Korea rallied more than 1%, while the Hang Seng gapped higher to almost its best level in three weeks. Europe’s Dow Jones Stoxx 600 is up for the second consecutive session, and it is being led by information technology. US shares are trading firmer after the

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brazil, Currency Movement, ECB, EUR/CHF, Eurozone Industrial Production, Featured, Federal Reserve, FX Daily, Germany Consumer Price Index, India, newsletter, Turkey, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.08% to 1.0946 |

EUR/CHF and USD/CHF, December 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.comeur - Click to enlarge |

FX RatesOverview: With the FOMC meeting delivered no surprises, attention turns to the ECB meeting as the UK go to the polls. Lagarde will hold her first press conference as ECB president today, and it will naturally command attention. Equities are advancing today, and tech appears to be leading the way. In Asia Pacific, Taiwan and South Korea rallied more than 1%, while the Hang Seng gapped higher to almost its best level in three weeks. Europe’s Dow Jones Stoxx 600 is up for the second consecutive session, and it is being led by information technology. US shares are trading firmer after the S&P gained about 0.3% yesterday. Bond yields are mostly lower, though some in the European periphery are sticky, and the US 10-year yield has edged back above 1.80%. The dollar is soft but mostly consolidating the post-Fed drop. Emerging market currencies are mostly firmer, and if the JP Morgan Emerging Market Currency Index holds on to its minor gains, it would be the eighth advancing session in the past ten. Gold’s three-day rally is at risk as the upper end of the $1450-$1475 holds. Oil prices are little changed, and the January WTI contract continues to straddle the $59 a barrel level. |

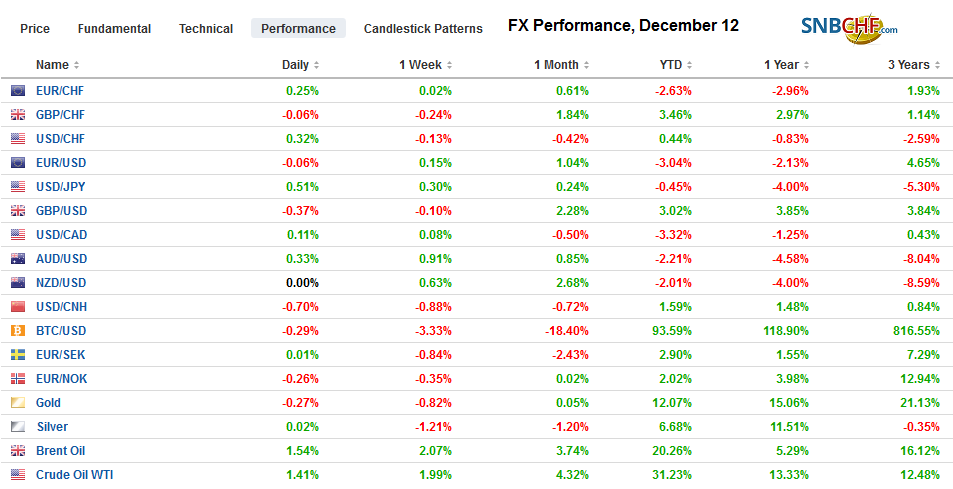

FX Performance, December 12 - Click to enlarge |

Asia Pacific

President Trump is to meet with his team today to discuss the tariffs threatened for December 15. The conflicting signals from the officials may be designed to keep pressure on Beijing. However, the market appears to assume, for the most part, that new levies will be delayed. This means that the implementation would likely elicit a more dramatic response than the suspension. It is also not clear when the announcement will be made. Some expect it as early as today, but the risk is that the official word is not made until after the markets close tomorrow.

Japan’s October core machinery orders plunged 6%. It is the fourth consecutive monthly decline and shocked economists. The median forecast in the Bloomberg survey called for a 0.5% gain. The year-over-year contraction deepened to -6.1% from a 5.1% gain in September. This underscores the weakness in capex, which also will likely be reflected in tomorrow’s Tankan Survey. The world’s third-largest economy appears to be contracting by around 2.7%-3.0% this quarter at an annualized pace.

India’s inflation is due shortly. It is expected to have accelerated to 5.3% in November a three-month high, from 4.6% in October. Over the last seven sessions, the 10-year benchmark yield has risen by about 30 bp to about 6.77%. S&P warned yesterday that it may reduce India’s credit rating (BBB-) unless growth improves. A move by S&P would take away India’s investment-grade status. Moody’s rates India a notch above S&P but adopted a negative outlook last month.

The dollar remains mired in an extremely narrow trading range against the yen. This week’s range so far has been about JPY108.45 to JPY108.85. There are two expiring options to note. One is at JPY108.70 for around $450 mln, and the other is at JPY109 for almost $390 mln. The Australian dollar is building on yesterday’s nearly 1% gain, the largest in two months. It tested $0.6800 on Tuesday and is nearing $0.6900 today. There is an option stuck at $0.6875 for about A$575 that will be cut today. The 200-day moving average that has turned back counter-trend rallies this year is found near $0.6910. China’s yuan continues to move sideways in narrow ranges. For the fourth session, the net change is less than 0.1%.

EuropeThere is a sense of great continuity between Draghi and Lagarde. The obvious comparison is Bernanke and Yellen. However, that continuity puts even more emphasis on management and communication style. And here we are likely to see a marked difference. Lagarde is comfortable in English and arguably more at ease with the press. Collaboration also seems to be a strong suit, and seemingly in contrast to Draghi, or so his critics argue. This is not to play down the real differences between the creditor and debtor nations or between the small and large countries. Instead, many central banks have divisions but have found ways to overcome divisions insofar as there are dissenting opinions that are formally incorporated in the decision-making record. The ECB, like the Federal Reserve, is engaged in a comprehensive review of the monetary policy framework. The results will likely be a highlight in next year. The staff forecasts will be updated, and these will draw some interest as well. |

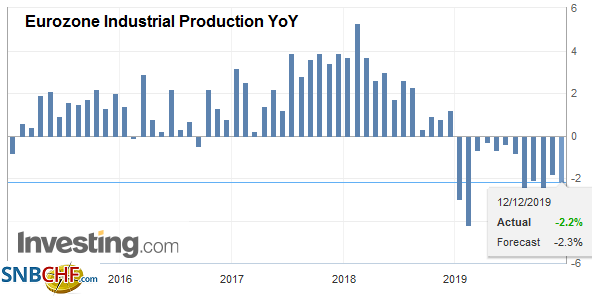

Eurozone Industrial Production YoY, October 2019(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

| In the UK, 650 seats of the House of Commons are at stake today, but not really. In 2015, 17% of the seats actually changed hands, and in the 2017 election, about 10% did. Although some polls have shown the race tightening as the election drew near, the market is still expecting a sufficient Tory majority to push through Brexit. Sterling has reached nine-month highs as the voting begins. There seem to be two risks. One is obvious. The polls are wrong, and it is a much tighter contest, and the Tories are denied a majority. Sterling would come off hard. The second is that the Tories do win, but the news has mostly been anticipated, and after what may be a quick flurry, it comes off, amid “buy the rumor sell the fact” type of activity. |

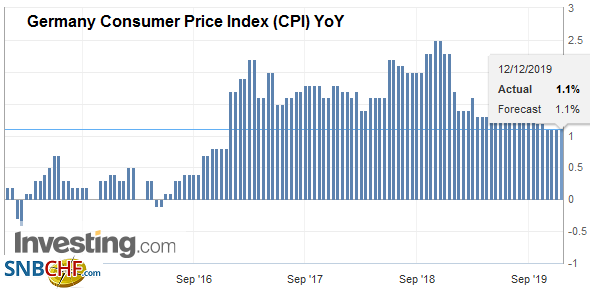

Germany Consumer Price Index (CPI) YoY, November 2019(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

Two other central banks at opposite ends of the risk spectrum also draw attention today. First, the Swiss National Bank met and, as widely expected, remained on hold. It threatened to continue to intervene as necessary and sees global risks tilted to the downside. The euro made highs for the year against the Swiss franc in April near CHF1.1470. It trended lower to reach the year’s low in August around CHF1.08. For the last two months, the euro has traded mostly between CHF1.0860 and CHF1.1050. The Swiss franc would likely a “safe haven of choice” if the US-China tariff truce ends. The other central bank is Turkey. Inflation continues to trend lower. Every month beginning with April, Turkey’s monthly CPI was less than the same month in 2018. The central bank has slashed rates since the first cut in July. The one-week repo rate peaked at 24%, and after four consecutive moves counting today’s larger than expected 200 bp cut, it now stands at 12.0%. Most were expecting a 150 bp cut. Cumulative monthly CPI prints show CPI running near 10.5% this year, and this leaves the real rate around 1.5%, which does not appear to compensate for the risks and may leave the lira vulnerable. The lira softened in the immediate aftermath of the larger than expected cut.

The euro reached almost $1.1145 today as it tries to extend its rally into a fourth session. Last month’s high was near $1.1175, but ahead of it, the 200-day moving average (~$1.1155) is found, and the euro has not traded above in six months. There is an option for almost 720 mln euros at $1.1125 that is expiring today, and that area offers initial support. There is also an option for about 675 mln euros at $1.12 that will be cut. Sterling is straddling $1.32 today. There is a nearly billion sterling option struck there (~GBP930 mln) expiring today. Initial support near $1.3180 was successfully tested in the European, and the market demand for sterling does not appear satiated. There is a smaller option at $1.3250 for about GBP240 mln that suggests the next upside target.

America

The Federal Reserve did not surprise, but the dollar and bonds rallied as some saw a dovish leaning. Powell suggested that while policy is on hold, the bar to a cut is lower than a bar to a hike. The Fed is interested in ensuring the expansion continues, and that price pressures increase. Powell also seemed to emphasize scope for lower unemployment without spurring inflation. Minor tweaks were made to economic forecasts, and it dropped the reference to “uncertainties” in the outlook. The long-run unemployment rate was shaved to 4.1% from 4.2%. The economy is expected to expand by 2% in 2020 and 1.9% in 2021. Thirteen Fed officials think that no change in Fed policy is appropriate next year. Four think a hike will be required. The median forecast is consistent with no hike in 2020 and a hike in 2021 and 2022. While Powell has drawn parallels to the midcourse correction in 1998, he drew back from extending that analogy to what followed. The three cuts delivered then were unwound over the following 18 months or so. The takeaway for investors is that it was a dovish hold. The yield curve (2-10-year) flattened as the two-year yield slipped three basis points, and the 10-year yield fell by five basis points. The implied yield of the December 2020 fed funds futures contract fell 3 bp to 1.305%. This seems to fully discount a 25 bp rate. The Dollar Index fell to four-month lows (~97.00).

The US PPI and weekly jobless claims are not the stuff to move the markets, and this seems doubly true given that investors’ attention at the time will be on the ECB meeting. That said, both are expected to edge higher. Mexico reports October industrial output figures, and the first back-to-back monthly decline is expected since February-March. The first Fed official post-meeting will be the NY Fed’s Williams tomorrow. As widely expected, Brazil’s central bank delivered a 50 bp cut in the Selic rate yesterday, bringing it to a new record low of 4.5%. It did not shut the door on future cuts but said it would act cautiously. It was the fourth consecutive rate cut and the market expected pause even if not the end of the cycle.

The US dollar returned toward the CAD1.3150 area from where it had rallied in response to last week’s diverging employment reports. Whether the level holds depends on the greenback’s general direction, which may be in the hands of the ECB now. It has approached the lower Bollinger Band, set two-standard deviations below the 20-day moving average, and this may induce some caution and reinforce the importance of the CAD1.3150 support, which is also a (61.8%) retracement area of the US dollar rally last month. A break would initially target something close to CAD1.3100. The US dollar recorded a bearish outside down day against the Mexican peso and tested the MXN19.10 level, one-month lows. Follow-through selling could see the dollar test support near MXN19.00. It has not been below there since the very end of July. The dollar has slipped about 0.65% before the central bank’s as expected rate cut. Slipping below BRL4.12, it also set one-month lows. The next level of support is seen around BRL4.08.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brazil,Currency Movement,ECB,EUR/CHF,Eurozone Industrial Production,Featured,federal-reserve,FX Daily,Germany Consumer Price Index,India,newsletter,Turkey,USD/CHF