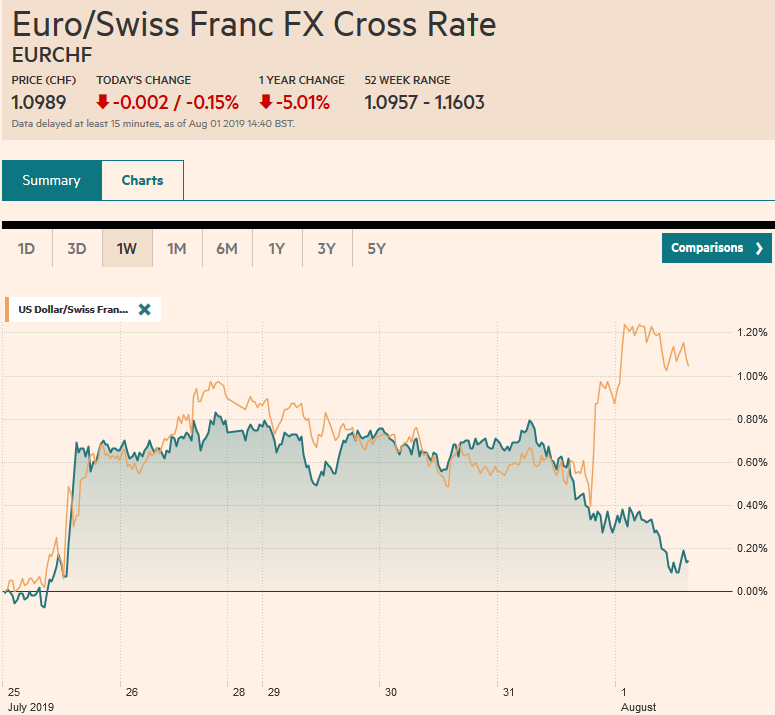

Swiss Franc The Euro has fallen by 0.15% to 1.0989 EUR/CHF and USD/CHF, August 01(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The Federal Reserve delivered the first rate cut since the Great Financial Crisis but couched it in terms of a mid-course correction rather than the start of a larger easing cycle. By doing so, Fed chief Powell cast the cut in less dovish terms than the market expected and the reaction function of the market has been clear. The US dollar has advanced against nearly all the world’s currencies. The greenback broke through key levels that had been holding capping it, like JPY109 and .11 for the euro. Asian equities followed the US lead

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Currency Movements, EUR/CHF, Eurozone Manufacturing PMI, Featured, Federal Reserve, FX Daily, Germany Manufacturing PMI, Japan Manufacturing PMI, newsletter, South Korea, U.K. Manufacturing PMI, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.15% to 1.0989 |

EUR/CHF and USD/CHF, August 01(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Federal Reserve delivered the first rate cut since the Great Financial Crisis but couched it in terms of a mid-course correction rather than the start of a larger easing cycle. By doing so, Fed chief Powell cast the cut in less dovish terms than the market expected and the reaction function of the market has been clear. The US dollar has advanced against nearly all the world’s currencies. The greenback broke through key levels that had been holding capping it, like JPY109 and $1.11 for the euro. Asian equities followed the US lead lower, with Japan an exception. European equities are faring better. US shares are little changed in European turnover. Benchmark 10-year bond yields are around basis points higher, and the peripheral yields in Europe are up a little more. Gold has been knocked back toward $1400, and WTI for September delivery is snapping a five-day advance. |

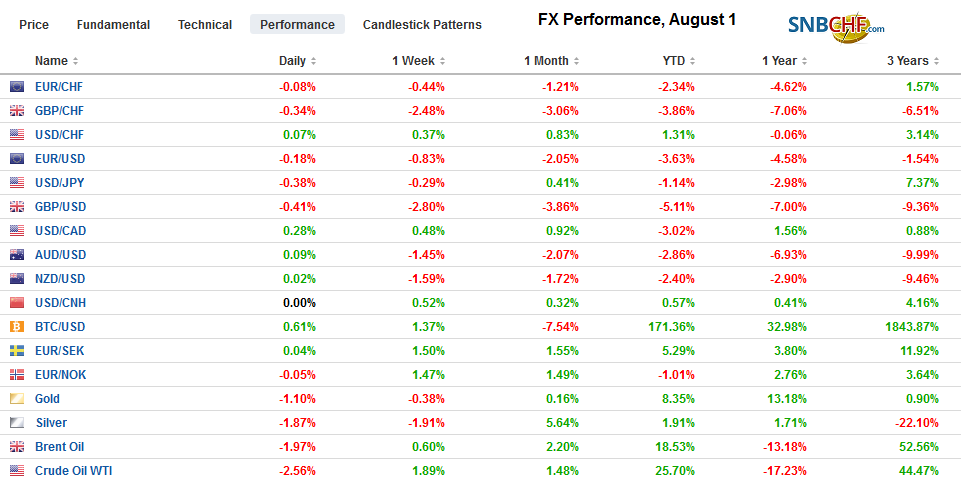

FX Performance, August 1 - Click to enlarge |

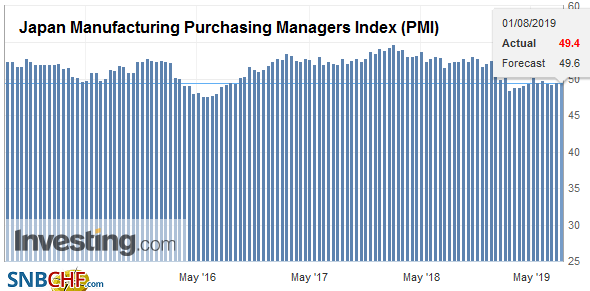

Asia PacificChina’s Caixin manufacturing PMI edged higher but is still below the 50 boom/bust level, but barely. It rose to 49.9 from 49.4. In the coming days, the rest of the Caixin PMI will be reported, as will reserves, trade, and inflation. The PBOC is widely expected to reduce reserve requires to ease financial conditions in the coming period. Japan’s manufacturing PMI firmed slightly to 49.4 from 49.3 from June, but disappointing given that the preliminary estimate was 49.6. It is the third consecutive month below 50. Separately, Japan reported strong auto production for May (9.3% year-over-year, double April’s 4.7% pace and the strongest in two years. The BOJ left rates on hold earlier this week after both it and the government shaved growth forecasts. |

Japan Manufacturing Purchasing Managers Index (PMI), July 2019(see more posts on Japan Manufacturing PMI, ) Source: investing.com - Click to enlarge |

South Korea reported its July manufacturing PMI slipped to 47.3 from 47.5, as its manufacturing sector remains distressed. After a bounce in March and April, it has returned to the March low (47.2). In all but one month since last October, it has been below 50. Separately, South Korea reported softer inflation (0.6% year-over-year vs. 0.7%), suggesting the central bank has more scope to ease monetary policy. The July trade figures were a little better than expected but still weak. Exports were off 11% year-over-year compared with a 13.7% decline in June. Imports fell 2.7% after a 10.9% slide in June. The challenges in the semiconductor industry continued. South Korea semiconductor exports were off 28.1% year-over-year (-25.6% in June). Exports to China were 16.3% lower than a year ago, while exports to the US were 0.7% lower. Imports from China rose 5.8%, and imports from the US rose 9.9%.

Japan’s cabinet is expected to decide tomorrow whether to exclude South Korea from its “white list” of preferred export partners. Japan claims that all of the claims against it from WWII were settled in a 1965 treat the US helped negotiate. South Korean courts say otherwise, and this is the source of the current dispute. If Japan does exclude South Korea, most of Japan’s exports to South Korea will be impacted and required to have individual product approvals. South Korean producers will have little choice but to find alternatives. This is seen as an opening for Chinese companies, and in particular, help the PRC develop its semiconductor fabrication capability. In turn, this would be consistent with its import-substitution strategy. The US appears to have a greater interest in the Japan-South Korea dispute than officials may have recognized.

The dollar popped above JPY109 in Asia for the first time since May and reached JPY109.30 before returning to the breakout area. A convincing break of JPY109 requires at least a close and perhaps a weekly close tomorrow. From a technical perspective, it suggests potential to JPY111.00. Below JPY109, support is seen in the JPY108.60-JPY108.80 area. There are a little more than $2 bln in JPY109.00-JPY109.10 options that expire today, and there is another option for about $825 mln at JPY109.30 that will also be cut. The Australian dollar initially saw its losses extended through $0.6830 but has found a new bid and is staging a recovery. A move above $0.6900 would lift the tone. It is trying to end an eight-day slump. The Chinese yuan softened and the dollar traded above CNY6.90 for the first time since mid-June.

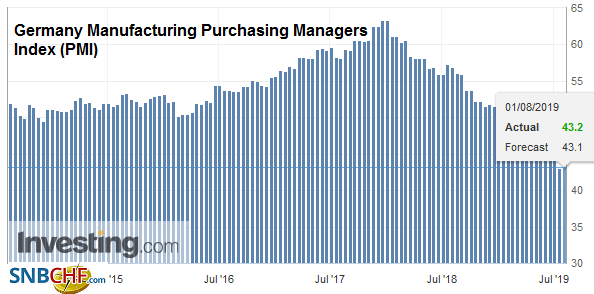

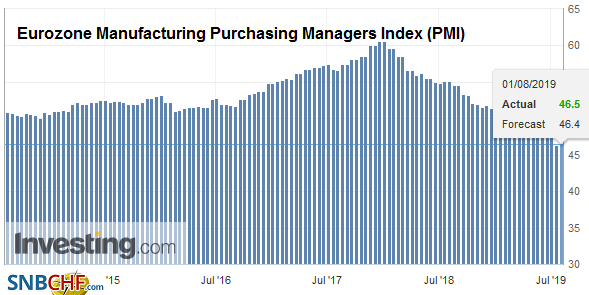

EuropeThe manufacturing sector in the eurozone seems so challenged that even a small upward revision to the flash PMI failed to ease concerns. The German preliminary reading of 43.1 was revised to 43.2, but it is still a cyclical low and is off from the lowly 45 reading in June. France’s manufacturing PMI was revised to 49.7, matching its cyclical low, from 50 of the flash reading and 51.9 in June. Both Italy and Spain ticked up from the June readings but are both below 50 (48.5 and 48.2 respectively). |

Germany Manufacturing Purchasing Managers Index (PMI), July 2019(see more posts on Germany Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| For the region as a while, the manufacturing PMI stands at 46.5 from the 46.4 flash reading and 47.6 in June. |

Eurozone Manufacturing Purchasing Managers Index (PMI), July 2019(see more posts on Eurozone Manufacturing PMI, ) Source: investing.com - Click to enlarge |

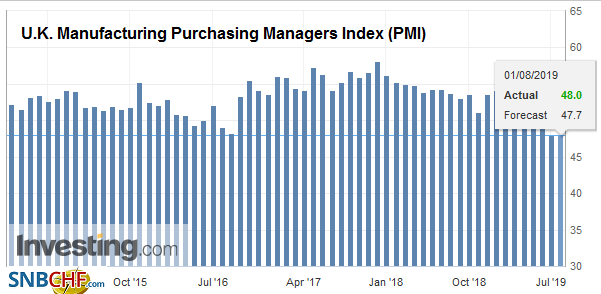

| The Bank of England meets today. Policy is unlikely to change, and it is the color that Governor Carney provides that will be key to the market’s response. The tone is expected to change from a tightening bias, which the market doubted, to a more neutral. The slide in sterling can lift price pressures, but the BOE will likely signal its willingness to ease policy if the exit from the EC is disruptive. Separately, the UK manufacturing PMI was unchanged at 48.0. The market had expected a small decline. It is the third month below the 50 boom/bust level. |

U.K. Manufacturing Purchasing Managers Index (PMI), July 2019(see more posts on U.K. Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The euro peaked yesterday near $1.1160 and today has approached $1.1030. Support is seen near $1.10, and old support (~$1.11) should now act as resistance. More immediate resistance will likely be encountered near $1.1060. Sterling began the week a little below $1.25 and is testing $1.21 ahead of the BOE announcement. There appears to be little chart support until $1.20.

America

Federal Reserve Chairman Powell is finding communicating to be particularly challenging. What had seemed like as much of a non-event as could have been hoped for by the first rate cut in more than a decade, but he defied the market’s assessment by casting the move as a mid-cycle adjustment rather than the beginning of an easing cycle. The mid-cycle language harkens back to the 1990s, where twice the Fed, under Greenspan, managed to have a short easing phase, which ostensibly extended the expansion. For the record, both times saw three 25 bp moves. Judging from the fed funds futures strip and the overnight index swaps, the market continues to price in another cut this year and has scaled back the odds of a third cut to about a 10% chance from around 35%.

We are more sympathetic to the dissenting Fed presidents George and Rosengren, and the several districts that did not call for a discount rate cut. However, these views are a minority, and the majority do seem inclined to cut rates again. We had penciled it in for December, but the market is discounting a little more than a 60% chance of a follow-up move in September. Data dependency seems to determine the timing of the next cut.

The US reports PMI, ISM, weekly jobless claims, and July auto sales. All this is ahead of tomorrow’s employment report. Canada reported a firm May GDP report yesterday, and it suggests the economy may have grown faster than the Bank of Canada’s 2.3% (annualized) estimated for Q2. Mexico’s PMI may draw some interest after reporting Q2 GDP edged up 0.1%–avoiding the second consecutive quarterly contraction. However, the year-over-year decline (-0.7%) was more than twice expectations and illustrates the pressure on the central bank. President AMLO has indicated that rather than cut spending, his government will draw down the savings (“rainy day fund”), which does little to attract investors which have been rebuffed by the end of the airport construction project and the limited opportunities for private investment in the energy space.

The US dollar is testing resistance near CAD1.3220. A convincing break gives potential toward CAD1.33. Initial support is seen near CAD1.3180. Barring a strong recovery in the Canadian dollar, this will be the third consecutive week of losses, the longest losing streak of the year. The US dollar is flirting with the upper end of its recent range against the Mexican peso (~MXN19.20), and July’s high near MXN19.35 would be the next obvious target. Brazil delivered a larger than expected cut yesterday. The 50 bp cut brought the Selic rate to a record low of 6.0%. The dovish comments suggest there is scope for another rate cut later this year. While several emerging market countries that have cut interest rates have seen their currencies strengthen, the real may struggle in the face of the well bid US dollar. Initial resistance is seen near BRL3.84.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Currency Movements,EUR/CHF,Eurozone Manufacturing PMI,Featured,Federal Reserve,FX Daily,Germany Manufacturing PMI,Japan Manufacturing PMI,newsletter,South Korea,U.K. Manufacturing PMI,USD/CHF