Summary Philippine central bank signaled another big hike. Poland central bank appears to be moving its forward guidance out further. Russia officials are sending confusing signals regarding monetary policy. Russia officials stand ready to support the ruble debt market if new US sanctions negatively impact it. South Africa’s African National Congress pledged to undertake land reform responsibly. Moody’s cut its 2018 growth forecast for South Africa to 0.7-1.0% from 1.5% previously. Central Bank of Turkey signaled it will hike rates at the September 13 meeting. Argentina announced a new export tax to help narrow the budget deficit. Brazil presidential candidate Jair Bolsonaro was seriously wounded at a campaign

Topics:

Win Thin considers the following as important: Argentina, Brazil, emerging markets, Featured, newsletter, Philippines, Poland, Russia, South Africa, Turkey, win-thin

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Summary

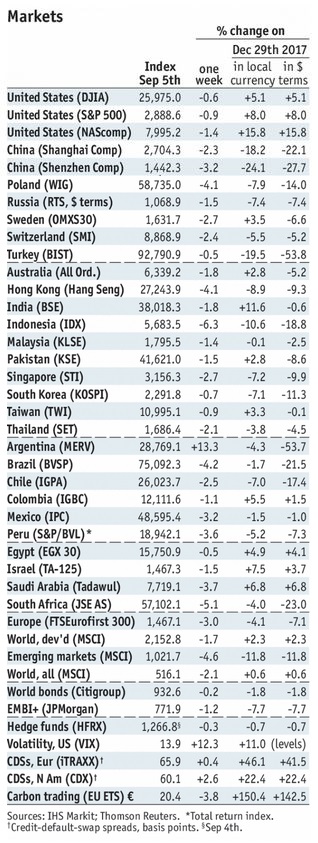

Stock MarketsIn the EM equity space, as measured by MSCI, Brazil (+1.4%), Turkey (+0.6%), and Hungary (-0.3%) have outperformed this week, while Colombia (-4.3%), China (-4.3%), and Hong Kong (-3.9%) have underperformed. To put this in better context, MSCI EM fell -3.2% this week while MSCI DM fell -1.6%. In the EM local currency bond space, Turkey (10-year yield -201 bp), Argentina (-68 bp), and Korea (-5 bp) have outperformed this week, while the Philippines (10-year yield +30 bp), Indonesia (+26 bp), and Chile (+20 bp) have underperformed. To put this in better context, the 10-year UST yield rose 8 bp to 2.94%. In the EM FX space, TRY (+2.2% vs. USD), ILS (+0.5% vs. USD), and HUF (+0.5% vs. EUR) have outperformed this week, while RUB (-3.1% vs. USD), ZAR (-2.9% vs. USD), and INR (-1.0% vs. USD) have underperformed. To put this in better context, MSCI EM FX fell -0.6% this week. |

Stock Markets Emerging Markets, September 5 Source: economist.com - Click to enlarge |

PhilippinesPhilippine central bank signaled another big hike. Governor Nestor Espenilla said that “The Bangko Sentral ng Pilipinas will “take strong immediate action.” The comment comes after higher than expected inflation of 6.4% y/y in August. Last time the bank promised strong action, it delivered a 50 bp hike last month. Next policy meeting is September 27, but Espenilla added that a policy meeting outside of the scheduled six-week cycle is an option. If so, it would be the first intra-meeting move since the BSP adopted inflation targeting in 2002. PolandPoland central bank appears to be moving its forward guidance out further. Officially, the bank sees steady rates through 2019. However, Governor Glapinski said after this week’s policy meeting that it’s “probable” that rates will be steady in 2020 as well. RussiaRussia officials are sending confusing signals regarding monetary policy. Governor Nabiullina said the bank will consider a rate hike at next week’s policy meeting, as inflation risks have grown due to the weak ruble. On the other hand, Deputy Governor noted that monetary conditions are already tightening “at a significant pace.” Lastly, Prime Minister Medvedev took a dovish tone, noting that “rates remain quite high” and urged the central bank to take an “active position” to address this. Russia officials stand ready to support the ruble debt market if new US sanctions negatively impact it. Deputy Finance Minister Kolychev said “In a very stressful scenario when we see the conditions of a market failure” both “the central bank and the government have the tools to intervene on the open market to cushion the adjustment period.” The government has been forced to cancel several debt auctions recently as yields rose too sharply. South AfricaSouth Africa’s African National Congress pledged to undertake land reform responsibly. ANC official stressed that “We will not and will never subscribe to land grabbing in South Africa, we are orderly and we are organized in what we do.” He added that “We’re after a constructive resolution on expropriation of land, which now will include non-compensation.” Markets remain on edge with regards to how land reform is carried out. Moody’s cut its 2018 growth forecast for South Africa to 0.7-1.0% from 1.5% previously. The agency warned that the weaker than expected outlook will add to the fiscal and monetary challenges. Moody’s is the only one of the three major ratings agencies to still have South Africa at investment grade (Baa3), but we think that its recent comments are setting up a downgrade to sub-investment grade. |

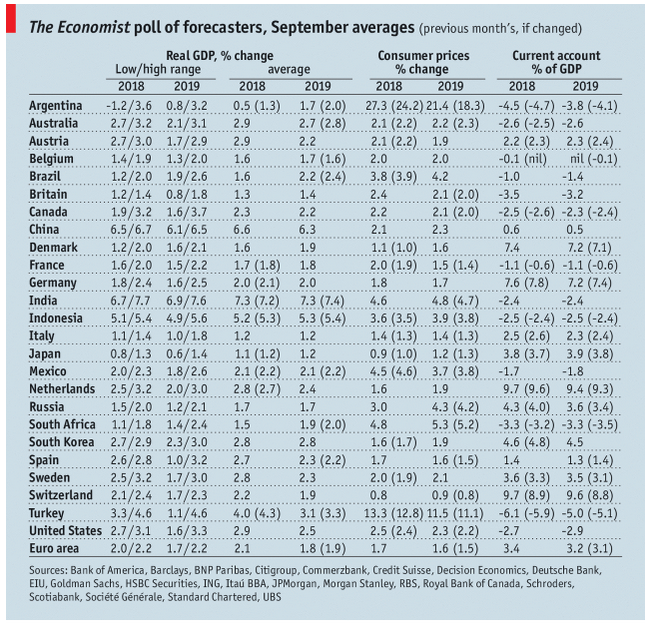

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, September 2018 Source: economist.com - Click to enlarge |

Turkey

Central Bank of Turkey signaled it will hike rates at the September 13 meeting. The statement came after Turkey reported higher than expected inflation of 17.9% y/y in August. Expectations are all over the place, with 1 analyst looking for no change and 1 looking for a 725 bp hike to 25%. The average forecast is a 325 bp hike to 21%, which was close to the bare minimum that the bank did back in May. The bank has tended to disappoint at every juncture during this crisis, and we think even a 325 bp hike would be a green light to sell the lira again.

Argentina

Argentina announced a new export tax to help narrow the budget deficit. All shipments of primary exports will be taxed at a rate of 12%. However, the tax will be capped at 3-4 pesos per USD value exported, depending on the product. The measure is a reversal for Macri, who has been eliminating distortionary taxes enacted during the Kirchner and Fernandez years.

Brazil

Brazil presidential candidate Jair Bolsonaro was seriously wounded at a campaign stop. He is now in stable condition, but markets are trying to gauge the full impact of the horrific stabbing. The knee-jerk reaction was positive due to the notion that Bolsonaro would get the sympathy vote. Polls up until now have shown him leading the first round but losing to virtually all possible candidates (tied with Haddad) In the second. Next round of polls will be very important.

Tags: Argentina,Brazil,Emerging Markets,Featured,newsletter,Philippines,Poland,Russia,South Africa,Turkey,win-thin