Turkey Officials have taken steps to make it more difficult and more expensive to short the lira, but that did not prevent a 5% slide ahead of the weekend. There is no interest rate, within reason, that can compensate for such currency risk. When S&P cut its sovereign credit rating to B+ from BB- and retained a stable outlook, it did not cite the dispute over the pastor. Moody’s cut Turkey’s rating to Ba3 from Ba2 and revised the outlook to steady. It explained that “The key drivers for today’s downgrade is the continuing weakening of Turkey’s public institutions and related reduction in the predictability of Turkish policymaking.” Despite the parallels that are being drawn with the 1997-1998 Asian Financial Crisis,

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, EUR, Featured, JPY, MXN, newsletter, Turkey, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Turkey

Officials have taken steps to make it more difficult and more expensive to short the lira, but that did not prevent a 5% slide ahead of the weekend. There is no interest rate, within reason, that can compensate for such currency risk.

When S&P cut its sovereign credit rating to B+ from BB- and retained a stable outlook, it did not cite the dispute over the pastor. Moody’s cut Turkey’s rating to Ba3 from Ba2 and revised the outlook to steady. It explained that “The key drivers for today’s downgrade is the continuing weakening of Turkey’s public institutions and related reduction in the predictability of Turkish policymaking.”

Despite the parallels that are being drawn with the 1997-1998 Asian Financial Crisis, Turkey is not essentially a currency crisis. The precipitous decline in the currency is a reflection of another crisis, and that is a crisis of confidence over its policies, which seem to purposefully disregard the requirements of capital. Tightening regulations, a promise of investment by Qatar, and the release of the Brunson will not be sufficient to attract investors. Indeed, even if officials were to stabilize the currency near current levels, the economic consequences will be severe. High inflation and a recession are all but avoidable, and a banking crisis seems probable.

Although at first, the meltdown in Anarka spurred a broad risk-off move, which seemed emotional and exaggerated, by the end of last week, Turkey’s woes seemed more idiosyncratic than systemic. Suggestions by some economists that given the speed at which the external balance will adjust, the lira is cheap relative to models of fair value seem premature. We share S&P’s concern that “absent quick and decisive action” the economic, financial, and fiscal costs could escalate. The pain already being inflicted on Turkey has not been sufficient to get Erdogan to capitulate.

S&P also noted risks stemming from its international relations. On the one hand, as a member of NATO, it is under the nuclear umbrella. The EU has failed to find an accommodation to integrate Turkey economically. The doubling of US tariffs on steel and aluminum imports from Turkey is in response to the sharp depreciation of the lira, not the dispute over Brunson. The US warned that more sanctions will be forthcoming if Brunson is not released. Turkey’s interests have diverged from the US in Syria and Afghanistan. We continue to suspect that unless some bold, creative leadership emerges, there is a reasonably good chance that Turkey leaves NATO. At the same time, what is seen as heavy-handedness by the US may encourage other countries to assist Turkey in modest ways to minimize the impact.

China

Officials have taken several steps to discourage shorting the yuan. The PBOC has set the fix (reference rate) stronger-than-expected for the yuan in recent days. It has taken regulatory steps to increase the cost of shorting the yuan. Officials also reduced offshore liquidity, and some have suggested officials may have intervened through state-owned banks in the offshore market. One of the important, and often overlooked drags on the yuan, has been falling interest rates, both in absolute terms and relative to the US. Both three-month SHIBOR and the government’s 10-year yield stabilized last week.

These developments, coupled with the dollar’s losses in North America before the weekend, will likely help lift the yuan in the coming days. We do not accept the claims that China has weaponized the yuan. Many American observers insist the US is the center of the narrative and China’s efforts to stabilize the yuan is an attempt to appease America ahead of the talks. We are not convinced and see domestic reasons why Chinese officials wanted to arrest the yuan’s slide.

The Chinese stock market has not stabilized. With last week’s 4.5% drop, the Shanghai Composite is off 19.3% year-to-date, and the pre-weekend close was the lowest since March 2016. Between August 2015 and March 2016, the Shanghai Composite was halved and it had repercussions through the global capital markets. Since the high for the year was recorded in early February, it is off nearly 25% and is spurring much less consternation and contagion. The MSCI Emerging Markets Index is off less than half as much (-11.7%). The rolling 60-day correlation with the S&P 500 on a purely directional basis fell from a little more than 0.70 to -0.45 over the past three months.

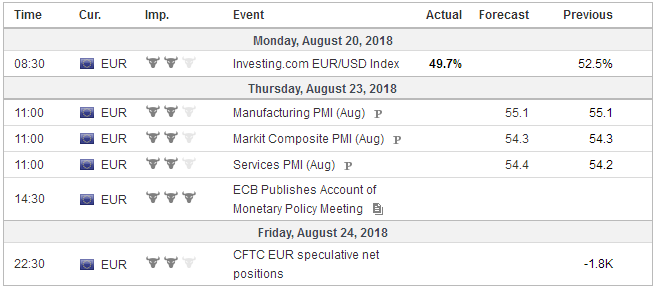

EurozoneThe favorable news stream from Europe that helped drive the euro higher last year has faded. The region has yet to fully recover from the slow down in Q1 linked to various one-off factors, like weather and strike activity. Yet the 0.7% growth reported in the last three quarters of 2017 may very well represent the peak in the cycle. August’s flash PMI for the eurozone is the data highlight in the week ahead. Although auto tariffs have been avoided, for the time being, the US steel and aluminum tariffs remain in effect for Europe and the US unilateral action against Iran will take a toll on European business who have ties to both countries. We wonder if there isn’t downside risk to the manufacturing PMI. Also, the unseasonably hot summer may also have impacted economic activity. Recall it rose from 54.9 in June, matching the lowest level since November 2016, before edging to 55.1 in July. It averaged 57.4 last year and 55.2 in Q2 18. The composite reading is also expected to firm to 54.4. from 54.3. It averaged 54.7 in Q2 18 and 57.0 in Q1 18 and 56.6 in H2 17. The risk-off impulse re-exposed the simmering problems in Italy. The 10-year Italian yield had pulled back from the dramatic peak in last May over 3.4% as capital struck against the new government’s initial plans to give the finance portfolio to a Euroskeptic. The yield fell roughly 100 bp as the signal was modified under the duress created by the President. At every turn, Salvini, the deputy PM from the League continues to bash the EU, while pushing for an income tax break,w which will not necessarily help address the country’s indebtedness. At the same time, Di Maio, from the Five Star Movement is pushing for a new transfer program that will aid those not in the labor market. Even a tragic bridge collapse was turned into an anti-EU rant. The 10-year yield closed above 3.0% every day last week, the doom-loop that ties the banks to the sovereign (through bond ownership) remains intact. The Italian bank share index fell in eight of the past nine sessions and have lost a little more than an eighth of their value three-week slide. Part of this is unique to Italy, but the spread between German Bunds and peripheral bonds is widening more generally. The Italian 10-year premium has yawned by 64 bp over 10-year Bunds. Spain has widened by 20 bp, and Greece by 50 bp. Among the periphery, Portugal has fared the best, with its premium nudging 13 bp higher. |

Economic Events: Eurozone, Week August 20 - Click to enlarge |

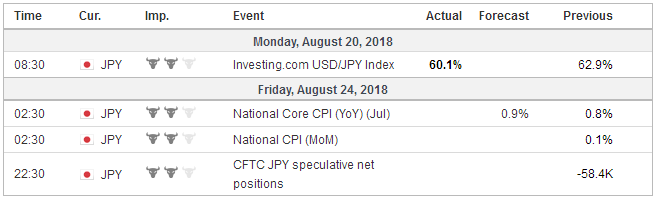

JapanWhen the BOJ announced its policy adjustment that included a wider trade range for the 10-year yield, the sell-off injected volatility in global bond markets and spurred some curve steepening. However, the market has now found a new equilibrium and the 10-year yield has been confined to about a two basis point range on either side of 10 bp. The inflation report at the end of the week reminder that while deflation has been arrested, inflation, excluding fresh food and energy has not upside momentum, even if it rises to 0.3% from 0.2%. Don’t let anyone say this is a 50% increase. The market is wary of other modifications of the BOJ’s operations, with some suggesting the next adjustment could be reducing the amount of ETFs it is buying from the current JPY6 trillion a year. Japanese shares had been highly correlated with the dollar-yen exchange rate through the H1. However, the correlation has broken down over the last six weeks. The 60-day rolling correlation had been near 0.95 for both the Topix and Nikkei in late June and is inverted for the Topix and less than 0.2 for the Nikkei. The correlation between the dollar-yen and the S&P 500 recovered from an inversion in the Q1 to finish Q2 near 0.5 and is now in the middle of a 0.50-0.70 range. The dollar-yen exchange rate continues to move in the opposite direction of the MSCI Emerging Markets Index. We suggest the relationship is best understood not as a safe haven, though, of course, there are some speculative flows that anticipate the real flow, but the unwinding of funding structures, where short yen is used finance higher risk assets (e.g., EM). The correlation between the dollar-yen and the MSCI Emerging Markets Index reached 0.75 (60-day rolling basis) in May and is now a little below 0.5. That is to say, knowing the direction emerging market equities does is not very helpful in forecasting dollar-yen presently. The correlation between the dollar-Swiss franc and the MSCI Emerging Markets Index is stronger at -0.6. In late July, it had briefly been near zero. |

Economic Events: Japan, Week August 20 - Click to enlarge |

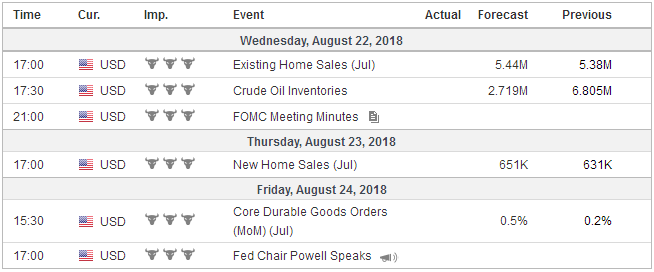

United StatesFed Chief Powell’s speech at the Jackson Hole confab on August 24 is the highlight in a week that features new and existing home sales, the flash PMI, and July durable goods orders. There is some speculation that Powell may hint at a shift in policy, perhaps in reducing the pace of the tapering of the balance sheet for technical and/or financial stability purposes. We demur and expect Powell to recognize the success of the current strategy and indicate a desire to continue going forward. The unwinding of the Fed’s balance sheet is less than a year old, and it does not reach its terminal pace until October. With trade tensions continuing to run high, there is no reason for Powell not to repeat his concern about the economic risks it poses. The US growth has accelerated with the help of the tax cuts and spending increases. The Atlanta Fed GDPNow sees the economy matching Q2 strength here in Q3. The St. Loius Fed’s model puts growth closer at 3.7%. The Blue Chip economists survey is for a little more than 3%. Even the NY Fed’s model of 2.4%, which would be disappointing, is above trend. A few analysts have played up the possibility of US intervention to cap the dollar, and some journalists have run with it. Trump is unpredictable and does not often let tradition restrain his freedom of expression, we recognized the possibility of additional verbal intervention. In fact, we have even doubted that the President wrote the most recent tweet that acknowledged that foreign capital inflows were driving the dollar higher. However, actual material intervention is a horse of a different color. It would require the authorization to sell US dollars and buy foreign money. Trump would not only find it distasteful but unpatriotic. The agreement with the EU bought the multifaceted Trump trade offensive a temporary truce on one flank, allowing it to concentrate on the other two, NAFTA and China. The NAFTA negotiations are much more protracted than the administration had anticipated and even now are playing up the likelihood of a near-term agreement. Rather than a three-way negotiation, in recent weeks the US has isolated Canada, and the Trump has been particularly critical of it, perhaps still miffed by the rancor at the last G7 meeting. In any event, a US-Mexican agreement itself remains elusive and the end of the month self-imposed deadline may be missed. And Canada will not accept a fait accompli and has indicated that a sunset clause is not acceptable. Investors seemed to like the positive spin put on the low-level talks between the US and China for August 22-23 in Washington. It is the first formal talks in a couple of months since the US walked away from China’s offer to boost its US purchases by $70 bln. The talks will not prevent the imposition of 25% tariffs on $16 bln of Chinese exports to the US as part of the $50 bln punishment for PRC intellectual property rights violations. Reports suggest next week’s meeting to begin preparing for a Trump-Xi summit in November, like after the US midterm elections on November 6. This too plays on ideas that Trump’s trade posturing shaped by electoral politics. Yet, given that trade policy is dominated by the likes of Lighthizer, Navarro, and Ross, we think that the administration’s assertive stance toward China is real and strategic. |

Economic Events: United States, Week August 20 - Click to enlarge |

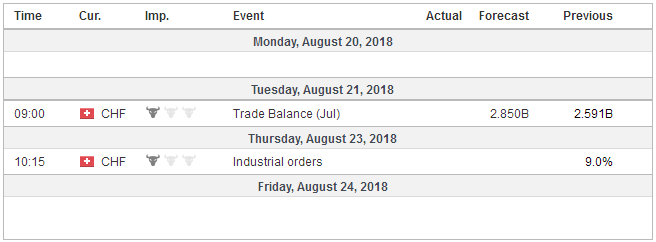

Switzerland |

Economic Events: Switzerland, Week August 20 - Click to enlarge |

Tags: #USD,$CNY,$EUR,$JPY,Featured,MXN,newsletter,Turkey