The US dollar surged last week, with the Dollar Index rising 1.25%, the most since April. The dollar is being boosted by two drivers. The first is the policy mix and interest rate divergence. The other is the intensification of pressure on emerging market. Turkey has a disastrous combination of more fundamentals, large short-term foreign currency debt obligations, unorthodox policies, and the lack of credibility. On top of this, Erdogan has antagonized the US when it is keen to flex its muscles. The lira collapsed 21% last week and as the headlong plunge accelerated risk assets fell out of favor. This included other emerging markets, equities, and peripheral European bonds. It did nothing for gold, which edged

Topics:

Marc Chandler considers the following as important: 4) FX Trends, CHF, EUR, Featured, JPY, newsletter, Norwegian Krone, Turkey

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The US dollar surged last week, with the Dollar Index rising 1.25%, the most since April. The dollar is being boosted by two drivers. The first is the policy mix and interest rate divergence. The other is the intensification of pressure on emerging market. Turkey has a disastrous combination of more fundamentals, large short-term foreign currency debt obligations, unorthodox policies, and the lack of credibility. On top of this, Erdogan has antagonized the US when it is keen to flex its muscles.

The lira collapsed 21% last week and as the headlong plunge accelerated risk assets fell out of favor. This included other emerging markets, equities, and peripheral European bonds. It did nothing for gold, which edged lower, extending its drop for a sixth consecutive week. The US provided more fodder by imposing sanctions on three countries last week, a new axis of evil (?)–Russia, Turkey, and Iran.

One of the key questions facing investors is whether Turkey is the canary in the coal mine the way Thailand was in the 1997-1998 Asian Financial Crisis. Recall that that crisis was one in which fixed exchange rate regimes were overwhelmed. That is not an issue now, though as we have seen floating rate adjustments can be quick and sharp as well. Still, a judgment must be made about the likelihood that the intense risk-off mood ahead of the week is sustained. Given the magnitude of bank exposures and the fact it is many investors had hedged and/or reduced exposure to Turkey already, we do not expect the market to be able to sustain the pace we saw at the end of last week. If an attempt to extend the pre-weekend moves in early Asia on Monday falters, then the markets recover.

While our outlook for the dollar remains constructive, it is over-extended. All the major currencies finished last week outside their Bollinger Bands. Momentum traders may try to push further, but we suspect that before the dollar can advance much more, it needs to consolidate its recent gains. The late dollar longs may be in weak hands, but the corrective or consolidative phase need not be deep or long. It is not unusual for the markets to retest the breakout. The liquidation by the momentum players may provide an opportunity for stronger hands of the investment community.

One way to express this view is in the crosses that were driven by the arguably exaggerated risk-off move like euro-Swiss or euro-yen. The euro fell to its lowest level against the Swiss franc since last August near CHF1.1340. To be sure, it is not just erosion of Turkey that weighed on the cross, which fell for the fourth consecutive week, but the dramatic move in the second half of last week saw the euro move three standard deviations from the 20-day moving average. A return to the breakout gives the euro scope for a 1% gain. The euro’s decline against the yen also saw it test three standard deviations from the 20-day average.

Another way to express this view is the Norway-yen cross. It already appeared to have begun recovering in the waning hours of last week. The Norges Bank, Norway’s central bank meets on August 16. We expect a hawkish hold, insofar as it confirms intentions to hike rates at next month’s meeting, a week ahead of the next FOMC meeting and at least a year ahead of the European Central Bank.

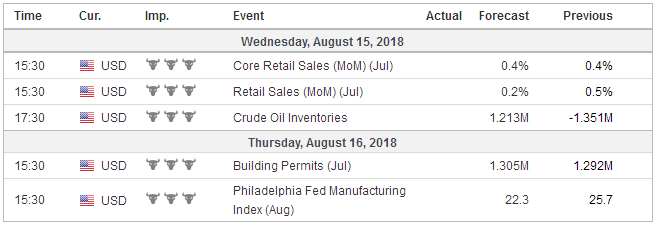

United StatesThere is little doubt among investors that the Fed will hike rates in September. That conclusion suggests that outside of reaction to headlines, investors will look past the data, barring a significant deviation from expectation. US retail sales report may be the most important. Auto and gasoline sales likely slowed from May, but excluding these, retail sales may have risen around 0.4%. The components that are used for GDP calculations also likely rose 0.4% after a flat June report. Sales for this “control group” averaged a 0.5% gain in Q2 after rising by an average of 0.2% in Q1, despite the stagnation of real hourly wages. The average monthly pace in 2017 was 0.4%. The Atlanta Fed GDPNow says the US economy is tracking 4.3% annualized growth in Q3. The NY Fed tracker suggests 2.6% growth, while the St. Louis Fed’s model splits the difference at 3.4%. Other data in the coming days will impact these forecasts, including the first look at August through the Empire and Philly Fed surveys. July Industrial production and manufacturing output are expected to have increased (0.4% and 0.3% respectively) after faster growth in June. Housing starts may attract some attention after the large 12.2% drop in June. Since last October, US housing starts have followed a sawtooth pattern alternating between gains and losses. Housing starts are expected to have risen in July to a 126 mln unit pace. The cyclical peak was set in January a little more than 1.33 mln pace. |

Economic Events: United States, Week August 13 - Click to enlarge |

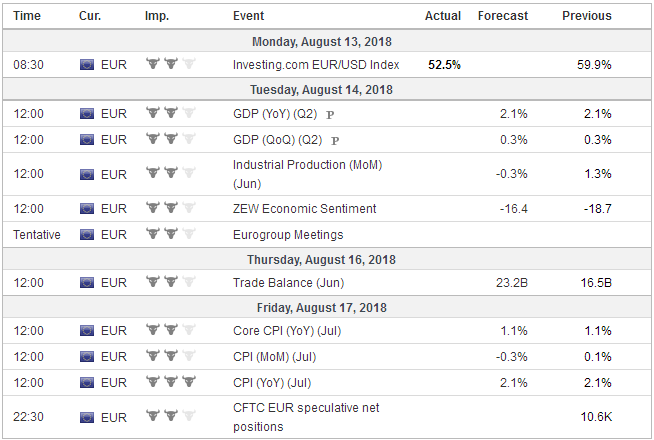

EurozoneEurozone growth and inflation reports are second looks, even if more color is provided, investors’ information set is unlikely to change. That said, there is a reasonable chance that Q2 GDP may be tweaked up to 0.4% from 0.3%. July CPI is expected to confirm the flash readings of 2.1% and 1.1% for the headline and core respectively. The economic data will not distract from discussions of European bank exposures to Turkey. The direct bank exposures are fairly clear as is industrial and commercial ties. What seems somewhat less transparent is the loan loss reserves put aside or hedges and other offsets that have been employed. The risk-off mood weighed on European peripheral bonds, which despite on the ongoing ECB purchases, continue to act like risk assets. Moreover, Spain and Italy appear headed toward a confrontation with the EC over next year’s budget in a few weeks. |

Economic Events: Eurozone, Week August 13 - Click to enlarge |

United KingdomThe UK reports employment, inflation, and retail sales in the coming days. The reports are not expected to change the general assessment of the UK economy. The unemployment rate and wage growth are forecast to be unchanged. Headline inflation may tick up because of the base effect from 2.4% to 2.5%, but it is likely to be reversed next month plus some as the August 2017 0.6% increase drops out of the comparison. The core rate is expected to be unchanged at 1.9%. Sterling’s depreciation may limit this trend but remember the UK’s core inflation rate was 2.7% in January. UK retail sales likely recovered from the 0.5% decline in June, but it might simply reflect higher priced motor fuel. Excluding that, retail sales may be flat after a 0.6% fall. An upside surprise likely would be greeted by sterling buyers. Meanwhile, talk at the end of the week that was overwhelmed by the dollar’s surge ahead of the weekend suggested that there may be some light opening in the EC’s stand on Brexit. It has been playing hardball and not being particularly flexible, but it is willing to accept the UK’s latest proposal to remain in common market for goods, suggesting that the four freedoms are not as inseparable as sometimes presented. However, the price of this may be more than the UK parliament or as some suggest a referendum may agree. |

Economic Events: United Kingdom, Week August 13 - Click to enlarge |

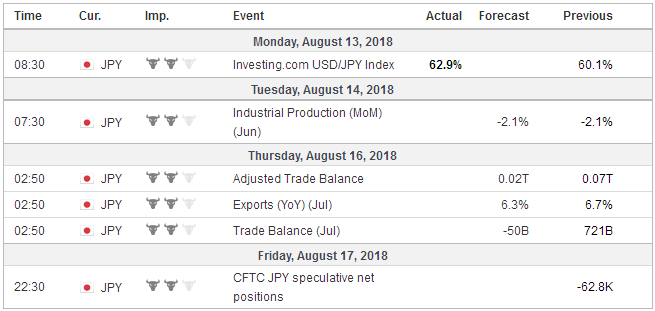

JapanJapan’s June industrial output report is of little interest after the country reported stronger growth in Q2 last week (0.5% vs. 0.3% forecast). However, July trade figures may draw some attention. Seasonal factors point to deterioration from June’s small (JPY21.4 bln) surplus. It is likely to be the fourth deficit so far this year. Before this year, the last monthly trade deficit was in February 2016. Exports in July likely are around 6.3% higher, but still, less than half the (13.4%) pace seen in July 2017. Imports likely rose about 14.2% year-over-year compared with 16.5% last July. |

Economic Events: Japan, Week August 13 - Click to enlarge |

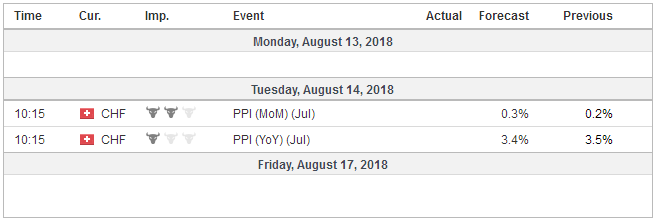

Switzerland |

Economic Events: Switzerland, Week August 13 - Click to enlarge |

A combination of factors, including rising nationalism, the inexorable rise of China and India power relationships are in flux. The Trump Administration is an attempt to reassert not so much US leadership but a narrowly defined national interest. Until the confrontation with Turkey over the arrest of an American pastor on the grounds of aiding a terrorist organization (which seems to have a broad definition), the wrath of the administration was directed at economic competitors. This is a different problem that the macroeconomic mess that the Erdogan and his government have created.

The problem is that the Turkish piece on the chessboard on which the Great Powers play was anchored in the West since the birth of NATO and now may be slipping away. For all practical purposes, and against the wishes of the US (at least until 2016) the EU not found a way to let Turkey into its club. Its claims in Cyprus remain unresolved. Its interests in Syria and elsewhere are increasingly diverging from the US. From the cold perspective of political realism, Turkey is a strategic asset that could shift from to a Russia-Iran-Syria bloc.

Market participants may be leery of some off-the-cuff comment by a Trump Administration official, if not the President himself expressing concern in one way or another about the dollar’s strength. It is its best level of the year against most of the major and emerging market currencies and JP Morgan Emerging Market Currency Index. The OECD’s PPP model puts the euro nearly 17% undervalued and the yen 12%. Sterling is almost 10% undervalued, and the Canadian dollar is a little more than 5% undervalued. Among emerging markets, the Mexican peso is judged more than 100% undervalued, and the South Korea yuan is roughly 29% below PPP.

During parts of a longer-term cycle, currencies are overvalued and undervalued. PPP is the level that currencies gravitate around in the long-run. It is not a short-term guide to fair-value or trading. Focus instead on the macroeconomic drivers and the movement there is still dollar-friendly. Efforts are to pass “tax-reform” 2.0 ahead of the November elections. This package would include making the middle-class tax cuts permanent. There is still some speculation that the administration may tap the oil reserves to release pressure on gasoline prices, but a decision will have to be made soon to prepare and implement a program in enough time to give a fighting chance to lower prices at the pump. Of course, there are many moving parts, and lower oil prices do not always translate into lower gasoline prices.

Tags: $CHF,$EUR,$JPY,Featured,newsletter,Norwegian Krone,Turkey