The triumphalism that followed the fall of the Berlin Wall nearly three decades ago has evaporated. The Great Financial Crisis and inexorable widening of income and wealth inequalities within countries undermined claims of moral and economic superiority. Liberal democracies are fighting a rearguard action and the rise of illiberal regimes. The president of the country with the strongest military might and largest economy not only articulates the illiberalism but tries exporting it as well. Trump eschews the ideological conflict that began in 1917 and shaped the international order since 1944 (Bretton Woods), the Marshall Plan (1948) and 1949 (birth of NATO), and emphasizes economic competition and anti-immigration.

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, CAD, EUR, Featured, JPY, newslettersent, Oil, TLT, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

The triumphalism that followed the fall of the Berlin Wall nearly three decades ago has evaporated. The Great Financial Crisis and inexorable widening of income and wealth inequalities within countries undermined claims of moral and economic superiority. Liberal democracies are fighting a rearguard action and the rise of illiberal regimes. The president of the country with the strongest military might and largest economy not only articulates the illiberalism but tries exporting it as well.

Trump eschews the ideological conflict that began in 1917 and shaped the international order since 1944 (Bretton Woods), the Marshall Plan (1948) and 1949 (birth of NATO), and emphasizes economic competition and anti-immigration. He pulled out of TPP negotiations, but he is more constrained in terms of other multilateral institutions he disparages, including NAFTA, WTO, and NATO. Trump is encouraging others to defect from multilateralist institutions.

Even before being elected president, Trump diverged from US policy and encouraged the UK to leave the EU. Reports suggest he recently tried to get France to abandon the EU. He tried to get Saudi Arabia to violate the recently struck agreement among OPEC and non-OPEC members and boost output by twice as much as had been agreed, which could have meant the end of the cartel. The US ambassador to Germany, who previously indicated intentions to encourage the populist right, now is reportedly negotiating with German car producers. Under WTO rules, whatever terms are agreed with the US must be extended to all countries. Merkel rejected bilateral talks in favor of multilateral negotiations.

If Trump’s modus operandi continues, the NATO summit on July 11 will feature more calls for greater burden sharing, which is a traditional US complaint. It will be followed by a meeting with Putin that will be considerably warmer than the NATO summit, despite the divergence of US and Russian strategic interests. Little noticed, and even less commented on before the weekend Russia joined the growing number of countries who are retaliating against US tariffs by imposing tariffs on US goods.

President Trump’s trade adviser Navarro had previously claimed that no country would retaliate against the US because access to the large US domestic market was so important. It is precisely because other countries are responding in what some would have thought was the predictable way given the recent history and rhetoric that shapes the current climate. In the coming weeks, the US will hold public hearings for the next set of tariffs (~$16 bln) on Chinese goods and when implemented China will respond in kind. This takes us to the end of the month or early August.

The initiative goes back to the US, and the question is whether Trump will make good his threat to levy an additional 10% tariff on $200 bln of Chinese goods. In addition, the seemingly pre-ordained conclusion of the investigation into US auto imports on national security grounds is expected in the coming weeks. The cycle of high-frequency data sees the UK, Japan, Germany, and China trade reports in the coming days. It is difficult to generalize, and it is too early to see significant impact of the rise of protectionism.

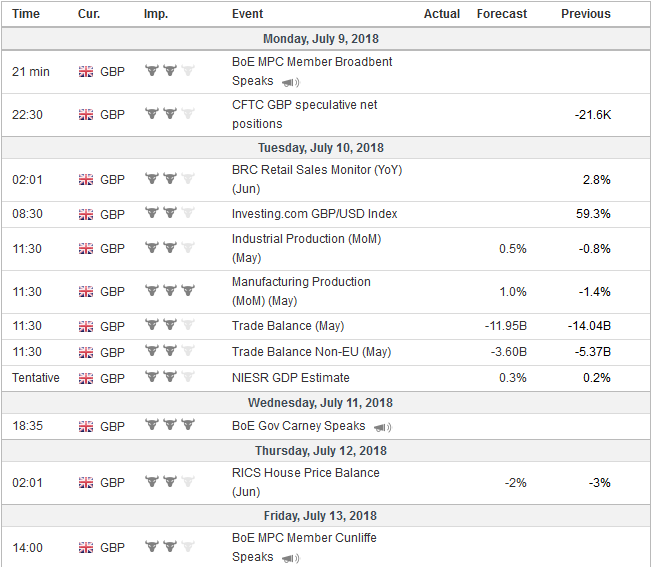

United KingdomThe UK is expected to report a smaller trade deficit in May after a blowout in April. Still, there continues to be an underlying deterioration in the UK trade balance. The trade deficit averaged nearly GBP2.1 bln a month last year. It is averaging near GBP3.0 bln a month this year compared with a GBP2.5 bln deficit in the first four months of 2017. |

Economic Events: United Kingdom, Week July 09 - Click to enlarge |

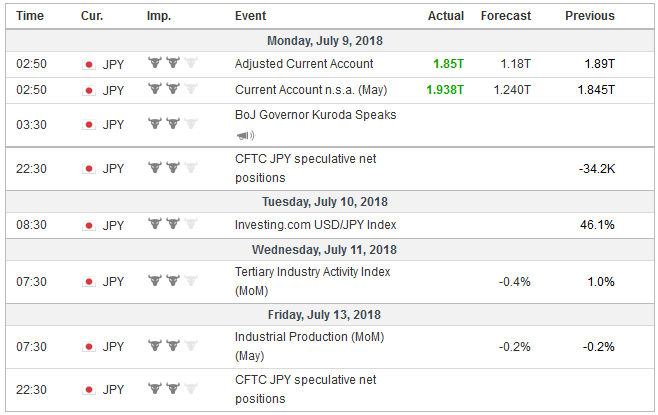

JapanJapan reports its May trade and current account balance. Japan is expected to report a trade deficit after a JPY574 bln surplus in April. There was a small trade deficit last May. However, Japan’s trade balance does not drive the current account. Japan’s current account surplus is driven by investment income in the form of profits, licensing fees, royalties, dividends and interest payments. In the January-April period, Japan’s current account surplus averaged JPY1.62 trillion compared with JPY1.80 trillion in the same period last year. |

Economic Events: Japan, Week July 09 - Click to enlarge |

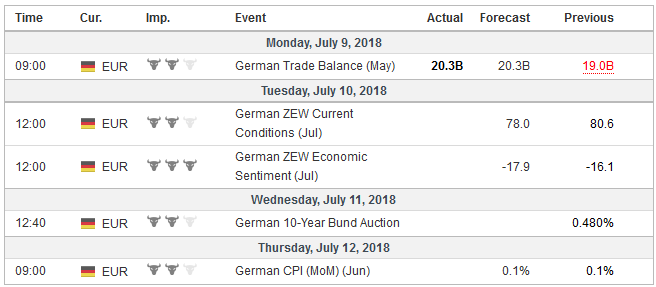

GermanyIn contrast, the German trade surplus is key to its current account surplus. Its trade surplus is a steady as a finely engineered machine tool. Consider that in 2015, the average monthly surplus was 20.4 bln euros. In 2016 it was 20.7 bln euros, and last year it averaged 20.4 bln euros a month. In the first four months of this year, it has averaged 20.1 bln a month. In May, it is expected to have edged to 20.2 bln euros from 20.4 bln euros. |

Economic Events: Germany, Week July 09 - Click to enlarge |

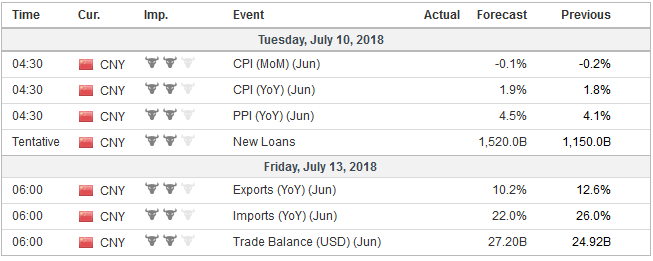

ChinaThe main objection is not that China has a large trade surplus. It is a host of other practices that the US, Europe, Japan, and others find objectionable. China’s trade surplus has averaged about CNY130 bln in the first five months of 2018. In the same 2017 period, the monthly average was CNY187 bln. Even in dollar terms, a reduced trade surplus is evident. It averaged just less than $20 bln a month so far this year compared with a little more than $27 bln a month in the same 2017 period. China also will report June CPI figures. The pace is expected to have risen to 1.9% from 1.8%. China’s CPI, like much of its data, seems unusually stable. It was 2.1% at the end of 2016 and 1.8% at the end of 2017. This may give Chinese officials cover to force deleveraging while trying to target liquidity provisions to minimize the collateral damage. In terms of the business and credit cycle, the US is in a superior place to China, but the products targeted for the retaliatory tariffs by China and other countries are conscious attempts to punish his supporters and his allies supporters. President Xi does not know such pressure. China will also report its June reserves. The market expects a $9 bln decline, which is really a rounding error of its $3.110 trillion holdings. Typically, when China’s reserves fall so do its holdings of US Treasuries. In June, the US 10-year Treasury yield was virtually unchanged at 2.86%, suggesting if it was a seller, it was small and inconsequential. The yuan is the world’s weakest currency since June 14. It has depreciated by 3.6%. PBOC officials have tried mild jawboning. There seems to be a growing number of observers who think that despite denials, the depreciation of the yuan is an attempt to blunt the impact of the tariffs. There has been a distinct change recently. Consider that on a purely directional basis, the yuan and euro correlation over the past 60 days is about 0.70, while the correlation over the past 30 days is a little more than 0.25. However, we are not convinced that this is about trade, though like so many of China’s moves, it can serve more than one objective. As part of the easing of some monetary conditions in China, officials may be unwinding the previous strength. Recall that through the end of April, the yuan was up 2.75% and one of the strongest currencies. It is now down 2% for the year,, and still one of the strongest emerging market currency. It is ironic that many neoliberal economists emphasize the risks posed by the surge in China’s debt and then don’t believe that investors and businesses would want to diversify away from the yuan, suspecting officials are driving it. And then, sounding like Saint Augustine praying for chastity and continence, but not quite yet, they say it is not the right time for China to surrender the yuan to market forces, wanting officials to stop it from falling. |

Economic Events: China, Week July 09 - Click to enlarge |

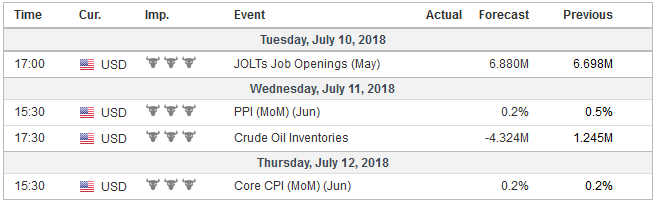

United StatesThe most important US economic report will be the June CPI. Although it is not the Fed’s preferred measure, it is an important part of the inflation story. US price pressures are rising. The base effect means that the 0.2% rise in the headline and core rate is enough to lift the year-over-year rate to 2.9% and 2.3% respectively. It seems incongruous for the US 10-year bond yield to continue to trend lower (having fallen more than 30 bp since the May peak) as US inflation crawls higher. With continued strong job growth, a JOLTS report is expected to continue to show more job openings than unemployed people and the full effect of the fiscal stimulus still to come, there is no reason not to expect a September rate hike. |

Economic Events: United States, Week July 09 - Click to enlarge |

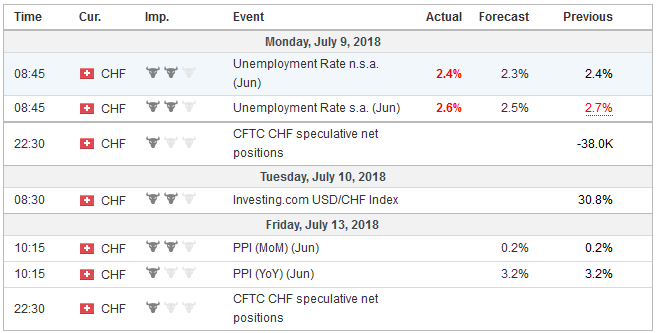

Switzerland |

Economic Events: Switzerland, Week July 09 - Click to enlarge |

Even if trade tensions are not evident in the trade figures, look for them to appear prominently in Fed Chief Powell’s prepared remarks that will be published ahead of his congressional testimony later in the month. Several Fed officials, including Powell, have highlighted the risks and these concerns were clearly expressed in the FOMC minutes. There appears to be a greater consensus on the risks posed by tariffs (boosts prices and slows the economy) than the yield curve, which Powell will also likely address. Although the US coupon curve continues to flatten, in the context of divergence and negative yielding bonds in Europe and Japan, many economists, and apparently several Board of Governors, are less concerned that some of the regional Fed presidents.

Trade tensions were also likely discussed at last month’s ECB meeting, the record of which will be released in the days ahead. Investors may be less interested in its warnings of the risk posed by trade and more interested in the debate over monetary policy. How solid is the commitment to finish asset purchases by the end of the year? Can the reinvestment of maturing proceeds really be used as a tool of monetary policy and what about Operation Twist? Is the ECB really pre-committing to a September 2019 rate hike?

Investors will be watching the fallout of Prime Minister May’s pre-weekend cabinet meeting, where she seemed to rein in her cabinet but not the hard Brexit camp in Parliament. Nor will the deal likely be ultimately acceptable to the EC negotiators. Perhaps there is a different game afoot. Some Brexit leaders may suspect that the EC will not accept what it will likely consider continued cherry picking: customs union for goods, but not services or people. And when May’s compromise is rejected, then there may be an attempt to replace her.

OPEC’s monthly output figures will be closely scrutinized. Despite what is expected to show an increase in Saudi output as promised, it will not make up for the disruption and losses from elsewhere. OPEC’s output likely fell. The US industry estimate (API) had shown another large draw of crude stocks, but the government’s estimate (EIA) was a small build. The market may be particularly sensitive to this week’s reports. Oil prices rallied strongly ahead of the weekend. With WTI poised to make new highs, the US rig count continues to grow.

Lastly, it is now widely accepted that the Bank of Canada will hike rates on July 11. This has been our base case since earlier this year. If it doesn’t, the Canadian dollar will quickly sell-off. That sell-off would provide an opportunity to buy Canadian dollars as it will likely be a hawkish hold. The Bank of Canada would likely indicate that it is still committed to removing accommodation (i.e., raise interest rates). We think that barring a new shock, the Bank of Canada will hike rates again before the end of the year.

Tags: #USD,$CAD,$CNY,$EUR,$JPY,$TLT,Featured,newslettersent,OIL