Interest rates, led by the US, have accelerated to the upside. With price pressures generally rising and oil prices at four-year highs, it is understandable. Market participants need to see the breakout that has lifted US 10-year yields to their highest level in seven years is confirmed in subsequent price action. The first test was passed as the disappointing jobs growth in September could have been an excuse to push yields lower. Perhaps, it was not a completely fair test as the unemployment rate fell to the lowest level in nearly half a century and there were strong upward revisions. The next test may be next week’s inflation reports. The core rates of both the PPI and CPI are expected to have crept higher while

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, brl, EUR, Featured, Italy, newsletter, Oil, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Interest rates, led by the US, have accelerated to the upside. With price pressures generally rising and oil prices at four-year highs, it is understandable. Market participants need to see the breakout that has lifted US 10-year yields to their highest level in seven years is confirmed in subsequent price action.

The first test was passed as the disappointing jobs growth in September could have been an excuse to push yields lower. Perhaps, it was not a completely fair test as the unemployment rate fell to the lowest level in nearly half a century and there were strong upward revisions. The next test may be next week’s inflation reports. The core rates of both the PPI and CPI are expected to have crept higher while the headline rate is either stable (PPI) or actually softens (CPI).

At the same time, despite some accusations of equivocating, we think Fed Chair Powell has been clear. Monetary policy remains accommodative with the Fed funds targets range below the neutral or long-term estimate. Interest rates will continue to be gradually lifted, and it may rise through the neutral rate. There is no reason to change the course until the economic performance changes in material ways. High-frequency data is noisy, and the Fed focuses on the signal.

United StatesAt least four considerations pushing US rates higher. First, the market is coming around to accept the Fed’s signal that three rate hikes will likely be appropriate next year. Since September 27, the implied yield of the December 2019 Fed funds futures has risen 12 bp to 2.93% (average effective Fed funds rate is now at 2.18%). This suggests that 75 bp of tightening has been largely discounted. The second consideration is also due to the central bank. Fed officials have played down what had been a conceptual anchor of monetary policy, r*, the neutral rate. It is not clear what will replace it except the good judgment of same said officials. This is another form of ad hocery, for which investors may require an additional premium. Third, the rise in oil prices lifts headline inflation, and there is a presently a strong correlation between oil prices and 10-year US yields. The US 10-year breakeven has about ten basis points over the past month, suggesting higher inflation expectations. This appears to account for about a quarter of the 40 bp increase in the yield of the 10-year benchmark note. Another consideration is the supply and demand dynamics. The supply is increasing, but the Fed is buying less, and the bid from corporate pensions ahead of the September 15 deadline has evaporated. TheTreasury will raise $770 bln in H2 18, which is a 60% increase from H2 17. The cross-currency swap basis and the relative flatness of the US curve make it expensive to hedge the currency, which discourages another set of potential buyers. The move toward 3.25% on the 10-year yield has stretched conditions, and near-term consolidation ought not be surprising. However, investors should be prepared for higher interest rates. The 10-year average yield over the past decade was surpassed eight months ago. The average over the past 20 years is 3.60%. Many are targeting 3.50% on the way to 4.0%. Moreover, the yield curve (2-10 year) steepened 10 bp last week to 35. It is the biggest move since February and brings the curve to back to the steepest last seen in June. This is also signaling a potential change in market dynamics. |

Economic Events: United States, Week October 08 - Click to enlarge |

EurozoneThe rise in Italian yields is arguably only tangentially related to the increase of US yields. Instead, the main driver in Italy is concern that fiscal profligacy of the new government. The benchmark 10-year bond yield has risen by a little more than 35 bp over the past month to approach a critical 3.50%, the highest level in four years. The risk is a move above this area could spur a sharp rise toward the 4.00%-4.25% area. Italian banks have been significant buyers of government bonds, and the link has seen an index of bank shares drop 13% over the past two weeks and is down 19% year-to-date. Despite some modest changes from the initial drafts, Italy’s proposals will bring it into a confrontation with the EC. Already there has been a firm push back against the proposal to backtrack from the fiscal consolidation that course that had been agreed upon. Aggravating the situation, the Italian government is forecasting stronger growth than the EC or private sector. By assuming a large denominator, the deficit/GDP ratio appears smaller. A repeat of the Greek experience needs to be avoided. A vicious cycle of higher interest rates, rising debt stress levels, demands for austerity weaker growth, larger deficits and more debt, could reignite the political and economic crisis in Europe. No one needs to be reminded of Italy’s size and important role in the capital markets. Also, it would complicate the ECB’s effort to exit the extraordinary monetary policy, which extends beyond the asset purchases. The EU is being challenged on many fronts. Brexit still threatens to be disruptive. The Visegrad bloc is estranged, and the current governments shun the liberalism it associates with Brussels and refuses to participate in absorbing refugees. It is considering escalating its sanctions against Russia. Trade tensions are rising with the US, where Trump recently rejected the EC’s offer to drop auto tariffs as insufficient. Bavaria holds state elections on October 14, and the CSU is likely to lose its majority. The SPD has also lost support, with the Greens moving into second place in the state. The Afd do not seem to be gaining new ground and is polling near 10%. EMU growth has lost momentum after a strong H2 17, and reports warn that the German government may revise down this year’s growth forecast to 1.8% from 2.3% and shave down next year’s projection to 2.0% from 2.1%. Political leadership is weak. Merkel’s CDU has seen its support dry up. Macron does not enjoy much more support than Hollande did. Italy’s Prime Minister is a compromise between the League and the Five-Star Movement. Europe has begun a two-year period in which the leadership of some institutions including the EC itself and the ECB will change, as well as a European Parliament election next spring. |

Economic Events: Eurozone, Week October 08 - Click to enlarge |

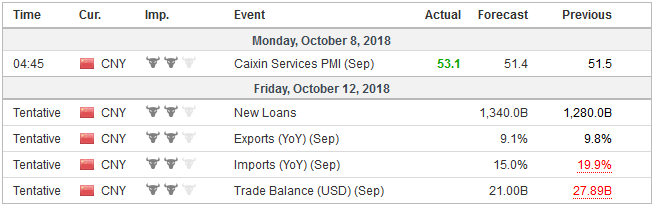

ChinaChina’s markets re-open after the week-long national holiday. The PBOC announced a 1% cut in required reserve ratio (effective October 15) that frees up about CNY1.2 trillion and may help cushion the adjustment to last week’s developments. Over the past week the Hong Kong Enterprise Index, composed of H-shares, fell 3.75% and the MSCI Emerging Markets Index fell 4.5%. The US dollar has been firm, though speculation against the offshore yuan was limited to about 0.25%. The market seemed reluctant to risk triggering official action and was tentative about bid the dollar above CNH6.90 on a sustained basis. The JP Morgan industry benchmark Emerging Market Currency Index fell a little more than 0.8%, to snap a three week firmer, albeit consolidative, phase. The reserve ratio cut will free up funds that allow Chinese banks to easily repay CNY450 bln of MLF (medium-term lending facility) that also comes due on October 15. Reserve requirements, following his cut, will be 15.5% for large banks and 13.5% for small banks. It peaked at 21% in 2011 and remains among the highest globally, which also gives it room to cut further to ease conditions as an alternative to reducing interest rates. It is the fourth reduction in the required reserve ratio this year. There are several economic reports from China in the coming day that will offer more insight into the state of the world’s second largest economy and the impact of the trade tensions. The official PMI showed weakness in export orders. September trade figures are due out late in the week. Before that Caixin’s service and composite PMI will be released. Aggregate financing, yuan lending, and money supply figures will be reported. The data lead up to the October 19 Q3 GDP. The 6.7% growth reported in Q2 was the weakest in two years. China reported a $22.7 bln drop in its currency reserves, which at the end of last month stood at $3.087 trillion. The decline was a little more than expected. While experienced capital outflows during the month and may have intervened to support, the pressure on reserves also likely stemmed from valuation adjustments. The other reserve currencies were mostly little changed, though the yen lost 2.3% against the dollar. The more important impact from valuation may come from the bonds held. Consider that US Treasury 10-year yields rose 20 bp and 10-year Bund yields rose 14 bp. |

Economic Events: China, Week October 08 - Click to enlarge |

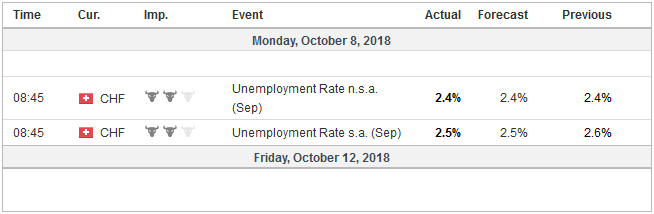

Switzerland |

Economic Events: Switzerland, Week October 08 - Click to enlarge |

The Bloomberg report on extensive Chinese corporate subterfuge is a challenge for both Chinese markets and another stumbling block in what appears to be a deteriorating relationship with the US. The recent confrontation in the South China Sea and the refusing of a port of call in Hong Kong are timely reminders that the rivalry extends well beyond trade. At the same time, many observers exaggerate China’s abilities. China remains clumsy on the world stage, as the disappearance of the Interpol chief (and Deputy Minister of China’s Public Security), and the assassination of Kim Jong-Nam, who had once been thought to be the heir apparent in North Korea, under its watch in 2017 illustrates. Its seeming near predator lending for the One Belt One Road initiative is also breeding contempt.

Brazil’s real and the Bovespa rallied strongly in the lead to today’s election. The real gained an impressive 5.4% against the US dollar last week. Nearly all the other emerging market currencies fell. The Bovespa rallied 3.75%. It was one of the few equity markets that did not decline. The latest polls show Bolsonaro enjoying some last minute momentum and expanding his lead to almost 38% to 24% for his leaving rival Haddad, from the Workers’ Party.

Some seem to think that polls are not capturing the full antipathy for the Workers’ Party and the Bolsonaro could get a majority. Barring this, which must be regarded as the most likely scenario, and no candidate secures a majority, a run-off will be held on October 28. This is too long for the market to sustain this momentum, though Bosonaro enjoys a narrower lead in a head-to-head contest.

The economy has not fully recovered from the 2015-2016 slump that saw output fall more than 7%. The budget deficit is expected to be over 7% this year, yet growth is tracking below 2%. The traditional political elite is in dispute. It is not only struggling to deliver the economic goods, and all that that implies, but the corruption appears to have reached intolerable levels. The previous president was impeached and removed. The one before was banned from running for President. The current president and 40% of Congress are under investigation.

The focus on financial variables should not obscure another important macro development, the rally in oil prices. The price of the front-month light sweet crude oil rose 30% in H2 17 and 22% in H1 18. It dipped slightly in Q3 (1.2%) though recouped it in full last week. Just like the decline in from mid-2014 through Q1 16 was a powerful economic force, the recovery, which is likely not over, even if there is some near-term consolidation, will also generate benefits and losses. The dollar’s appreciation exacerbates the cost to many oil importers whose currencies have depreciated. It boosts headline measures of inflation and many central bank target it rather than as the Fed does a core rate that excludes energy (and food). It risks slowing world growth, which may have already seen a cyclical peak. The World Bank and IMF are expected to revise down their growth forecasts at this week’s gathering.

The inability or unwillingness of other countries to boost output sufficiently to offset the loss of Iranian supply in the face of the US embargo is widely understood explanation. Some observers are suspicious of the extent of Saudi Arabia’s real capacity. As recently as the middle of last week, the US State Department urged OPEC to tap its reserves, something the US has also been reluctant to do. Separately, note the US oil rig count slipped for a third consecutive week, the longest streak in a year.

Tags: #USD,$CNY,$EUR,brl,Featured,Italy,newsletter,OIL