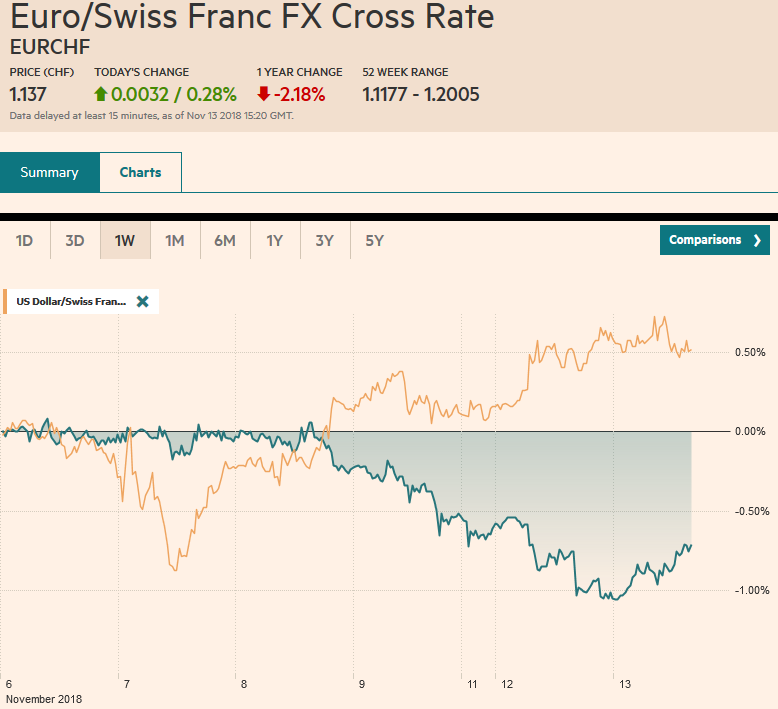

Swiss Franc The Euro has risen by 0.28% at 1.137 EUR/CHF and USD/CHF, November 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The US dollar has a heavier bias against most of the major and emerging markets currencies, but the pullback is shallow, and the greenback’s underlying strength is still evident. Asian equities were mixed. Concern that Apple may be reducing orders weighed on suppliers, but news that China and US trade talks are resuming boosted sentiment, allowing Chinese stocks to recover helped lift the Australian and New Zealand dollars. All the major industry groups in Europe’s Dow Jones Stoxx 600 are higher but energy as oil prices reversed lower

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, AUD, CAD, EUR, Featured, GBP, JPY, newsletter, SPX, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.28% at 1.137 |

EUR/CHF and USD/CHF, November 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US dollar has a heavier bias against most of the major and emerging markets currencies, but the pullback is shallow, and the greenback’s underlying strength is still evident. Asian equities were mixed. Concern that Apple may be reducing orders weighed on suppliers, but news that China and US trade talks are resuming boosted sentiment, allowing Chinese stocks to recover helped lift the Australian and New Zealand dollars. All the major industry groups in Europe’s Dow Jones Stoxx 600 are higher but energy as oil prices reversed lower yesterday following US President Trump’s complaints about the Saudi decision to export 500k few barrels of oil a day starting next month. Brent is trading near $69, and WTI is around $59. Italian stocks and bonds are underperforming today as the market expects the EC to begin excessive deficit procedures as the revisions to the budget proposals are not thought to be sufficient. |

FX Performance, November 13 - Click to enlarge |

Asia Pacific

There are two main talking points in Asia today. The first is industry specific. Concerns that iPhone suppliers may be experiencing a significant cut in orders spurred a wave of selling in the Apple ecosystem. The Nikkei gapped lower, and although it managed to close near session highs, it was still off 2%, the most in three weeks.

The second talking point helped bolster sentiment, aiding the recovery in the Chinese markets, and by extension, several other markets as well. Reports indicate that Chinese Vice Premier Liu He and US Treasury Secretary Mnuchin have resumed trade talks ahead of the G20 summit on November 30-December 1 where the two presidents will meet. At the risk of being cynical, investors are exaggerating the significance. Yes, on one level talking is better than not. However, China has been willing to talk throughout, while the US complains that China has not made serious counteroffers to US demands. It appears Chinese officials do not want to get into the “Art of the Deal” dynamics, where one side make strong demands and expects the other to draw close to it in a compromise.

Moreover, Chinese officials appear to feel betrayed by the experience earlier this year when it thought there was an agreement that it would buy more US goods to close the bilateral trade imbalance. It was negotiated with the US Treasury Secretary and later rejected by the US President. As trade adviser, Navarro, a hawk, warned yesterday, on he and the president should be engaged in trade negotiations. Chinese officials seem to recognize that trade policy in the Trump Administration is not set by the Treasury Department. The markets seem to be clutching to straws, and if we are right, the disappointment will be palpable.

The has been in a roughly JPY113.60-JPY114.20 range for the better part of the past three sessions and today. The US dollar is pushing against the upper end of the range in the European morning. The next immediate technical target is near JPY114.50, where a $375 mln option is struck that will expire today. The Australian dollar recovered from an eight-day low near $0.7165 to retake the $0.7200 in Asia, but the momentum faded in Europe. There is a large (A$1.7 bln) option struck there ($0.7200) that will be cut today.

Europe

Later today, Italy will formally respond to the EC’s demand that it revises its budget to bring it more in line with previous agreements and consistent with efforts to reduce the debt over time. Italy runs a primary budget surplus (which excludes debt servicing costs). The new government insists on three measures that will produce a larger deficit, a new income program for poor, not just unemployed, the introduction of tax simplification, which would also be a cut in taxes, and rolling back the increase in the pension age. It would not be the first time that Italy has been subject to excessive deficit proceedings. The process could ultimately lead to a fine (~0.2% of GDP), but that is more of a 2019 story. Meanwhile, Italy did manage to raise 5.5 bln euros in bond sales today as the premium over Germany for 10-year funding, widened above 300 bp for the first time this month.

The EC seems to think that negotiations with the UK are in the final stages, but Prime Minister May is not quite ready to force a cabinet decision. She is still not content with the EU’s draft that does not allow a date certain for the UK to leave the customs union, which is a backstop for avoiding a hard border between either the Republic of Ireland and Northern Ireland or between the UK and Northern Ireland. Neither is acceptable. That said a breakthrough is thought necessary in the next few days to allow a special summit later this month that would formalize the agreement. At the same time, May’s domestic challenges are formidable as her strategy is antagonizing both the hard Brexit camp but also members of the more pro-EU wing of the Conservative Party.

The UK labor market report was mixed. The claimant count rose by 20k, and the unemployment rate rose to 4.1% from 4.0% (ILO three-months, year-over-year). However, average earnings growth firmed to 3% from a revised 2.8% (initially 2.7%) and excluding bonuses, ticked up to 3.1% from 3.0% (three-months year-over-year). Inflation figures will be reported tomorrow, and CPI is running around 2.5% year-over-year.

Germany’s ZEW survey was also mixed. Although other data, like factory orders, industrial output, and the PMIs suggested that Europe’s largest economy was recovering from what the Bundesbank warned was stagnation in Q3.the ZEW survey warned that it may be a slow process. The November assessment of the current conditions collapsed to 58.2 from 70. The expectations component did not deteriorate but the improvement from -24.7 to -24.1 seems insignificant.

After falling to almost $1.1215 yesterday, the euro has stabilized and recovered to a little more than $1.1255 today. There is a 942 mln euro option struck at $1.1250 that expires today. Another option (for ~990 mln euros) at $1.13 also will be cut today. A little below $1.12 is where the last major retracement of last year’s euro rally is to be found. Sterling is also recovering a bit from yesterday’s low, which was a little below $1.2830. Today’s session high set in Europe near $1.2920. The intraday technicals suggest that both currencies could see marginal news highs in North America today.

North America

The US and Canada’s economic calendars are light. A few Fed officials speak (Kashkari, Brainard, and Harker). Outside of Kashkari, the other speakers are part of the consensus that the Fed will likely hike rates in 3-4 more times over the next year. This is what the Fed has signaled in the September dot plot and has been echoed by several officials. The new San Fransico Fed President Daly made similar remarks yesterday, suggesting a December hike at least a couple more next year. She also suggested there was room to make technical adjustments (i.e., not raising the interest on reserves as much as the fed funds target is lifted) to preserve the integrity of the target range.

The S&P 500 had gapped slightly lower before the weekend, and despite the firm close, there was strong selling yesterday and closed an earlier gap that had been created in the wake of the sharply higher opening after last week’s midterm elections. The close was poor yesterday, and back below the 200-day moving average (~2764.4). US stocks are trading higher, and the early call is for the S&P 500 to open about 0.4% higher. It needs to close back above the 200-day moving average to stabilize sentiment. Key support is seen near 2700.

It is still early, but so far today, the US dollar has not traded below CAD1.32 for the first time since June. The next upside target is the high from July near CAD1.33. The Dollar Index is in less than a 25 tick range near yesterday’s highs where were also the highs since the middle of last year. The shallowness of the pullback may be a tell that the bulls still have the upper hand despite the pressures for a technical correction.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,Featured,newsletter,SPX