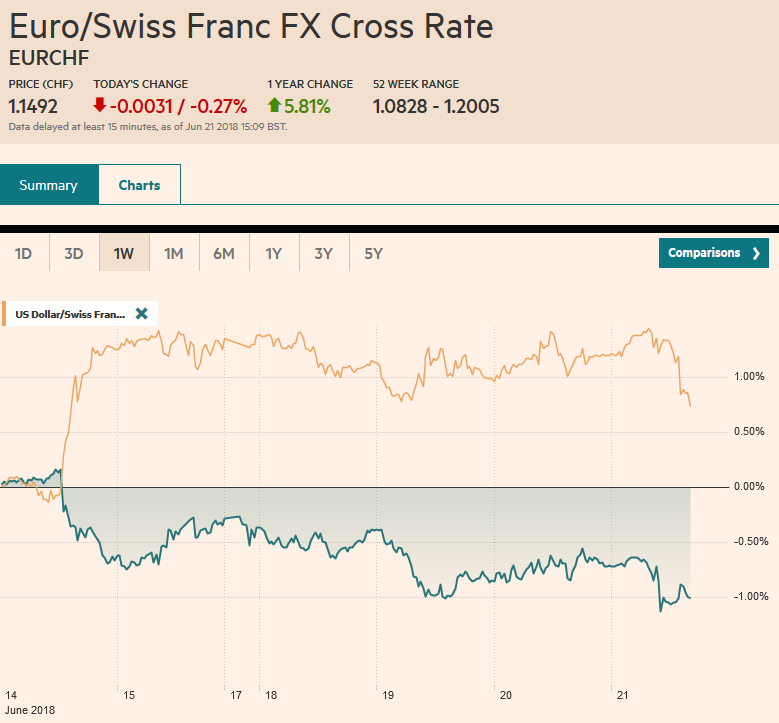

Swiss Franc The Euro has fallen by 0.27% to 1.1492 CHF. EUR/CHF and USD/CHF, June 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates There are large options that expire today at .1525 (1.2 bln euros) and .1550 (1.9 bln). Given the still substantial gross long euro positions in the futures market, it remains an open question of what level would trigger a capitulation. A break of .1500 immediately targets .1450, the 50% retracement of the euro’s rally from early last year. As painful as it may have been, we continue to view the 2017 price action as corrective in nature and place much emphasis on the US policy mix to understand the forces that are driving it. The

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CHF, Daily FX, EUR, EUR/CHF, Featured, GBP, JPY, newsletter, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.27% to 1.1492 CHF. |

EUR/CHF and USD/CHF, June 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThere are large options that expire today at $1.1525 (1.2 bln euros) and $1.1550 (1.9 bln). Given the still substantial gross long euro positions in the futures market, it remains an open question of what level would trigger a capitulation. A break of $1.1500 immediately targets $1.1450, the 50% retracement of the euro’s rally from early last year. As painful as it may have been, we continue to view the 2017 price action as corrective in nature and place much emphasis on the US policy mix to understand the forces that are driving it. The dollar’s early upside momentum against the yen was not sustained, and as North American dealers return to their posts, it is little changed from where they left it yesterday. There are also some large yen option expirations today: JPY110.30 ($700 mln), JPY110.50 ($520 mln), JPY110.65-JPY110.75 ($1.7 bln). |

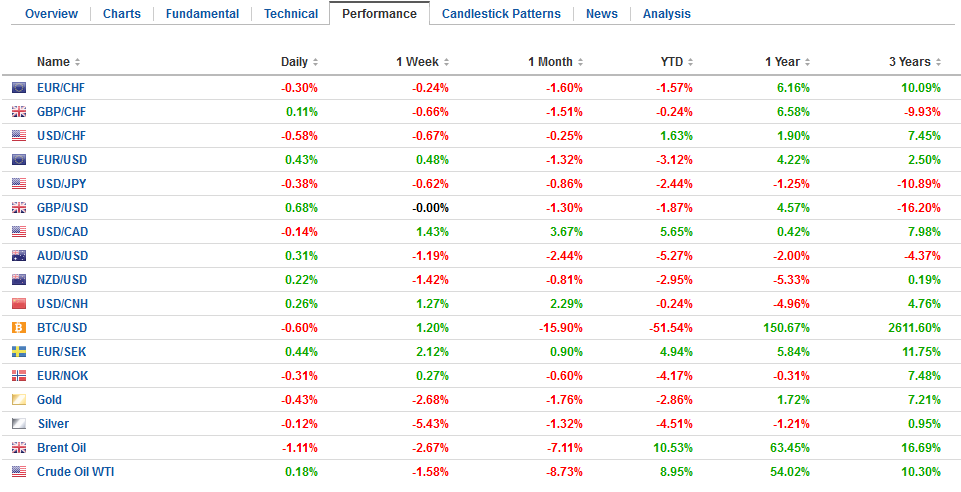

FX Performance, June 21 - Click to enlarge |

The half-hearted and shallow attempts by the currencies to recover appear to be emboldening the dollar bulls today. The greenback is higher against all major and emerging market currencies today. Demand for dollars is strong enough to offset the broader risk-off environment that is pulling stocks and core yields lower that is usually supportive of the yen. The greenback stretched to a week high near JPY110.75 today.

Asian shares were lower, and the MSCI Asia Pacific Index gave back yesterday’s 0.6% gain that snapped a five-day decline. The negative sentiment is illustrated by the fact that the Moody’s upgraded Samsung’s credit (1st in 13 years) and Korea’s shares still tumbled over 1%.

Chinese officials indicated another cut in reserve requirements was likely, but the PBOC failed to deliver today. Despite injecting more liquidity and tweaking its forward guidance, the PBOC could not prevent a further slide in Chinese shares. On the other hand, Australia continued to buck the regional trend and shrug-off worries about rising trade tensions. The S&P ASX 200 rose nearly 1% today to bring the five-day rise to a smart 3.6%.

European bourses are lower, though sterling’s weakness is underpinning the FTSE 100. Healthcare and consumer staple sectors are performing well, while financials and utilities are the largest drags. Italy’s bonds and stocks are underperforming. The equity market is off nearly one percent at midday, and the 10-year bond yield is up about 15 bp, while rest of the peripheral yields are up four-six basis points.

Two major central banks met. The Swiss National Bank left policy unchanged and repeated its refrain about the franc being over-valued and that it is prepared to intervene. Although it tweaked its inflation forecast higher, it warned of downside risks due to oil. It also recognized risks posed by Italy’s new government. The franc is trading at its best level here in June against the euro. Norway’s Norges Bank left rates steady as well, but it signaled a rate hike in September. The krone made a new marginal high for the year against the euro. However, the euro quickly recovered back above NOK9.40.

Against the dollar, the euro cannot find much traction. It has completely unwound the gains scored in the first part of the month, culminating in the initial response to the recent ECB meeting. Yesterday Draghi hinted at a material decision about the reinvesting of maturing bonds. Currently, the rules allow for flexibility and the proceeds have to be reinvested within three months. Imagine instead, it is the period is extended to say 12 months. This would appear to make the recycling that is a simple matter of course in the US into a potentially new powerful tool that could be used to support the market for longer.

Prime Minister May succeeded in yesterday’s vote in the House of Commons, but sterling drew little comfort. After being turned back yesterday from a foray over $1.32, sterling tested $1.31 today a new low for the year. May’s challenge is that the mangled compromises she has made domestically still leaves the UK far from what the EC is demanding. The Bank of England could help steady sterling today. A dissent or two from the majority’s likely decision to keep policy steady, and minutes that note the firmness of wages and inflation and that higher rates may be necessary. Still, the $1.3150-$1.3170 may be difficult to overcome. There are large options (~GBP1.15 bln) struck at $1.3200-$1.3205 that do not seem in play.

Saudi shares rose about 0.25% seemingly unfazed by the MSCI decision to include them in the Emerging Market Index in a year’s time. Perhaps some of the buying that lifted the market 5.5% over the past three months and 13.3% year-to-day was in anticipation of yesterday’s announcement. If foreign ownership will be at similar levels as seen in the UAE and Qatar, some estimates suggest Saudi Arabia may see $30-$45 bln inflows in the next two years.

Argentina is moving back into the EM Index as well. MSCI did caution that its assessment of Argentina would be reviewed if it limited accessibility (e.g., capital controls), and due to liquidity concerns, the first Argentine shares would be those that trade offshore, like US ADRS). Kuwait would be under review to be lifted to EM from frontier status. Argentina and Kuwait together account for about 37% of the frontier index.

The US economic data includes the weekly jobless claims that cover the week of the non-farm payroll survey and the Philadelphia Fed Survey for June. Investors and economists recognize that the US economy accelerated this quarter. However, there are doubts about the durability going forward. Indeed, all the major central bankers that spoke at the ECB’s confab yesterday expressed concern about the risk posed by the trade tensions.

Even Powell acknowledged hearing for the first time businesses turning cautious on investment. Ideas that China or the US will capitulate before the implementation of the tariffs on July 6 seem like a stretch. At the same time, India joined Europe and Canada in threatening to implement retaliatory tariffs shortly. Ideas that the dollar cannot rally during trade conflict or due to twin deficits flounder when its performance during the 1980-1985 period is reviewed.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CHF,$EUR,$JPY,Daily FX,EUR/CHF,Featured,newsletter,USD/CHF