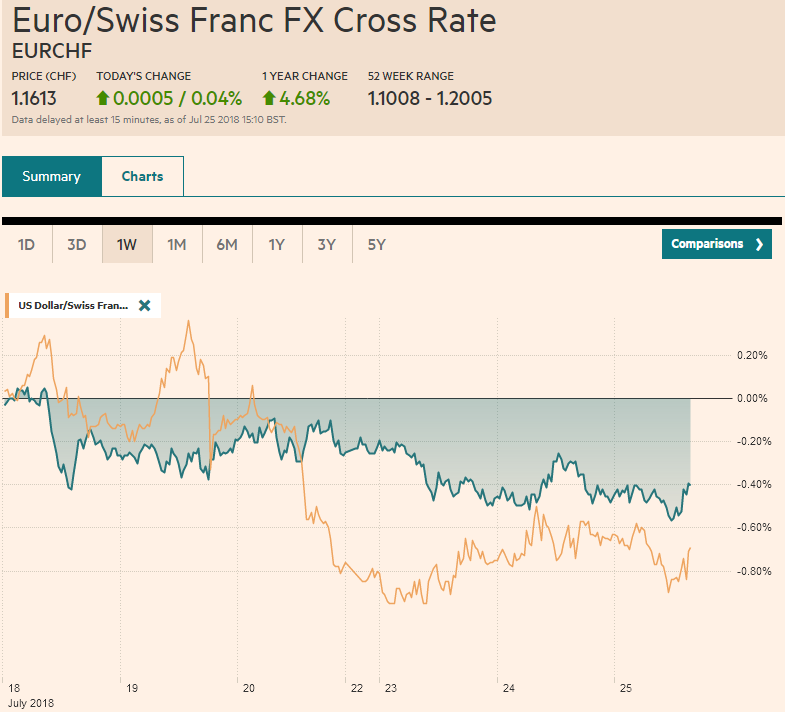

Swiss Franc The Euro has risen by 0.04% to 1.1613 CHF. EUR/CHF and USD/CHF, July 25(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The US dollar is trapped in narrow trading ranges. That itself is news. At the end of last week ago, the US President seemed to have opened another front in his campaign to re-orient US relationships by appearing to talk the dollar down. Contrary to fears, and media headlines of a currency war, the dollar is fairly stable. And, looking at at the fed funds futures strip, if anything, the market is pricing in a slightly greater chance of a two more rate hike this year than it was before the President spoke. Sterling has edged higher,

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, Australia Consumer Price Index, EUR, Eurozone M3 Money Supply, Featured, GBP, Germany IFO Business Climate Index, JPY, newsletter, SPY, TLT, U.S. New Home Sales, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.04% to 1.1613 CHF. |

EUR/CHF and USD/CHF, July 25(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is trapped in narrow trading ranges. That itself is news. At the end of last week ago, the US President seemed to have opened another front in his campaign to re-orient US relationships by appearing to talk the dollar down. Contrary to fears, and media headlines of a currency war, the dollar is fairly stable. And, looking at at the fed funds futures strip, if anything, the market is pricing in a slightly greater chance of a two more rate hike this year than it was before the President spoke. Sterling has edged higher, though also in narrow ranges. Reports that Prime Minister May is taking charge of the negotiations has been understood by the market as favoring a softer Brexit. This is consistent with the apparent pattern for sterling to gain on soft Brexit hopes and weaken on hard exit or an exit without an agreement. Sterling is knocking against the 20-day moving average (~$1.3175). A move above there would target $1.3300. The dollar has thus far remained below yesterday’s high against the yen (~JPY111.50) and has not risen about the previous session in a week. It has held above yesterday’s low (~JPY110.95) which was above Monday’s low (~JPY110.75). However, given the price action and softer US yields, the greenback looks a bit vulnerable. Although the media and short-term traders had to take notice of Trump’s comments, other countries did not take the bait. There is no currency war, and the Federal Reserve’s independence is intact. At the same time, the dollar has not been able to regain the momentum that it had before Trump’s comments. It continues to consolidate. The euro has been confined to about a quarter-cent range. It is firm near $1.17 where is a 927 mln euro expiring option is struck. There are another billion euros on a $1.1750 strike that is also expiring. Note that there he $1.17 level is a popular option strike and there is another expiration there tomorrow and 1.4 bln euros on Friday. |

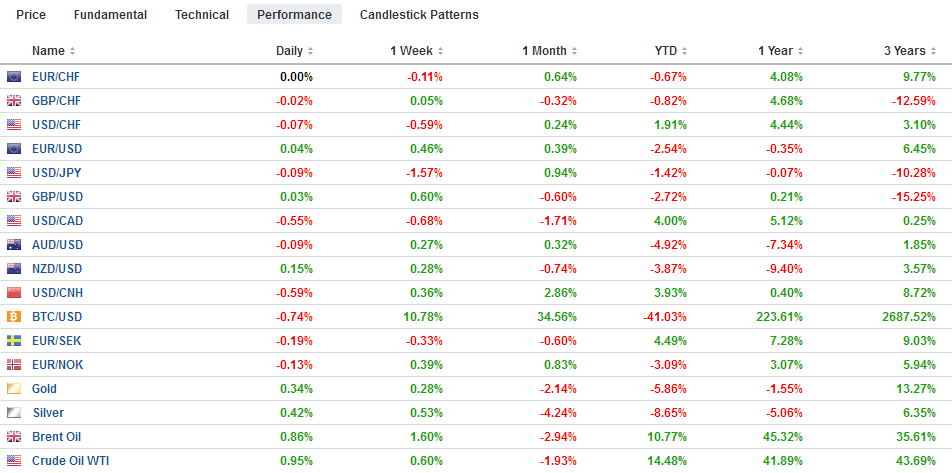

FX Performance, July 25 - Click to enlarge |

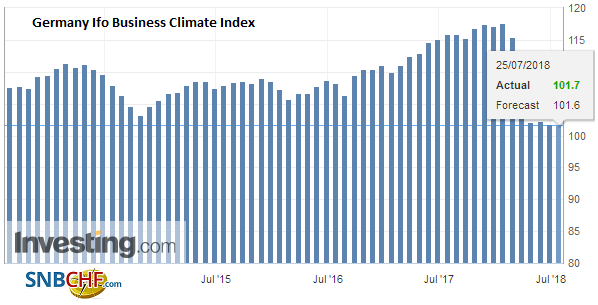

GermanyThe German IFO failed to stir the market. The business climate measure slipped but not as much as had been expected. Still, it has not risen since last November. The current assessment edged up to 105.3 from 105.2. This seems consistent with the improved flash PMI. The expectations component eased more than expected. It is the lowest since March 2016. The EC’s Junker is in Washington today to talk trade. Trump has provocatively called for the end of all tariffs, subsidies, and barriers. The US and Europe had been negotiating a free-trade agreement (TTIP), but domestic political considerations ended the talks. Given Trump’s distaste for multilateral agreements, many suspect Trump’s call is primarily meant to shake things up and keep the adversary off-balance. Eighteen months into the Trump presidency, there can be no mistake. His trade initiative is not just aimed at China, like many thought. Auto imports, which are under investigation on national security grounds, is more of an issue for Europe, Canada, Japan, and Mexico than China. Tariffs on autos and auto parts would be significantly disruptive than the actions seen so far. |

Germany Ifo Business Climate Index, July 2018(see more posts on Germany IFO Business Climate Index, ) Source: Investing.com - Click to enlarge |

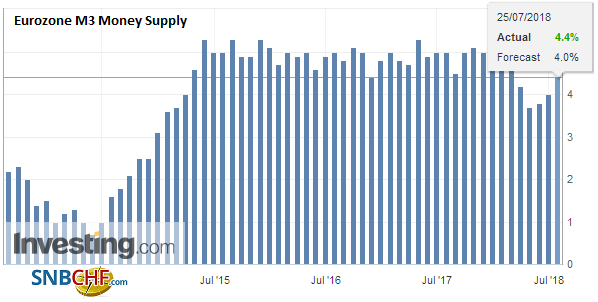

EurozoneThe ECB reported money supply M3 growth accelerated to 4.4% from 4.0%. It is the third consecutive increase. The pace peaked last September at 5.2%, and last June stood at 4.9%. Lending to firms increased to 4.1% year-over-year from a 3.7% pace in May. This is the strongest pace since 2009. Lending to households was unchanged at a 2.9% pace. The ECB meets tomorrow, and the data coupled with the GDP implications of the PMI will likely underpin its confidence. Brexit and trade issues will likely be featured at the press conference. |

Eurozone M3 Money Supply YoY, June 2018(see more posts on Eurozone M3 Money Supply, ) Source: Investing.com - Click to enlarge |

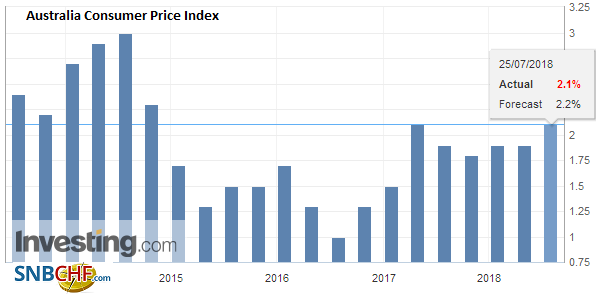

AustraliaAustralia reported a slightly softer than expected Q2 CPI. It rose 0.4%, matching the Q1 rise but softer than the 0.5% that economists expected. It was a soft 0.4% as it was rounded up from 0.38%. The year-over-year rate did tick up to 2.1% from 1.9%. The trimmed and weighted median measures met expectations. The Australian dollar initial was pushed off the perch it had reached near $0.7460 and found bids a little below $0.7400, where there is an A$680 mln option expiring today. Views on the outlook for the RBA is unaffected by today’s news. |

Australia Consumer Price Index (CPI) YoY, Q2 2018(see more posts on Australia Consumer Price Index, ) Source: Investing.com - Click to enlarge |

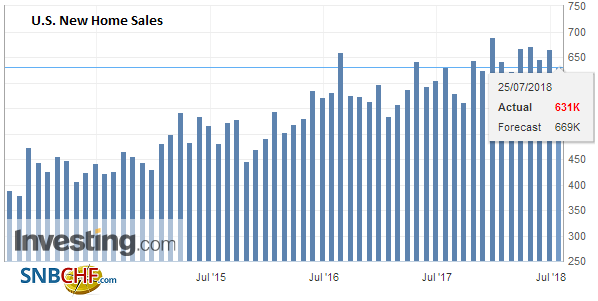

United StatesThe US reports new home sales. Following disappointing housing starts and existing home sales, another soft housing report out not to surprise. New homes sales remain near the cyclical peak. Several large US multinational companies report earnings. The S&P 500 gapped higher yesterday, and although the early momentum was not sustained, a small gap remains (~2808.6 to ~2811.1). The gap may draw prices, but it remains unfilled, it would be seen as a bullish indicator. |

U.S. New Home Sales, June 2018(see more posts on U.S. New Home Sales, ) Source: Investing.com - Click to enlarge |

Japan

Japan reported strong department store sales, but the market is more focused on possible changes of the BOJ’s policies. The yield on the 10-year JGB eased almost a single basis point to about 0.065% yield. US and European benchmark 10-year yields are 1-2 bp lower, while the peripheral yields are off a bit more. Although Chinese mainland shares could not maintain the upside momentum, Japanese shares managed to hold on to modest gains, extending yesterday’s gains by almost 0.5%, and helping lift the MSCI Asia Pacific Index for the second consecutive session. Foreign investors were net sellers of Korean and Taiwanese shares today.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$EUR,$JPY,$TLT,Australia Consumer Price Index,Eurozone M3 Money Supply,Featured,Germany IFO Business Climate Index,newsletter,SPY,U.S. New Home Sales