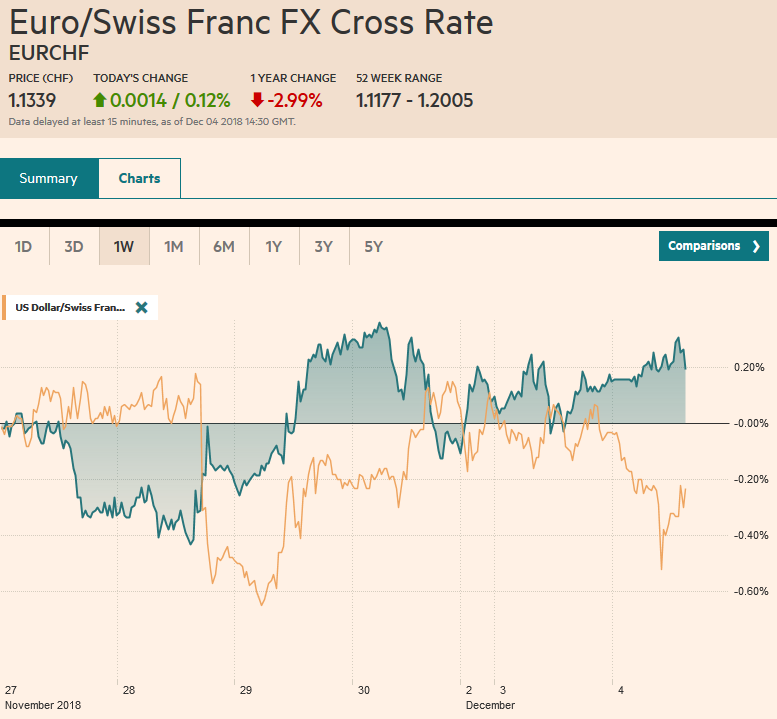

Swiss Franc The Euro has risen by 0.12% at 1.1339 EUR/CHF and USD/CHF, December 04(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Equity markets are unable to build on yesterday’s advance, but bonds and oil are extending gains. The dollar remains on the defensive and is off again all the major currencies. The lack of a joint statement over the weekend by the US and China and seemingly different interpretations of what was agreed leaves investors in a lurch. Saudi Arabia noted that there has been no agreement to cut output, but investors are anticipating one and have extended oil’s recovery after last month’s shellacking. A new twist in the Brexit drama emerged

Topics:

Marc Chandler considers the following as important: $CAD $GBP, 4) FX Trends, AUD, EUR, Featured, GBP, JPY, MXN, newsletter, SPX, TLT, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.12% at 1.1339 |

EUR/CHF and USD/CHF, December 04(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Equity markets are unable to build on yesterday’s advance, but bonds and oil are extending gains. The dollar remains on the defensive and is off again all the major currencies. The lack of a joint statement over the weekend by the US and China and seemingly different interpretations of what was agreed leaves investors in a lurch. Saudi Arabia noted that there has been no agreement to cut output, but investors are anticipating one and have extended oil’s recovery after last month’s shellacking. A new twist in the Brexit drama emerged as opposition parties first debate whether the government is in contempt of Parliament for not releasing the legal advice underpinning the Withdrawal Agreement. Asian equities mostly fell after strong gains yesterday. China and Hong Kong markets were the chief exceptions. European bourses are lower and the national indices are working on filling the gaps created by yesterday’s higher opening. The Dow Jones Stoxx 600 is off about 0.30% in late morning turnover after gaining 1% on Monday. The S&P 500 jumped higher yesterday too and looks set to try to enter and possibly fill the gap today, which extends to around 2761. |

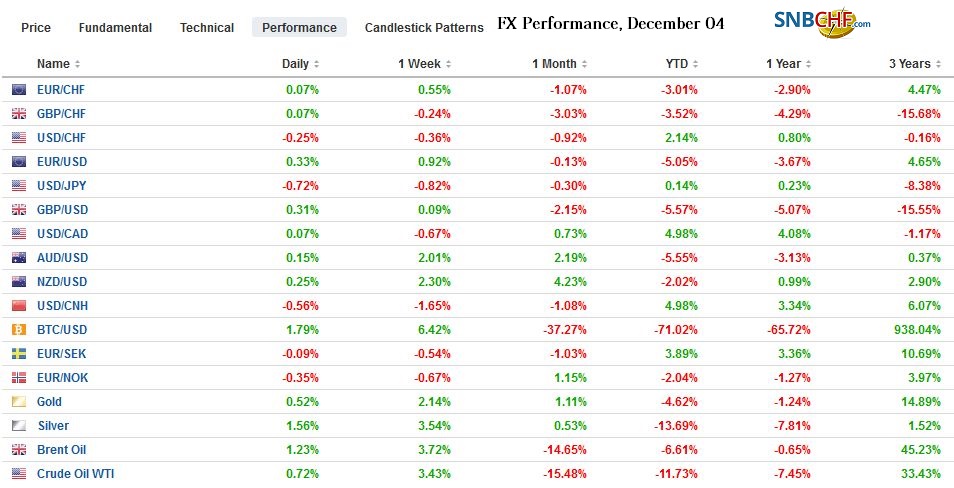

FX Performance, December 04 - Click to enlarge |

Asia-Pacific

With Chinese President Xi visiting the Iberian Peninsula before returning home, officials have not formally responded to the various claims the US is making regarding the weekend agreement. There are several accounts in the media showing the contrasting statements of the US and China. The US statements themselves are changing. Initially, the US said that there would be negotiations over the next 90-days, during which time additional tariff action would not take place. Late yesterday, Kudlow indicated that 90-day period begins January 1. The Chinese statements do not appear to show a reference to the 90-day term at all. Kudlow also suggested that an agreement on intellectual property rights was close, while Chinese officials have denied a systematic problem. As if prepared for release after the meeting between the two presidents, China announced new punishments for violations of intellectual property rights today. Will this satisfy transactional-oriented US officials or will they emphasize the gap between China’s declaratory and operational policies?

The 10-year government bond yield eased a few basis points to slip below 3.35%, its lowest rate in 20 months. The yuan rose 1.1% yesterday and nearly half as much today for its biggest two-day advance in at least a decade. The dollar has fallen through the 100-day moving average against the yuan (~CNY6.87) for the first time in since April. Initial support now is seen near CNY6.80. The 200-day moving average is closer to CNY6.62.

The Reserve Bank of Australia left rates on hold as it has done since the August 2016. The statement dropped the reference to weak wage growth, but the RBA is in no hurry to change policy. Despite the “welcome” increase in wages, growth in household income is poor, and debt levels are high, and the housing market continues to weaken. Separately, Australia reported a slightly wider than expected current account deficit for Q3, which still represented a substantial improvement from Q2 (-A$10.7 bln vs. a revised -$12.1 bln-from -A$13.5 initially).

After gapping higher yesterday, the Australian dollar held above the gap in early Asia and is knocking on $0.7400 near midday in Europe. The $0.7450 area corresponds to a retracement objective of this year’s decline. The New Zealand dollar, which also gapped higher yesterday, is motoring ahead to reach its best level since mid-June and appears to be reaching for $0.7000. The US dollar has been sold through last week’s low against the yen (~JPY112.90). Initial chart support is seen near JPY112.50, and there are roughly $1.1 bln in options struck at JPY112.55 and JPY112.70 that are expiring today.

Europe

There are three macro developments in Europe to note. First, the UK Parliament debate on the Withdrawal Agreement begins today but not before the opposition squeeze the government one more time. The issue is whether the government is in contempt of Parliament for not releasing the entire legal opinion behind the agreement. The Democrat Unionist that the Tories rely on to govern voted with the opposition. Second, the French government appears on the verge of capitulating to pressure on reverse itself on the petrol tax increase. Still, the French government may not fully grasp the situation yet. It seems to see it as a reason to speed up neoliberal reforms, including allowing business more flexibility to make temporary layoffs and stay open on Sundays. Finance Minister Le Maire says that he is prepared to cut spending (read government programs and benefits) if room is needed to deliver the tax cuts. Third, Italian Prime Minister Conte appears to be emerging out of the shadow of his two deputies that head the coalition parties and may be negotiating a compromise between Italy and the EC. Italy’s 10-year yield is consolidating after dropping around 55 bp since earlier in the month when it reached a peak above 3.70%, as fears of a repeat of the Greek crisis eased and redenomination risk also slackened.

The European Central Bank made some minor tweaks in the capital key, which it is required to do every five years. The capital key is determined by population and GDP. It is used to settle various issues, including contributions to the EU, the allocation of assets purchases under QE, and rotating voting rights at the ECB. Sixteen countries have a higher share, and 12 lower. Interestingly EMU countries accounted for a smaller overall majority (69.6176% vs. 70.3915%) compared with the non-EMU countries (30.3824% vs. 29.6085%). More than 2/3 of the decline of the EMU’s share is accounted for by Italy. Ironically, the UK saw among the largest increases (14.3374% vs. 13.6743%), though we are still talking about fractions of a percent. There are some questions about which capital key the ECB will use for reinvesting the proceeds of maturing bonds, the capital key it used for the purchases or the new capital key. The difference seems minor, but it does not mean it won’t be vigorously debated. Under the new capital key, some calculations suggest, that the Eurosystem would purchase around 800 mln less Italian bonds.

The euro held $1.13 before the weekend and is pushing above $1.14. There is an option there for about 840 mln euros that expires today. A move above $1.1450 would lift the technical tone. An option struck there for a little more than 410 mln euros rolls off today, as well. That said, the intraday technicals warn that session high may be in place. Sterling is also firm, but the momentum that carried it to a three-day high (~$1.2840) may b stalling ahead of last week’s high (~$1.2860).

North America

There is a light economic calendar for US, Canada, and Mexico today. US markets will be closed tomorrow. The S&P 500 gapped higher yesterday and the anticipated lower opening today would hold above the gap (~2760.9-2773.4). Last month’s high was set a little above 2815. The US 10-year yield has continued to fall. After being turned back from 3.05% yesterday and finishing at 2.97%, the yield fell to almost 2.93% today. The December note futures contract is at its highest price in three months.

The Dollar Index is threatening the uptrend line from September near 96.60 today. Intraday technicals are stretched. The US dollar is in narrow ranges near yesterday’s lows against the Canadian dollar. The greenback appears to be finding support near CAD1.3160 but needs to resurface above CAD1.3220 to be anything noteworthy. The US dollar is consolidating at the upper end of yesterday’s range against the Mexican peso. It is near the middle of the MXN20.00-MXN20.50 range that contained most of last month’s price action.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD $GBP,$EUR,$JPY,$TLT,Featured,MXN,newsletter,SPX