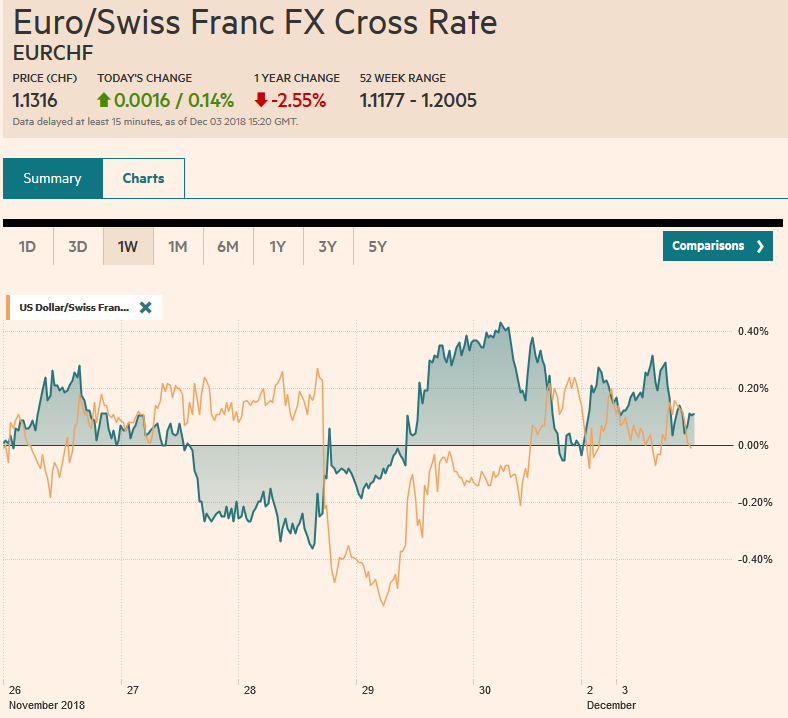

Swiss Franc The Euro has risen by 0.14% at 1.1262 EUR/CHF and USD/CHF, December 03(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The US and China kept their trade guns cocked at each other but offered the last opportunity for a negotiated settlement before escalation. What is billed as a 90-day freeze on tariff increases is really only 60 days beyond January 1 when Trump had threatened to increase the 10% tariff on 0 bln of Chinese goods to 25%. The US and China could not agree on a joint statement, and there appear to be differences between the two on what was agreed. Moreover, early today Trump tweeted that China would reduce and remove tariffs on US

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, EUR/CHF, Featured, GBP, JPY, MXN, newsletter, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.14% at 1.1262 |

EUR/CHF and USD/CHF, December 03(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The US and China kept their trade guns cocked at each other but offered the last opportunity for a negotiated settlement before escalation. What is billed as a 90-day freeze on tariff increases is really only 60 days beyond January 1 when Trump had threatened to increase the 10% tariff on $200 bln of Chinese goods to 25%. The US and China could not agree on a joint statement, and there appear to be differences between the two on what was agreed. Moreover, early today Trump tweeted that China would reduce and remove tariffs on US autos, which had not been announced previously. At the same time, Russia and Saudi Arabia agreed to extend their pact, boosting the likelihood that OPEC+ will announce output cuts later this week. Efforts to support the oil market also came from an unexpected source. The Canadian province of Alberta announced a 325k barrel a day cut (8.7%) starting in January. Equities have rallied strongly. The MSCI Asia Pacific Index nearly matched last week’s 2% gain. China, Hong Kong, Taiwan, and Singapore markets led the advance, gaining more than 2% each. India was the sole exception. The rupee is also underperforming in the face of the US dollar’s pullback. Higher oil prices appear to be the drag. Oil has rallied 4-5% after last month’s 22% plunge. European shares are higher, and the Dow Jones Stoxx is up more than 2% in late morning turnover in what could be the biggest advance in eight months. The high beta dollar-bloc and Scandi currencies are leading the move against the US dollar. Among emerging markets currencies, the South African rand, the Mexican peso, and Chinese yuan are up over 1%. |

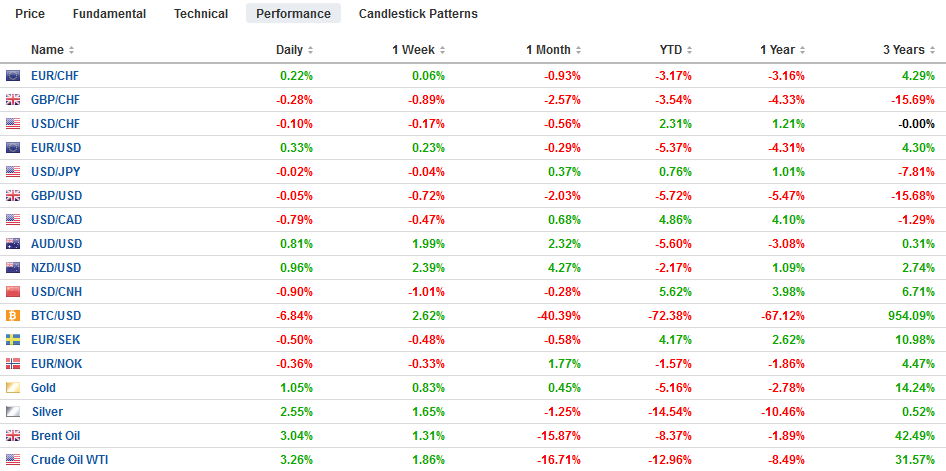

FX Performance, December 03 - Click to enlarge |

Asia Pacific

China reportedly agreed to step up its purchases of US agriculture and industrial goods (including energy) immediately. This is one of the measurable outcomes even though the amounts were not agreed. China also agreed to classify fentanyl as a controlled substance, which would allow greater over it, which has been a scourge in America (and Canada). Neither the US nor China claimed any change in the Made in China 2025 initiative or US arms deals with Taiwan.

Separately, Caixin reported its manufacturing PMI edged higher in November to 50.2 from 50.1. Recall that the official measure eased to 50.0 from 50.2. The Caixin measure picks up more small businesses than the official PMI. Chinese officials cut the required margin to trade futures on equity indices.

The Japanese economy contracted in Q3, and after the capex details, the weakness may be deeper than initially reported. Next week, the -0.3% initial estimate could be revised to -0.5%. Capital spending was considerably weaker than expected. The 4.5% increase compares with median forecasts (Bloomberg survey) of 8.5% after rising 12.8% in Q2. Corporate profits were also weak. The 2.2% rise pales in comparison with expectations of a 14% increase (almost 18% in Q2). However, this is history, and the economic weakness was largely a function of the disruption caused by natural disasters. An economic recovery has already begun as 2.9% surge in October industrial output (preliminary figures reported last week) illustrate. The November manufacturing PMI slipped to 52.2 from 52.9 in October. New orders fell back to July levels warning that the best of the recovery may be behind it.

The dollar initially traded higher against the yen, reaching JPY113.85 in early Asia. It trended lower and returned to the pre-weekend lows near JPY113.35. A break below there would undermine the technical tone. Last week’s range was roughly JPY113.20 to JPY114.05. There are $1.3 bln in expiring options at JPY113.15-30 today and nearly the same amount between JPY113.70 and JPY114.00.

The Australian dollar gapped higher, and that gap appears on the weekly bar charts, making it potentially even more significant. Last week’s high was $0.7344, and Bloomberg has today’s low at $0.7348. Тhe last session’s high was near $0.7325. The upside momentum seemed to falter in the European morning, and the gap may attract prices. There is are A$1.1 bln in $0.7350 strikes that expire today. The RBA meets tomorrow, and it is widely seen on hold for some time.

Europe

The EMU November PMI was a little better than the flash estimate suggesting that the worst of the soft patch may be abating, though Italy is still problematic. The final manufacturing PMI came in at 51.8 compared with the 51.5 flash reading and 52.0 in October. German and French preliminary readings were revised higher, while Spain exceeded expectations (52.6 from 51.8 in October and is highest since August. Italy, however, went the other way. The contraction deepened to 48.6 from 49.2. A reading below 50 is associated with falling output.

The UK manufacturing PMI also surprised on the upside, rising to 53.1 from 51.1. It recovers from the sharp fall in October. It stood at 53.7 in September and averaged 53.5 in Q3. The debate in the parliament over the Withdrawal Bill begins tomorrow, culminating in a vote on December 11. All the opposition parties are opposed as is the Tory ally the DUP. Among the Tories, as 60-100 are expected to vote against the government. Both wings, the eurosceptic and well as the europhile are opposed. Gyimah, the Science Minister and pro-Europe, resigned before the weekend.

The euro is trading within the pre-weekend range (~$1.1305-$1.1400). It reached session highs near $1.1380 in late Asia. There is a 506 mln euro option at $1.1390 that will be cut today. Initial support is seen in the $1.1320-30 area. Despite the widespread demonstrations in France against President Macron’s agenda, including fuel tax, investors have shown little reaction. French 10-year bond yield is up about half a basis point more than Germany today, and both the DAX and CAC are up a little more than 2%. Sterling initially rose through its pre-weekend high (~$1.2810) and peaked ahead of $1.2850 before falling out of favor. It briefly slipped through the pre-weekend low (~$1.2735). The low from last week was about $1.2725, which nearly matches the month’s low. The October low was nearer $1.2700. The low for the year was set in mid-August around $1.2660.

North America

Both the US ISM and PMI will be reported today. November auto sales will also be reported. The data will give economists’ data set another addition ahead of the ADP private sector jobs estimate to forecast the week’s highlight in the form of the monthly non-farm payroll report. Most economists project a slowing of US activity after the 3.5% Q3 pace. Still, growth is expected to be above trend. At least five Fed officials speak today. We suspect Governor Brainard’s comments may be the most interesting. She has drawn an arguably meaningful distinction between a short-run neutral rate and a longer-term neutral rate that might be helpful in contemplating the Fed’s challenge.

Markit reports Canada’s November PMI. The Bank of Canada meets this week. No one expects a change in policy until early next year, and even that is being scaled back. Excluding inventories and exports, final domestic demand unexpectedly contracted in Q3. Canada will also report jobs data at the end of the week. Full-time job growth is averaging about a third of last year’s pace, and wage growth has been slowing since May. The US dollar gapped lower against the Canadian dollar and has continued to fall. After closing near CAD1.33 before the weekend, the greenback has tumbled to CAD1.3160 in the European morning, where bids have been uncovered. The 20-day moving average, which the US dollar has not closed below since mid-October, is found near CAD1.3220.

The Mexican peso is up about 1.5%, the most in two months. Business-friendly comments by AMLO the new president and the risk-off sentiment has seen the dollar slump from near MXN20.37 at the close before the weekend to almost MXN20.00 today. The market may be getting ahead of itself as intraday technicals are stretched. US dollar resistance is seen now near MXN20.20.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,Featured,MXN,newsletter,USD/CHF