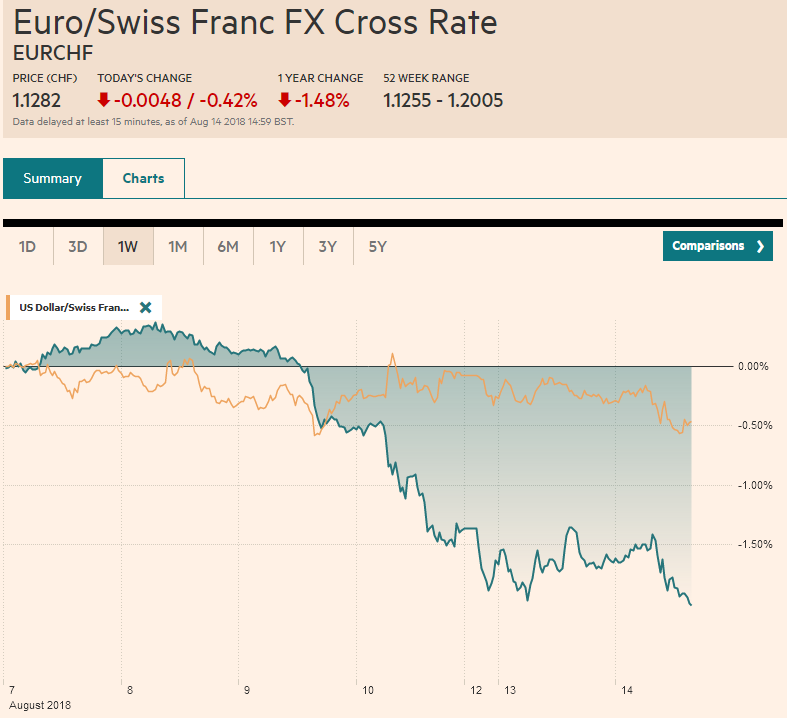

Swiss Franc The Euro has fallen by 0.41% to 1.1282. EUR/CHF and USD/CHF, August 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Corrective pressures grip the capital markets today, helped by the easing of the selling pressure on Turkey, but its more a respite than a relief as no new policy initiatives are behind the lira’s upticks. The implication of this is that it is unlikely to last. In fact, the dollar’s low in early Europe a just above TRY6.41 after trading a little above TRY7.23 yesterday may be about the most that can reasonably be expected. And not all countries are participating. India’s rupee and Indonesia’s rupiah fell to record lows, spurring reports

Topics:

Marc Chandler considers the following as important: $CNY, $INR, $TRY, 4) FX Trends, ARS, AUD, CAD, EUR, Featured, GBP, Germany Gross Domestic Product, newsletter, TLT, U.K. Unemployment Rate, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.41% to 1.1282. |

EUR/CHF and USD/CHF, August 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesCorrective pressures grip the capital markets today, helped by the easing of the selling pressure on Turkey, but its more a respite than a relief as no new policy initiatives are behind the lira’s upticks. The implication of this is that it is unlikely to last. In fact, the dollar’s low in early Europe a just above TRY6.41 after trading a little above TRY7.23 yesterday may be about the most that can reasonably be expected. And not all countries are participating. India’s rupee and Indonesia’s rupiah fell to record lows, spurring reports of central bank intervention and only then did they recover. |

FX Performance, August 14 - Click to enlarge |

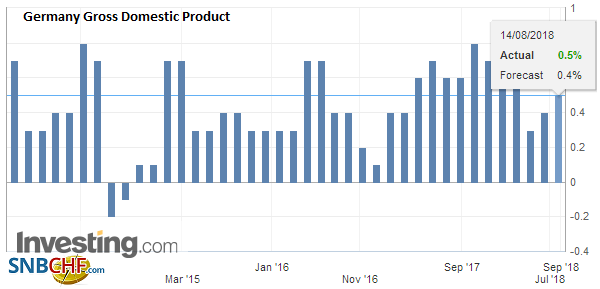

GermanyFavorable European economic data was insufficient for the euro to hold on to even modest upticks. The euro had retested yesterday’s highs near $1.1430, and stronger than expected growth from Germany (Q2 GDP 0.5%) and Q1 was revised up (0.4% from 0.3% failed to help it sustain the gains. German GDP helped spur an upward revision to the EMU GDP to 0.4% from 0.3%. Separately, the August ZEW survey, both the assessment of current conditions and expectations also improved more than expected. The euro found bids $1.1380, and corrective forces remain intact. |

Germany Gross Domestic Product (GDP) QoQ, Q2 2018(see more posts on Germany Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

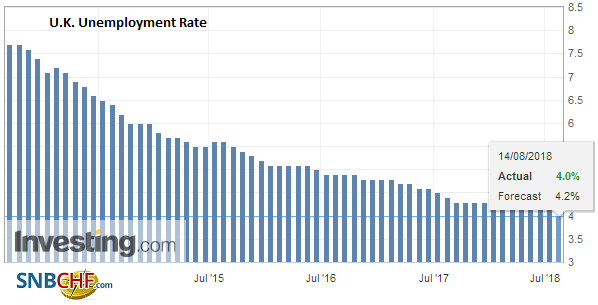

United KingdomNor was the UK data enough to deter selling into sterling’s gains that had carried it through yesterday’s high (~$1.2790) and a little past $1.2825. Sterling fell to nearly $1.2765, ahead of support seen near $1.2740. Employment growth slowed in the UK to 42k (3m/3m) from 137k. This is the slowest period since last October. `Separately, regular earnings grew 2.7%, as expected, though the May reading was revised to 2.8% from 2.7%. The unemployment rate fell to 4.0% from 4.2%. |

U.K. Unemployment Rate, June 2018(see more posts on U.K. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

On the other hand, disappointing Chinese data could not send the yuan lower, though Chinese equities are a different story. The MSCI Asia Pacific Index rose nearly 0.5%, but, Chinese stocks slipped lower. The yuan both onshore and offshore is a little firmer. China’s data-retail sales, industrial production, and fixed asset investment-were all softer the than expected. This followed the slower lending and money supply figures. The anticipation and implementation of the trade tensions may have contributed, but a broader slowdown was underway. Just as importantly, Chinese officials have already signaled a policy shift toward greater economic support.

The relaxation of market angst has weighed on the yen.The dollar already had begun recovering yesterday after trading below JPY110.20. It finished the US near JPY110.70, which, as it turns out, is the long-run average (since the end of 1989). It approached JPY111.20 today, where offers were encountered at the end of last week. The Nikkei rallied 2.3%, and the Topix tacked on 1.6%. Telecom led the rally, and while all the sectors participated, materials and financials lagged.

European equities are retracing yesterday’s loss. The Dow Jones Stoxx 600 is up about 0.4%, led by consumer staples and health care, while energy, materials and real estate are not participating. Financial are flat, but Italy’s bank index is off for a fifth consecutive session (~-0.3%). Spanish banks are slightly firmer.

The corrective mood is also evident in the bond markets, where core bond yields, including 10-year JGBs, are 1-2 bp higher, while peripheral bond yields are .lower. The US 10-year benchmark is almost two basis points higher, just below 2.90%.

There is important insight Turkey can glean from Argentina. Yesterday, Argentina surprised investors with a 500 bp increase in the key seven-day note yield to 45% and kept it there until at least October. It announced it would sell $500 mln to relieve pressure on the peso. The $50 bln IMF package is barely two-months-old.

And yet, the Argentine peso finished the day on its lows, off 2.4% to extend its slide into a sixth consecutive session. It has lost 9.5% over this run. Turkey’s key policy rate is at 17.75%. Its inflation was a little more than half of Argentina’s near 30% pace but will quicked as the lira’s depreciation works its way through the economy.

There is an important reminder for traders and short-term investors. For all practical purposes, there is no yield high enough to offset the risk of a 9.5% currency depreciation over a two-week period. Medium and long-term investors know that the exchange rate is an important part (and risk) of total returns. The variability of currencies can generate two-thirds of the returns of global bond funds and a third of the return of a global equity fund.

Turkey may not be a systemic shock to the EU, but it is still a new headwind. There are four direct channels, trade, bank loans, portfolio investment, and on the ground assets. Turkey is the EU’s fifth largest export market, and especially for capital goods, like machinery and transportation equipment. European companies had a stock of direct investment in Turkey of around $80 bln. Global banks, mostly European banks, have around $250 bln of gross exposures, without counting hedges and other offsets. Foreign investors own an estimated 60% of Turkey’s government bonds (~30% of GDP) and about a 20% of the equity market.

The North American session will be dominated by the corrective/consolidative forces that have emerged. The economic calendar is light, and US import/export prices are small beer. The NY Fed released the Q2 Household Debt and Credit Report, which always makes for sober reading., but it is not a market mover. We suspect that there is room for additional upside correction in the euro toward $1.1460 and sterling toward $1.2850. The dollar may have scope toward JPY111.40 and maybe CAD1.3045. The Australian dollar is inside yesterday’s range but could rise toward $0.7290.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$INR,$TLT,$TRY,ARS,Featured,Germany Gross Domestic Product,newsletter,U.K. Unemployment Rate