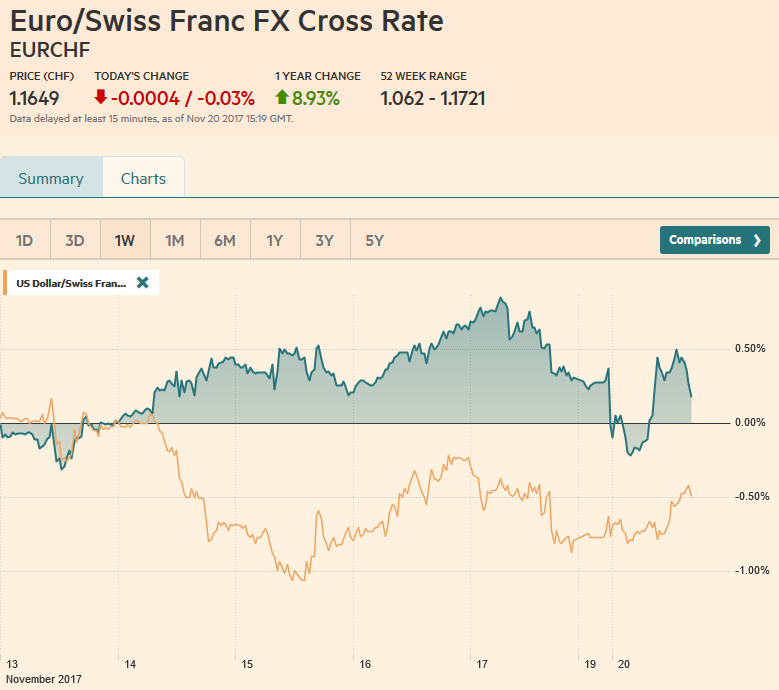

Swiss Franc The Euro has fallen by 0.03% to 1.1649 CHF. EUR/CHF and USD/CHF, November 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge CHF/GBP The Swiss Franc has seen some weakness of late as risk appetite is changing which is creating less demand for the Swiss Franc. Investors for the moment are looking at the US for better returns after a run of positive economic data from the US and on the expectation Donald Trump’s domestic infrastructure splurge could bear fruits for investors. In a sign of the times the Swiss Franc has now fallen to its lowest point against the Euro in just under three years. The Swiss Franc could be set for a volatile period against both the pound and

Topics:

Marc Chandler considers the following as important: EUR, EUR/CHF, Featured, FX Trends, GBP, Germany Producer Price Index, Japan Exports, Japan Imports, Japan Trade Balance, JPY, newsletter, TLT, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.03% to 1.1649 CHF. |

EUR/CHF and USD/CHF, November 20(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

CHF/GBPThe Swiss Franc has seen some weakness of late as risk appetite is changing which is creating less demand for the Swiss Franc. Investors for the moment are looking at the US for better returns after a run of positive economic data from the US and on the expectation Donald Trump’s domestic infrastructure splurge could bear fruits for investors. In a sign of the times the Swiss Franc has now fallen to its lowest point against the Euro in just under three years. The Swiss Franc could be set for a volatile period against both the pound and the Euro in these coming weeks. The UK continues with the Brexit negotiations which is still the big driver for sterling exchange rates. However the EU gave Britain a deadline to make sufficient progress and this ultimatum comes to an end this week. Depending on how this turns out come Friday GBP CHF is likely to see volatility. Clients looking to buy or sell Euros for Swiss Francs specifically should keep a close eye on the political situation in Germany. With coalition talks in Germany between the three parties having broken down this is creating uncertainty for Euro exchange rates. If no agreement can be found then there is a strong chance that there could be new elections although due to the process involved in doing so it would probably not be until the spring of 2018 before elections can take place. There appears to be some will from Angela Merkel to get negotiations back on track although this will inevitably mean concessions and a change of stance may not be easy to achieve within her party. Expect considerable volatility for EUR CHF as these events unfold and there may even be some repercussion for GBP CHF as Brexit is ultimately heavily linked to what happens in Germany. |

CHF/GBP - Swiss Franc British Pound, November 20 - Click to enlarge |

FX RatesNews that the attempt to forge a four-party coalition in Germany collapsed Sunday saw the euro marked down in early Asian activity. The euro fell to nearly $1.1720 in the immediate response to the news, stabilized before turning higher in early European turnover. It quickly recovered and poked through $1.1800. The pre-weekend high was seen near $1.1820. It is not clear where Germany goes from here. However, the important takeaway is that investors do not see this as a systemic issue, but a local one. Investors quickly looked past Catalonia’s secessionist push on similar grounds. Likewise, state developments in the US rarely move the markets, even large states, like New York and California. Nevertheless, we suspect the euro’s recovery has run its course, and the intra-day technicals warn of the risk of a new setback to the lows. Still, there are several options available to Germany. More compromises by the CDU/CSU and Greens to win back the FDP. The CSU/CDU could try to woo the SPD, which has thus far refused to be part of a Grand Coalition again. The CSU/CDU and Greens could form a minority government, which the FDP says they would support. The German President could reject a minority government and insist on new elections. |

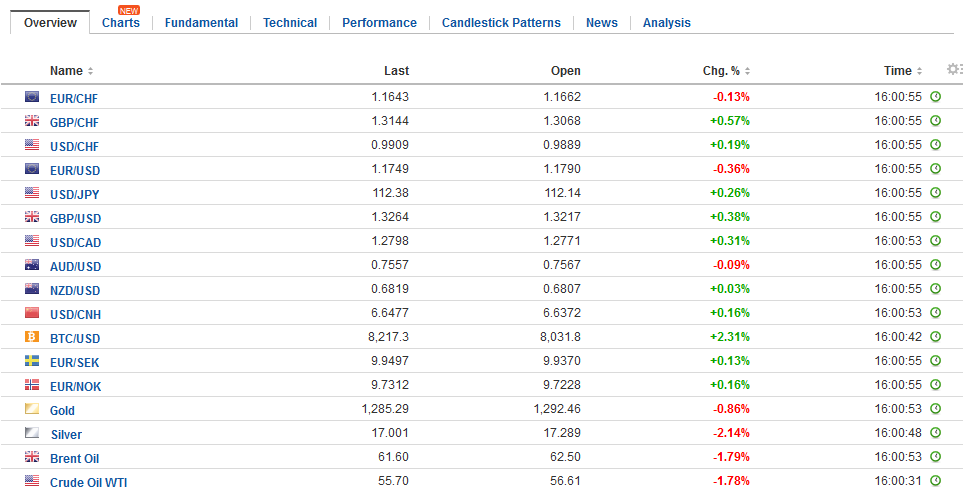

FX Daily Rates, November 20 - Click to enlarge |

| In the US, the struggle over tax reform continues. Surveys suggest the tax reform is unpopular. The Joint Committee on Taxation (Congress) estimated that under the Senate plan 65% of American households would experience higher taxes while 24% would get a tax cut. Given that the cyclical expansion remains intact, and if anything, it has accelerated, we suspect that public investment (infrastructure) is a greater priority than tax relief.

Corporate tax schedules are misleading as the effective tax rate is considerably lower. According to a US Treasury report from last year, the average tax rate paid on profits of new investment in the US was 24%, in contrast to the 35% tax schedule. Businesses in other G7 countries paid an average of 21% (weighted by the size of the respective economies). Another relevant measure is the tax take on worldwide profits. Multinationals headquartered in the US pay about 28% of their global profits in US and foreign taxes. Companies with headquarters in other G7 countries (weighted by the size of their economies) paid an average of 29%. The record profits (earnings) being reported by US companies, which explains the bulk of the equity market rally since the 2009 trough, suggest economic challenge America faces is not too high of effective taxes on US corporations. Sterling is the best performer through the European morning, gaining 0.4% against the US dollar and is recouping about a third of what it lost against the euro last week. The market is anticipating a move by the UK this week to jump-start the moribund Brexit talks. |

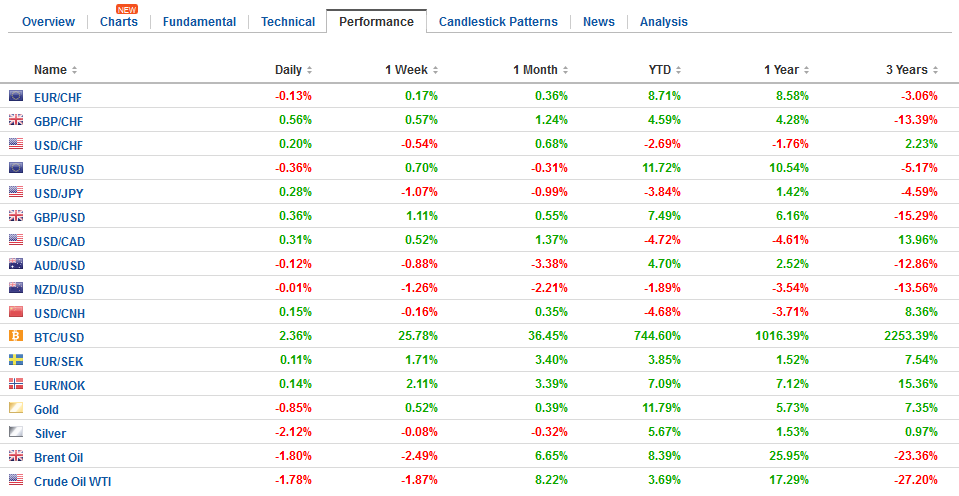

FX Performance, November 20 - Click to enlarge |

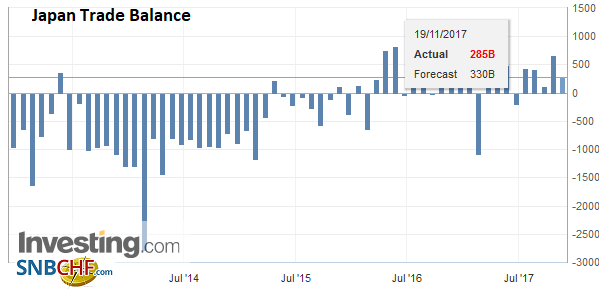

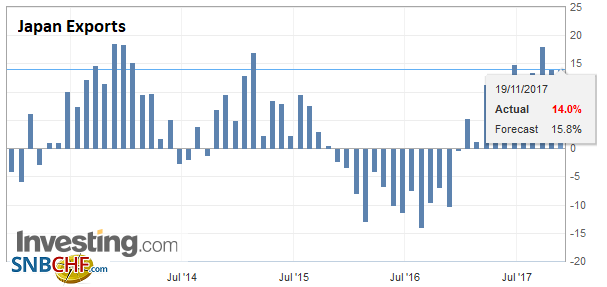

JapanJapan reported a smaller than expected October trade surplus (JPY285.4 bln vs. median forecasts for a JPY330 bln surplus). Exports were a tad weaker, but at 14.0% year-over-year, they are hardly weak. |

Japan Trade Balance, Oct 2017(see more posts on Japan Trade Balance, ) Source: Investing.com - Click to enlarge |

| In fact, October is the fourth month of double-digit year-over-year gains-a streak not seen since before the financial crisis. Exports to Japan’s main trading partners are up across the board. |

Japan Exports YoY, Oct 2017(see more posts on Japan Exports, ) Source: Investing.com - Click to enlarge |

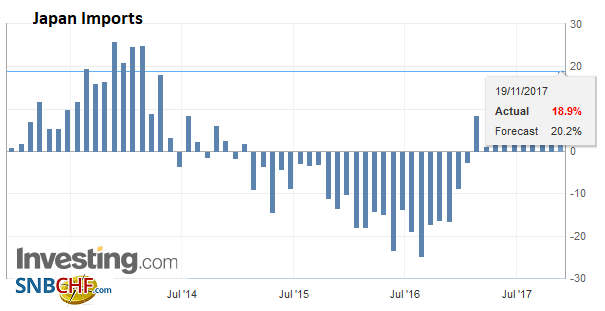

| Exports to the US are up 7.1% compared with 26% to China and nearly 19% to Asia. Exports to the EU were up 15.8%. Although global trade has not reached pre-crisis levels, it has increased notably this year and Asia has played a big role. |

Japan Imports YoY, Oct 2017(see more posts on Japan Imports, ) Source: Investing.com - Click to enlarge |

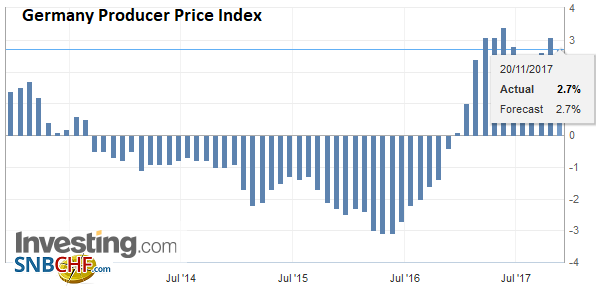

Germany |

Germany Producer Price Index (PPI) YoY, Oct 2017(see more posts on Germany Producer Price Index, ) Source: Investing.com - Click to enlarge |

Reports suggest the UK will boost its initial financial offer of about GBP18 bln. It is only reasonable that the government seeks to minimize the cost to British taxpayers. The EU negotiators, cagey in their own right, appear to have signaled that they are looking for something on the magnitude of three times more. Surely Prime Minister May’s initial offer is not her best or last.

One of the reasons for that the UK appears to be playing its hand poorly is that the government itself is weak and divided. The referendum that was billed as non-binding, which has set the dramatic forces in motion, was decided by a narrow 52-48 majority. Reports indicate that there may be 40 Tory MPs that are willing to sign a letter of no-confidence. Eight more are needed to allow a leadership challenge. Given even a cursory review, the EU must realize that it is more likely the most likely successor to May would be from a wing of the party that would probably be even less compromising.

In the UK, there does not seem to be an agreed upon backup plan to the pie-in-the-sky campaign rhetoric. Maintaining or improving the current trade relation and access to the common market, while being free to make other trade agreements and opt-out of the immigration and labor mobility is untenable.

Speculators in the futures market have returned to a small net short position after a small net long position was seen briefly for a few weeks in September and October. However, the speculative gross short sterling position (~57.7k futures contracts) is the smallest in nearly two years. The gross long speculative position (53.1k contracts) is essentially the 52-week average (52.1k).

Since the middle of September, the correlation of the spot sterling and three-month vol on a purely directional basis turned positive on both a 30-day and 60-day rolling basis. This may be signaling that the market is less prepared for an upside than a downside surprise, while the speculative positioning in the futures market has the bears cautious. Sterling is trying to establish a foothold above its 50-day moving average (~$1.3260), and the top end of its two-month range is seen near $1.3340.

Chancellor the the Exchequer Hammond delivers the Autumn budget on Wednesday. His political future could very well be at stake. Hammond was forced to backtrack from the spring budget initiative to raise the health tax on self-employed people. There has been speculation over the past couple of weeks that May is considering a cabinet reshuffle, and Hammond is one of the ministers thought to be a candidate for being replaced. The hard Brexit ministers are believed to have targeted Hammond.

The ECB will publish the record of its recent meeting this week. At meeting, the ECB expanded its asset purchases through September 2018 at half the current pace. It specifically did not give a firm end date of its operations. However, in recent days, there has been a backdoor effort to offer September as an end date. Some observers underscored ECB’s Mersch suggestion that a fresh program after September was unlikely. We do not think Mersch intended to rule out the possibility of a gradual tapering from the 30 bln euro pace into the end of 2018. He was simply underscoring the fact that the asset purchases are winding down, and a new program, as the Fed did twice, is not needed.

The same difference between the material impact of the actual buying and the signaling effect that we think is the key to understanding Fed policy is also evident at the ECB. In a speech before the weekend, Draghi emphasized the importance of the “signaling effect of asset purchases” over the “duration effect.” It seems to us that this is a key issue and maybe more important divide among central bankers and investors which hawks and doves may less meaningful in present circumstances.

We continue to place an emphasis on the 10-year US yield as a key to the dollar-yen exchange rate. Some have asked about the correlation with equities. Here is what our work has found. Conducting the correlations on the basis of percent change for the past sixty sessions, the dollar-yen and 10-year yields the most correlated at 0.76. The correlation between the dollar-yen and Japanese equities (Nikkei and Topix) is less than a third at 0.31-0.33. The correlation between the dollar-yen and the S&P 500 is higher at 0.55.

The dollar slipped briefly below JPY112.00 in early Asia, partly as the euro-yen cross broke below a neckline of a topping pattern (near JPY131.40). However, the dollar stabilized in a narrow range, meeting offers near JPY112.20. Resistance in the North American session is seen in the JPY112.40-JPY112.60 range.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$EUR,$JPY,$TLT,EUR/CHF,Featured,Germany Producer Price Index,Japan Exports,Japan Imports,Japan Trade Balance,newsletter,USD/CHF