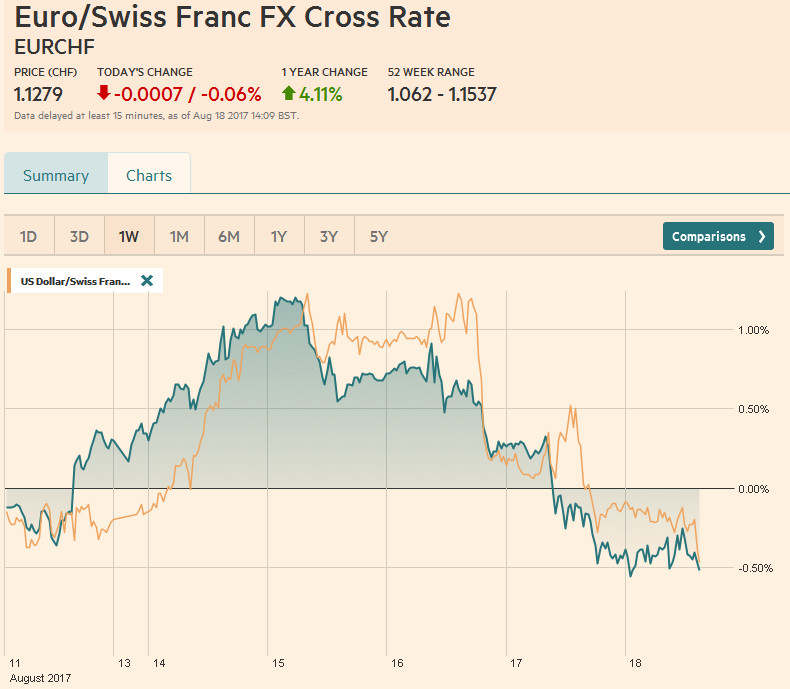

Swiss Franc The Euro has fallen by 0.06% to 1.1279 CHF. EUR/CHF and USD/CHF, August 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates The second largest drop in US equities this year has spilled over to drag global markets lower. The MSCI Asia Pacific Index fell nearly 0.5%, snapping a four-day advance and cutting this week’s gain in half. The Dow Jones Stoxx did not completely escape the US carnage yesterday, but losses are accelerating today, with a nearly 1% decline following a 0.6% decline yesterday. Despite the better than expected retail sales figures earlier in the week, US yields have fallen this week. The 10-year yield is back below 2.20%, off four basis

Topics:

Marc Chandler considers the following as important: Canada, Canada consumer price index, Dow Jones Stoxx, EUR, EUR/CHF, Eurozone Current Account, Featured, FX Trends, Germany Producer Price Index, JPY, newsletter, SPY, TLT, U.S. Michigan Consumer Sentiment, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.06% to 1.1279 CHF. |

EUR/CHF and USD/CHF, August 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe second largest drop in US equities this year has spilled over to drag global markets lower. The MSCI Asia Pacific Index fell nearly 0.5%, snapping a four-day advance and cutting this week’s gain in half. The Dow Jones Stoxx did not completely escape the US carnage yesterday, but losses are accelerating today, with a nearly 1% decline following a 0.6% decline yesterday. Despite the better than expected retail sales figures earlier in the week, US yields have fallen this week. The 10-year yield is back below 2.20%, off four basis points. Today’s yield two-three basis points decline in European bonds leaves most bond markets (except Spain) little changed on the week. |

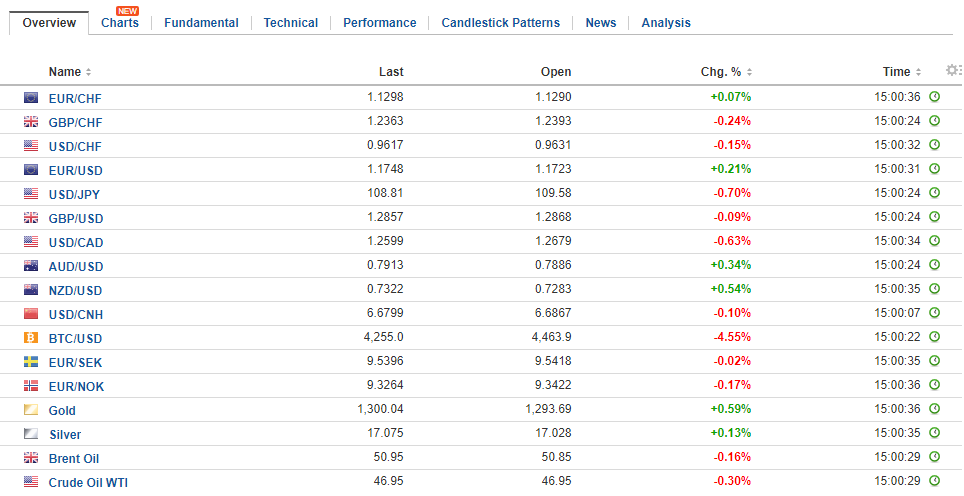

FX Daily Rates, August 18 - Click to enlarge |

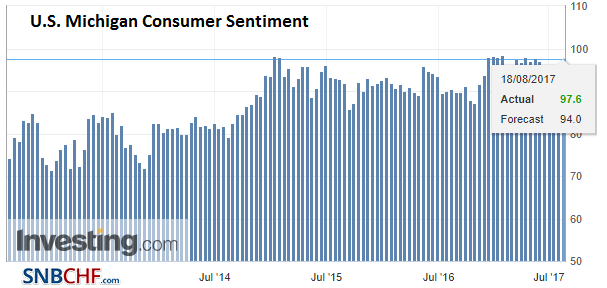

| The news stream is light and activity is winding down for the weekend. The North American session features the University of Michigan’s consumer sentiment survey and inflation expectations. It will be the preliminary August reading. Unless there is a large move in sentiment survey, the most important part of the report is the long-term inflation expectations. Recall that the 5-10 year expectation finished 2016 at 2.3%. After it rose to 2.6% in January, it eased and as recently as May was at 2.4%. However, it rose in June and July to return to 2.6%. It has not been above it since March 2016.

The euro is trading within yesterday’s widest range in nearly two weeks. The euro has spent most of the week below the 20-day moving average (~$1.1760) since the second half of June. A series of lower highs creates a down trend line that comes in today a little above $1.18, and $1.1760 in a week’s time.After reaching almost JPY111 in the middle of the week, the combination of developments saw it briefly slip below JPY109.00. A week ago, the greenback made a low nearer JPY108.75. Our work continues to show a strong correlation between the change in US interest rates and changes in the dollar-yen exchange rate. |

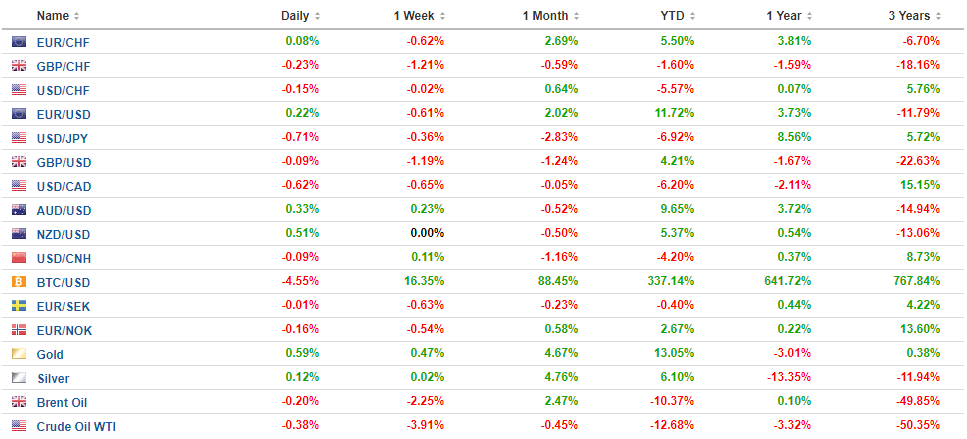

FX Performance, August 18 - Click to enlarge |

United StatesThe US political tension escalated importantly this week that is potentially important for investors. Up until now, it seemed that the leadership of the large US companies were willing to work with the new president, despite his unorthodox ways. The economic agenda, tax reform, deregulation, and infrastructure initiative had much to commend itself to them. However, what has happened in recent days, is that the national bourgeoisie wing of the coalition has begun defecting. That part of the reason that rumors of NEC Director Cohn stepping down elicited such a strong market response. Confidence that Trump’s economic agenda will be implemented has waned in recent months, as the health care reform floundered, and one drama or another distracted. We did not emphasize Trump’s declining support as a market factor because his base held. There are signs of it cracking. Heightened policy uncertainty may not be conducive to the investment climate and the same moment the Fed raises the decibel of its warning about asset prices. A combination of the terrorist strike in Spain and developments in Washington are cited as the major drivers of the slide in US equities, which was seen in the consensus view as a trigger to the dollar and drop in yields. Such explanations are surely part of it, but we would also underscore the importance of what the Fed said in the minutes. We cited it yesterday, but think is so important, we repeat it today: “vulnerabilities associated with asset valuation pressures edged up from notable to elevated.” The Fed upgraded its concern about asset prices (read stock market and long-term bonds). The following the day the stock market sells off and yet few draw a connection. |

U.S. Michigan Consumer Sentiment, Aug 2017(see more posts on U.S. Michigan Consumer Sentiment, ) Source: Investing.com - Click to enlarge |

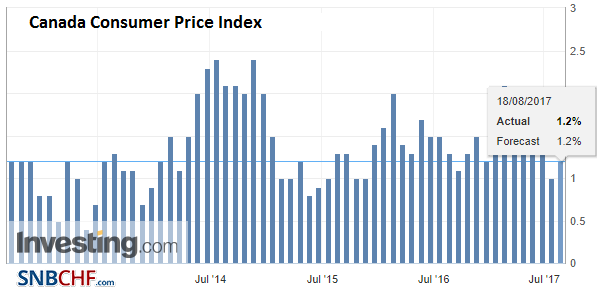

CanadaCanada reports its July CPI data today. Headline inflation, which has fallen from 2.1% in January to 1.0% in June, is expected to rise for the first time this year (to 1.2%). The underlying measures run a little higher than the headline. Extrapolating from the OIS, market expectations for an October hike (there is a Bank of Canada meeting on September 6, but that is not the focus given the July rate hike) have been very stable around 50% over the past month. Investors may be more sensitive to a weaker rather than a stronger report. |

Canada Consumer Price Index (CPI) YoY, Jul 2017(see more posts on Canada Consumer Price Index, ) Source: Investing.com - Click to enlarge |

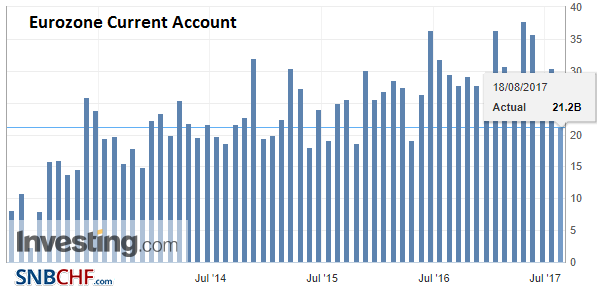

Eurozone |

Eurozone Current Account, Jun 2017(see more posts on Eurozone Current Account, ) Source: Investing.com - Click to enlarge |

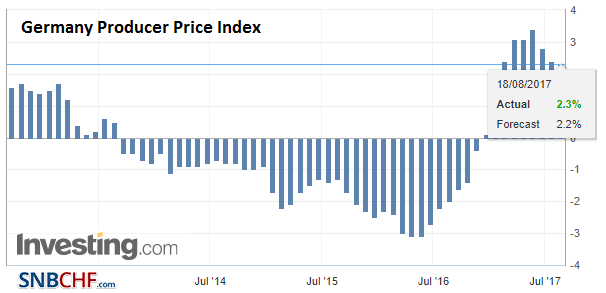

Germany |

Germany Producer Price Index (PPI) YoY, Jul 2017(see more posts on Germany Producer Price Index, ) Source: Investing.com - Click to enlarge |

We note two emerging market developments. First, Taiwan upgraded it economic outlook for this year and next. The anticipation of stronger exports was key. This is not just about Taiwan. Global trade appears to be improving after being sluggish post-crisis. While many economists understand how trade can increase growth, it has become clearer that stronger growth also facilitates trade. Second, China’s Shanghai Composite posted its biggest advance (~1.9%) in four months, though was little changed today. Separately, China announced it would restrict domestic companies from investing in real estate, hotels, entertainment and sports clubs. Overseas investing in gambling will also be banned.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,$EUR,$JPY,$TLT,Canada,Canada Consumer Price Index,Dow Jones Stoxx,EUR/CHF,Eurozone Current Account,Featured,Germany Producer Price Index,newsletter,SPY,U.S. Michigan Consumer Sentiment,USD/CHF