A certain meme has become popular among advocates of both gold and cryptocurrencies. This is the “Fix the money, fix the world” meme. This slogan is based on the idea that by switching to some commodity money—be it crypto or metal—and abandoning fiat currency, the world will improve greatly. Taken in its moderate form, of course, this slogan is indisputably correct. State-controlled money is immoral, dangerous, and impoverishing. It paves the way for government theft of private wealth through the inflation tax, and thus allows the state to do more of what it does best: wage wars, kill, imprison, steal, and enrich the friends of the regime at the expense of everyone else. Privatizing the monetary system and imposing a “separation of money and state” would help

Topics:

Ryan McMaken considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

A certain meme has become popular among advocates of both gold and cryptocurrencies. This is the “Fix the money, fix the world” meme. This slogan is based on the idea that by switching to some commodity money—be it crypto or metal—and abandoning fiat currency, the world will improve greatly.

A certain meme has become popular among advocates of both gold and cryptocurrencies. This is the “Fix the money, fix the world” meme. This slogan is based on the idea that by switching to some commodity money—be it crypto or metal—and abandoning fiat currency, the world will improve greatly.

Taken in its moderate form, of course, this slogan is indisputably correct. State-controlled money is immoral, dangerous, and impoverishing. It paves the way for government theft of private wealth through the inflation tax, and thus allows the state to do more of what it does best: wage wars, kill, imprison, steal, and enrich the friends of the regime at the expense of everyone else. Privatizing the monetary system and imposing a “separation of money and state” would help limit these activities.

But it’s also important to not overstate the benefits of taking money out of the hands of the state. The temptation to push the “fix the world” idea to utopian levels is often seen among cryptocurrency maximalists, and among some gold promoters as well.

For example, at least one bitcoin enthusiast thinks bitcoin will bring “the end of the nation states.” And in one particularly over-the-top paragraph from another bitcoin promoter, we’re told that cryptocurrency will essentially cure every ill from poverty to corruption to environmental destruction.

The idea that changing to different money will somehow end theft, poverty, or even war is the sort of messianic thinking that would have given old-school Marxists a run for their money.

Yes, we can all agree that if we “improve the money” we also “improve the world.” But removing the state’s money monopoly won’t make states fold up their tents and slink away in the night. (And, needless to say, simply changing the money won’t make bad food or poverty disappear either.)

States existed before states took control of the money. And they’ll exist afterward—unless profound ideological changes take place as well.

States Predate Fiat Money

In a recent essay for mises.org titled “How Governments Seized Control of Money,” I explored the early history of the European state and the long process of how states gradually asserted control over money and the financial system. Significantly, however, we find that state power grew well before states established anything resembling true monopolies over the monetary system—or the power to create fiat money.

That is, states long predate the money monopolies they now enjoy. During the sixteenth and seventeenth centuries—without the benefit of fiat currencies—states created enormous standing armies for the first time. They established mercantilist economies. Many rulers managed to assemble large bureaucracies to serve absolutist states. States were centralized to a degree that had not been seen in Western Europe since the Romans. It was a period of enormous gains in state building for princes and their agents.

Yet these states could not “print money” nor enjoy the benefits of fiat money except in very short-lived and limited cases. Indeed, this period of immense state growth was also a period of “concurrent” and “parallel” currencies during which a wide variety of gold and silver coins—most of them foreign—competed within the borders of a single state. Many efforts by regimes to issue questionable, debased money failed because there were so many alternatives. But this didn’t stop, say, Louis XIV from hammering together a powerful state.

So, when we ask ourselves the question, “Can states survive without fiat currency?” the answer is clearly “All experience points to yes.”

States Can Still Tax without Fiat Money

The existence and health of the state does not depend on fiat money or monetary inflation. Those things help a state, to be sure, but they’re not critical to the equation. Rather, what really matters is the ability to use the state’s monopoly on the means of coercion to seize resources.

The great historian of the state Charles Tilly has noted that “no state lasts long” without the ability to engage in “extraction” or “drawing from its subject population the means of statemaking, warmaking, and protection.”1

“Extraction,” of course, will to most modern readers mean simply “taxation.” But historically it can mean other things as well. States can extract resources by demanding tribute as a payment for the “protection” services a state allegedly provides. This might be payment made by a local government to the central government. States also often own large amounts of land and other property. This means states can extract resources directly through rents, leases, and fees. States also can grant monopolies to nominally “private” organizations which provide both tangible and intangible benefits to the state (this is a common tactic under systems like mercantilism). None of this requires fiat money or a monopoly of the production of money. This all simply requires that states have the coercive force necessary to collect taxes, rents, tribute, and other benefits.

Some advocates of cryptocurrencies have nonetheless attempted to claim that when the financial system is decentralized through crypto networks states will somehow be unable to tax. This would work if resources took no form other than money. But that’s not the case. Since human beings are physical beings—with needs for food, water, shelter, heating, and more—the state need only concentrate on taxing and monitoring physical goods. This would certainly shift the tax burden from the financial sector to physical assets, but it wouldn’t end the ability to tax.

Rather, if states find themselves with less access to the monetized economy, states will instead increase taxes on real estate, retail trade, fuel, and hard-to-move physical capital. These states could even require that these payments be made in the state’s preferred money, thus ensuring the continuation of state-controlled money, even if that money is a less preferred money within a competitive framework. Those who refuse to comply would see their assets confiscated at the point of a state-wielded gun.

War Making: The Key Piece of the Puzzle

Finally, we must remember why states need to extract all these resources to begin with. One reason, of course, is that resource extraction begets more resource extraction. Once a state has an army of tax collectors and regulators, it’s easier to expand resource extraction even more. Fortunately—from the state’s perspective—this requires only a fraction of total revenues. Moreover, many taxpayers can be counted on to enthusiastically comply.

An enormous portion of that revenue—virtually all of it in the days before the modern welfare state—has traditionally gone to what Tilly calls a “state’s essential minimum activities.” These are

statemaking: attacking and checking competitors and challengers within the territory claimed by the state.

warmaking: attacking rivals outside the territory already claimed by the state;

protection: attacking and checking rivals of the rulers’ principal allies, whether inside or outside the state’s claimed territory.

These activities are the “core competencies” of states, and these activities also constitute—as Rothbard noted—the most high-stakes activities for states. They are high stakes because states that fail to succeed in these activities are generally doomed states. Thus, even if states are forced to scale back their welfare states, they will fight tooth and nail before giving up any of these “minimum activities.“

Historically, of course, states have been able to obtain more than enough when it comes to resource extraction for purposes of war making and ensuring the protection of the their coercive powers. A monopoly over money and fiat currency was never essential to this equation. States have proven to be quite ingenious when it comes to borrowing, threatening, and propagandizing when necessary to carry out wars—whether against foreigners or against a state’s own people.

Ideologically, of course, the origins of the state lie largely in the ability of state agents to promise “protection” from both foreign and domestic threats. And so long as the general public believes the state is necessary in this equation, states will continue to be able to demand tax revenues, obedience, and “unity.” If anyone doubts that such ideas are alive and well, one need only speak in favor of splitting the United States into smaller pieces. One is likely to immediately hear about how this must never be allowed to happen because China (or some other bogeyman of the day) poses too grave a threat to American “national interests.” A “strong America” is necessary, we’re told. This “strength,” of course, is funded by taxes.

The ideological grip states have over the public in this regard is extremely strong. Unless ideologies change in a big way, most people in the world are likely to continue to look to states to offer protection from various perceived evils. Consequently, separating the state from money won’t fundamentally change the world of geopolitics. It won’t change the fact that many states are immensely popular and regarded by the subject population as important and beneficial. Moreover, age-old sources of conflict will remain. Ethnic tensions will endure. Nationalism won’t disappear. Border disputes and fights over who “rightfully” controls some strategic strip of coastline won’t go away.

Yes, taking the control of money out of the hands of politicians and bureaucrats is clearly a good thing, and ought to be done quickly and thoroughly. But it won’t “fix the world.” It’s only a piece of a much larger puzzle.

- 1. Charles Tilly, Coercion, Capital, and European States, AD 990–1992 (Malden, MA: Blackwell, 1992), p. 96.

You Might Also Like

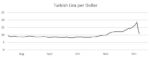

Turkey’s Economy Is in Big Trouble

Turkey’s Economy Is in Big Trouble

2022-01-08

Over the years observers of Turkish politics have become somewhat inured to erratic swings in policy coming out of Ankara. Particularly since the political reforms of 2017, his high degree of control over the primary functions of the state mean President Recep Tayyip Erdoğan faces few hurdles to executing abrupt changes he views as correct or necessary. This lack of any effective institutional check to his authority is, at present, leading the country off an economic cliff.

Markus Krall & Thorsten Polleit – Macht man Gesetze nur für die Reichen?

Markus Krall & Thorsten Polleit – Macht man Gesetze nur für die Reichen?

2021-12-05

Dr. Markus Krall & Prof. Thorsten Polleit im Gespräch: Werden die Gesetze für das Volk oder nur für die Reichen gemacht? Und welche Einflüsse haben unsere Gesetze auf die wirtschaftliche Entwicklung unseres Landes?

The Bank of Canada’s Failed Mission to “Preserve the Value of Money”

The Bank of Canada’s Failed Mission to “Preserve the Value of Money”

2021-12-03

In Canada, inflation hit 4.7 percent in October, and is expected to go even higher. According to a recent survey, 46 percent of Canadians are struggling to feed their families because of the rising cost of living. Perhaps they are also struggling to understand the logic of the Bank of Canada’s (BOC) mission statement: “We work to preserve the value of money by keeping inflation low and stable.”

Is Self-Ownership Necessary?

Is Self-Ownership Necessary?

2021-09-22

Isn’t a principle of nonaggression against others another way of stating the self-ownership principle? "Not necessarily," says the insightful philosopher Chandran Kukathas.

What They Really Mean When They Say “Do the Right Thing”

What They Really Mean When They Say “Do the Right Thing”

2021-09-19

As a senior in high school, I ran for class president with “Do the right thing” as my campaign slogan. Though I realized years ago how utterly pretentious that message is, I’m often reminded that it’s good politics, which proves the point that politics is poison.

Mark Spitznagel Teaches the Economists How to Invest

Mark Spitznagel Teaches the Economists How to Invest

2021-09-16

Bob reviews Mark Spitznagel’s latest book, Safe Haven: Investing for Financial Storms, on which he was a consultant. Bob explains that Spitznagel rejects the alleged dichotomy between risk and return, and then gives a numerical example to illustrate the two schools of thought.

Inflation’s Assault on the Family

Inflation’s Assault on the Family

2021-08-15

I moved aside and watched our twelve-year-old van pull into the driveway. My wife opened the door, smiled, and told me she got the job. Putting the basketball down, I hugged her and told her I was proud. The job was a part-time evening and weekend position at the local country health food store, a good fit considering my wife’s interests. But deep down, a sense of sadness and partial defeat rolled over me.

The Case Against the New “Secular Stagnation Hypothesis”

The Case Against the New “Secular Stagnation Hypothesis”

2021-08-14

Abstract: The new “secular stagnation hypothesis” developed by Lawrence H. Summers attempts to justify why the demand stimulus applied in the aftermath of the global financial crisis failed to revive growth in a satisfactory manner.

Tags: Featured,newsletter