Government-mandated money in the form of legal tender is a historical anomaly. For much of mankind’s history private monies and quasi monies competed alongside each other. Now, again, a new era of private money competition is resurging and reshaping our world. Money, finance, and banking are currently experiencing the “Great Unbundling.” Value chains within finance are being broken up across the spectrum. Customers or users are no longer obtaining their money services as an all-in-one package from a single universal bank but increasingly follow a best-in-class approach in which the best offers from many different providers are chosen. This trend of the fragmentation of financial services has also been recognized by the tech giants of our time. Amazon, Apple,

Topics:

Pascal Hügli considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Government-mandated money in the form of legal tender is a historical anomaly. For much of mankind’s history private monies and quasi monies competed alongside each other. Now, again, a new era of private money competition is resurging and reshaping our world.

Government-mandated money in the form of legal tender is a historical anomaly. For much of mankind’s history private monies and quasi monies competed alongside each other. Now, again, a new era of private money competition is resurging and reshaping our world.

Money, finance, and banking are currently experiencing the “Great Unbundling.” Value chains within finance are being broken up across the spectrum. Customers or users are no longer obtaining their money services as an all-in-one package from a single universal bank but increasingly follow a best-in-class approach in which the best offers from many different providers are chosen.

This trend of the fragmentation of financial services has also been recognized by the tech giants of our time. Amazon, Apple, Google, and Facebook are all pushing into the financial sector. Amazon, for example, already offers loans and other financial services in some countries. Apple and Google Pay are already part of our everyday lives through iOS and Android devices. Facebook recently launched its payment system, Facebook Pay. WhatsApp’s payment system was already active in Brazil when it was halted by the Brazilian central bank (the service is bound to relaunch soon).

Facebook’s Libra Money Scheme Never Went Away

As far as the largest social network in the world is concerned, the goals have been set even higher. In mid-2019, the tech giant announced its intention to launch the digital currency libra, which would be based on a consortium of several members. Soon after this announcement regulators and politicians all around the world began speaking up against this endeavor. Their fear: libra would be an ideal vehicle for money laundering and tax evasion that could potentially destabilize today’s financial order.

After a lot of headwind, the people behind the project not only rebranded libra but came up with version 2.0, called Diem. Not only was the conglomerate consisting of twenty-seven members, with Facebook as one associate, renamed the Diem Association, the project has also changed its structure and goals significantly. While with the first design proposal much of the emphasis was on the libra stablecoin, Diem is designed to become a generic platform for digital programmable currencies. As such, a digital dollar, euro, or pound (e.g., ≋USD, ≋EUR, or ≋GBP) is supposed to be running on Diem’s infrastructure. These digital versions would each be backed by a reserve of assets made up of cash or cash equivalents and very short-term government securities (essentially government bonds) in the respective national currency.

At the same time, a Diem coin (≋XDX), a price-stable multicurrency coin, is to be supported on the Diem payment system. Being a multicurrency stablecoin, the diem coin will be backed by a basket of the several single-currency stablecoins available on the Diem network. Thus, Diem will not rely solely on one national currency, but will be composed of a handful of different government currencies. The concept is similar to the Special Drawing Rights of the International Monetary Fund. Incorporating these national currencies into the Diem system can be interpreted as a step to win the favor of critics in the Western hemisphere.

Can Diem Compete with Government Fiat Monies?

After all, Diem is faced with a dilemma. Its founders envision the diem coin as an efficient cross-border settlement coin as well as a neutral, low-volatility option for people and businesses in countries that do not have a single-currency stablecoin on the network yet. This means that Diem will mainly be to the advantage of developing nations. In order to launch this project, though, the approval and favor of developed countries is needed.

What politicians initially disliked about libra: the possible launch of a new private money by a large private company. Ultimately, this was seen as an attack on today’s sacred cow among politicians, economists, and technocrats: the state’s monopoly of money.

Now that Diem’s major focus is no longer a new global currency existing on its own, but a global payment system and a global financial infrastructure that is based on digital versions of today’s dominant national currencies, critics might change their view. The setup as it stands now would certainly be to the benefit of the US and other governments, as Diem’s coin would serve as a major demander of their securities. In a sense, Diem could ironically also turn out to be fiat’s last chance to keep its relevancy or at least would be a great geopolitical secret weapon against the digital currency initiatives initiated and eagerly pursued by the Chinese.

The Diem a.k.a. libra story shows one thing all too clearly: challenging the state’s monopoly over money is no easy task. Hardly any initiative is met with greater resistance, as officials as well as economists know the sort of power they have by controlling money and its issuance.

Friedrich A. Hayek knew and articulated this well: “I don’t believe we shall ever have a good money again before we take the thing out of the hands of government, that is, we can’t take them violently out of the hands of government, all we can do is by some sly roundabout way introduce something that they can’t stop.”

Notwithstanding libra/Diem, a new monetary era has been initiated by a potential new form of money called bitcoin. Born at the height of the financial crisis, bitcoin represents the antithesis to the existing financial order. The cryptoasset is an attempt to wrest money as a force influencing the economy, politics, and society from the hands of centrally planned God players. Money should be scarce and decentralized in order to tame the endless appetite of politicians, functionaries, and economic giants. In the eyes of its supporters, bitcoin is a counterreaction to the shameful misuse of fiat money.

In the eyes of bitcoin enthusiasts, the efforts of fintech and Big Tech are not the solution, but part of the system, while the system is the real problem. Whether money is supported by the state and issued by private banks or even corporations, the problem remains the same: it remains in centralized hands and cannot be kept self-sovereign.

Digital payment solutions such as Diem that want to turn current money into fiat money 2.0 are merely “lipstick on a pig,” according to bitcoin aficionados. They will not solve the fundamental problem of monetary socialism that ails our monetary system. Money is still tied to intermediaries, and every payment made is recorded in a central database controlled by a third party. Transactions can be censored at any time if necessary.

A Credible Alternative?

For this reason, a distinction must be made between digital currencies and cryptocurrencies. The latter can be exclusively controlled by individuals using cryptographic methods. So-called cryptographic values can thus be held and used directly by their owners and without intermediaries, similar to bearer instruments or material objects. Instead of being managed by an intermediary, crypto values and cryptoassets are based entirely on a blockchain. This is a distributed database nobody has sole control over. The blockchain is ultimately a computer protocol based on programming code. From a technical point of view, this makes the cryptoassets pure information and mathematics.

Consequently, bitcoin stands for an alternative way of imagining a financial system. Today, our financial system is a conglomerate of abstract constructs such as contracts, promises, and balance sheets. This bears witness to the fact that our economy has been getting ever more abstract. The great philosopher and sociologist George Simmel had already noted this tendency toward ever-greater abstraction in 1900, in his work The Philosophy of Money. It can be assumed that this development will continue in the future. Money in the narrower sense, also known as base money, is likely to recede more and more. Money in the broader sense, i.e., money surrogates such as bank deposits, credit cards, and other credit agreements, is likely to become even more prominent.

This development is driven by the financialization of the past decades, which has led to a stronger fusion of the economic and financial worlds. This amalgamate requires a financial alchemy that is now based on three basic building blocks: institutions, incentives, and human participation. In the existing financial system, the human element predominates. Contracts and promises are framed by institutions, but they are executed and enforced by human hands.

In contrast, bitcoin at the protocol level reduces the human element to an unprecedented extent and gives the other two components more weight. On the one hand, technology and incentives to keep the human element in check are becoming more important due to mathematics, cryptography, and computer science. A financial alchemy as we know it today, but one based on bitcoin, is likely to depend less on the human element and more on computers, formulas, and code to control, execute, and enforce it.

What kind of financial alchemy is better in an objective sense cannot be determined at this point in time. This is for the future to decide. As with the discovery of bitcoin, the decision will be made between different types of money that are in direct competition. There’s a traditional world that will be upgraded and take the form of CBDCs (central bank digital currencies) and tokenized assets still based on fiat state money. And there is a more decentralized new world that is being developed, dominated by more private versions of money in the form of bitcoin, ether, and other cryptoassets that will host tokenized assets (such as gold) as well.

You Might Also Like

Trump’s Payroll Tax Order Is Good Politics, but Doesn’t Offer Much Tax Relief

Trump’s Payroll Tax Order Is Good Politics, but Doesn’t Offer Much Tax Relief

2020-08-15

President Trump issued a new executive order on August 8 directing the Treasury Department to defer the 6.2 percent Social Security tax on wages for employees making less than about $100,000 a year. The suspension on collections will be in effect from September 1 through December 31.

MMT Follow-up: A Framework for Money, Inflation, and Debt

MMT Follow-up: A Framework for Money, Inflation, and Debt

2020-08-19

As a follow-up to his discussion on MMT with Rohan Grey (in ep. 130), Bob goes solo to explain the basic cash balance framework for thinking about money, inflation, and debt. Specifically, Bob will explain why he thinks it’s far more important to know how the government finances a deficit rather than knowing what it spends the money on.

Calculating GDP Correctly

Calculating GDP Correctly

2020-08-21

There are many reasons we should be skeptical of the GDP statistic. But it is nonetheless important to understand how it is calculated.

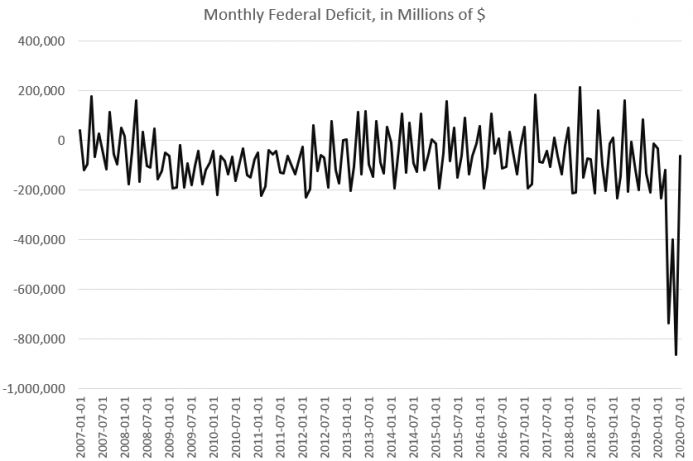

2020 Will Be a Record-Breaking Year for Debt. How Long Can This Last?

2020 Will Be a Record-Breaking Year for Debt. How Long Can This Last?

2020-08-27

The deficit narrowed during July after months of record shortfalls in federal tax revenues. During April, May, and June of this year deficits surges to unprecedented highs as economic activity dried up, workers were furloughed and laid off, and tax payments were deferred.

Why Americans Are Looking for a Safe Haven from the Dollar

Why Americans Are Looking for a Safe Haven from the Dollar

2020-08-30

As the Federal Reserve’s quantitative easing practices generate the biggest debt bubble in history, gold futures are trading at record highs, a phenomenon some have called "a bit of a mystery." However, this "mystery" was solved long ago by the laws of economics.

The Failures of Federal Race-Based Paternalism

The Failures of Federal Race-Based Paternalism

2020-09-07

In an address to the Massachusetts Anti-Slavery Society in 1865, Frederick Douglass noted that he had often been asked “What should we do with the Negro?”

The 2020 Debate: A Breakdown

The 2020 Debate: A Breakdown

2020-10-04

Ryan McMaken and Tho Bishop talk about Tuesday’s debate, why "the issues" don’t matter, and why the debate probably won’t change the minds of many voters.

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-01-25

Update January 25, 2021: SNB buying euros at high prices. Sight Deposits have risen by +0.6 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.6 bn. compared to last week.

Tags: Featured,newsletter