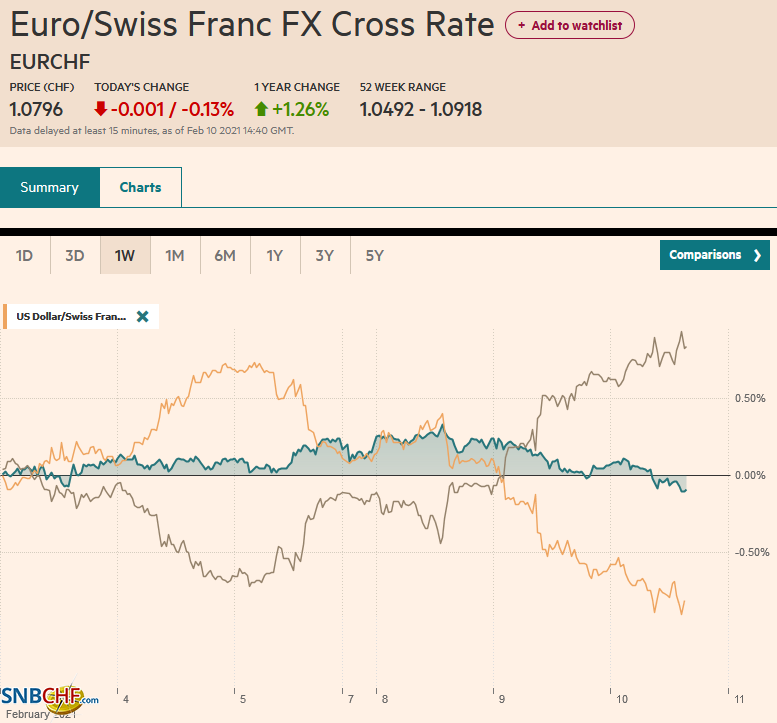

Swiss Franc The Euro has fallen by 0.13% to 1.0796 EUR/CHF and USD/CHF, February 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Despite a soft close in US indices yesterday, global shares are on the march again today. Led by China and Hong Kong, most large markets in the Asia Pacific region advanced today. Officials gave approval for a new game from Tencent, which helped lift the Hang Seng. Europe’s Dow Jones Stoxx 600 slipped fractionally yesterday but has recouped and more today, led by utilities, information technology, and materials. US shares are trading with a firmer bias. Bond markets remain quiet. Ahead of today’s US auction of bln 10-year notes, the benchmark yield is near 1.16%. European

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, Featured, inflation, newsletter, Oil, Olympics, Riksbank, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.13% to 1.0796 |

EUR/CHF and USD/CHF, February 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

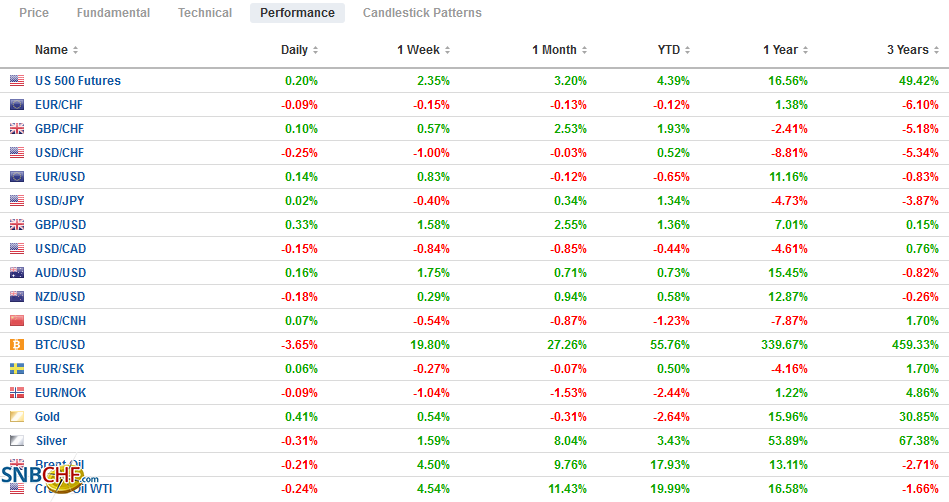

FX RatesOverview: Despite a soft close in US indices yesterday, global shares are on the march again today. Led by China and Hong Kong, most large markets in the Asia Pacific region advanced today. Officials gave approval for a new game from Tencent, which helped lift the Hang Seng. Europe’s Dow Jones Stoxx 600 slipped fractionally yesterday but has recouped and more today, led by utilities, information technology, and materials. US shares are trading with a firmer bias. Bond markets remain quiet. Ahead of today’s US auction of $41 bln 10-year notes, the benchmark yield is near 1.16%. European yields are mostly little changed, with a slight upside bias. The dollar is mixed. The Scandis and sterling are leading the way higher. Sterling is at new highs after punching through $1.38 yesterday. The dollar bloc and yen are softer. Emerging market currencies are also mostly firmer, and China’s yuan is a notable exception as trading winds down ahead of the holiday. The JP Morgan Emerging Market Currency Index is rising for the fourth consecutive session. However, it is oil that is enjoying the longest streak. Today is the eighth session in a row that oil prices are rising, though the upside momentum may be fading. March WTI is near $58.60, after finishing last week a little below $57.00. Gold is firm within yesterday’s range, meeting resistance near $1850. |

FX Performance, February 10 - Click to enlarge |

| Asia Pacific

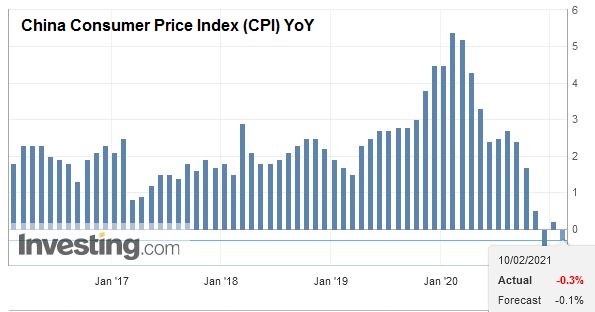

China’s economic recovery is well known, but it has not been accompanied by price pressures. Its headline CPI fell 0.3% year-over-year in January. Core inflation slipped below zero (also -0.3%) for the first time since 2010, dragged down by weak household demand for services. Part of the issue is the base effect. Headline inflation rose 1% on the month in January after a 0.7% gain in December. Food prices rose 1.6% year-over-year, down from a double-digit pace through last summer. |

China Consumer Price Index (CPI) YoY, January 2021(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

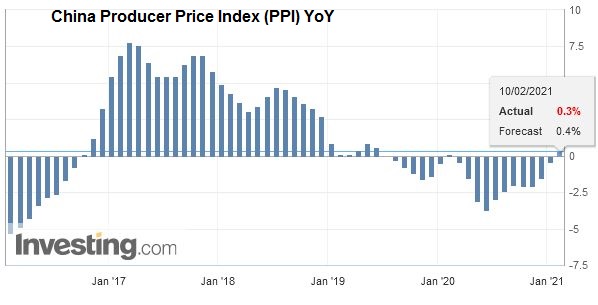

| Pork prices, a key driver of headline inflation, fell 3.9% from a year ago, following a 1.3% decline in December. Separately, rising commodity prices lifted PPI above zero (0.3%) year-over-year for the first time since last January. The soft inflation readings are unlikely to impact PBOC policy but underscore why fears of an imminent tightening are exaggerated. |

China Producer Price Index (PPI) YoY, January 2021(see more posts on China Producer Price Index, ) Source: investing.com - Click to enlarge |

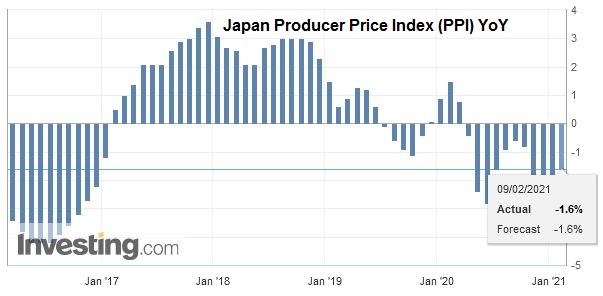

| Rising commodity prices did little for Japan’s PPI. The 0.4% gain in January lifted the year-over-year rate to -1.6% from -2.0%. Meanwhile, Japan’s Summer Olympics remains up in the air. It has been riddled with numerous problems even before the pandemic. Former Prime Minister Mori’s recent comments, insulting women, has produced a new backlash, and the corporate sponsors are complaining, and nearly 400 (of 80,000) volunteers have reportedly resigned. Pressure will mount on Mori to resign, and Prime Minister Suga has not called for his resignation either. Recent polls suggest 80% are opposed to holding the Olympic games on schedule (opening ceremony July 23). The corporate sponsors are planning on meeting ahead of the weekend to take a united stance. The theme of the Olympics ironically is “Unity in Diversity.” |

Japan Producer Price Index (PPI) YoY, January 2021(see more posts on Japan Producer Price Index, ) Source: investing.com - Click to enlarge |

The dollar is recovering from the test on JPY104.40, the lower end of our target (JPY104.40-JPY104.60). Nearby resistance is seen in the JPY104.90-JPY105.10 area. Yesterday’s loss (~0.60%) was the largest so far this year, and a higher dollar close today would be the first in four sessions. The Australian dollar extended its recent gains and poked above $0.7750 before sellers emerged. Support is seen near $0.7700, yesterday’s low, and a close below it would weaken the technical tone, hinting that the upside correction has run its course. The PBOC set the dollar’s reference rate at CNY6.4391, a little higher than the Bloomberg survey of bank models. As the Lunar holiday is about to begin, note the dollar has been confined with a couple of minor exceptions to the range set in the first couple sessions of 2021: roughly CNY6.43 to CNY6.51. Also, the offshore yuan (CNH) has once again risen past the onshore yuan (CNY), and the gap is the widest in a month.

Europe

Sweden’s Riksbank did not surprise. There was no change in policy. It does not expect that inflation will sustainably reach its target until 2023. Officials acknowledged that the changing consumption patterns and changes to the labor market data methodology complicate the economic analysis. Sweden’s economy was among the best performers in Europe last year with a 2.8% contraction. The eurozone’s output appears to have shrunk by more than twice that.

Of the large countries in the euro area, French industrial output was the biggest negative surprise. Ironically, the Bloomberg survey’s median forecast was for a 0.4% gain, which was more than it had expected from Germany, Italy, and Spain. Instead, output fell by 0.8%, and even worse, manufacturing output collapsed by 1.7%, while economists had anticipated a 0.3% decline. Production in Germany, Italy, and Spain was expected to rise by 0.3%. Germany’s was flat, Italy’s fell by 0.2%, and Spain surprised with a 1.1% increase. The aggregate figure is due on February 15, followed by the preliminary Q4 20 GDP the next day.

The euro approached our $1.2150 target in late Asian turnover. We suspect the market may try to retest the highs, though a break of $1.2100 would suggest it has been rejected. The euro has risen for three sessions coming into today after falling in the previous four. A move above $1.2150 brings $1.2200 into view. Sterling is making new highs today, a little above $1.3850. It has held above $1.3800 so far today. Recall that a week ago, sterling had briefly traded below $1.3570. There is little chart resistance ahead of the $1.40 area.

| America

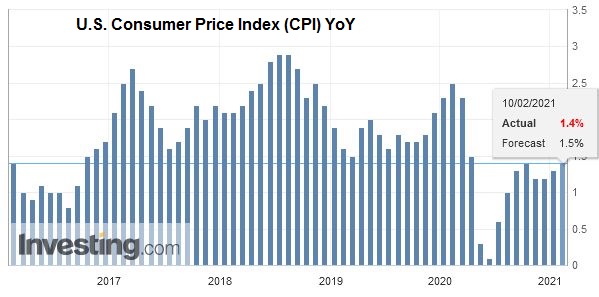

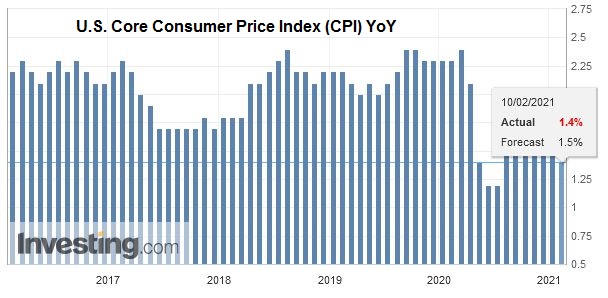

The US reports January CPI today. The headline pace may tick up to 1.5% from 1.4%, while the core rate is expected to slip to 1.5% from 1.6%. It is unremarkable, but the calm is almost over. After February, the spring inflation scare will properly begin. In March 2020, headline CPI fell by 0.3%, in April by 0.7%, and by 0.1% in May. |

U.S. Consumer Price Index (CPI) YoY, January 2021(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| As these negative prints drop out, the base effect will lift the year-over-year rate. The scare will subside in June-August as the CPI in 2020 rose 0.4%-0.5% a month. |

U.S. Core Consumer Price Index (CPI) YoY, January 2021(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

Although Mexico’s January inflation, reported yesterday, was a little firmer than expected at 3.54% (vs. the median forecast in Bloomberg’s survey of 3.45%), Mexico’s central bank is widely expected to deliver a 25 bp rate cut today that will bring the overnight rate to 4.0%. The pandemic has hit Mexico particularly hard, and by some metrics, among the hardest hit in the world. The AMLO government has been reluctant to provide much fiscal support, which puts more weight on monetary policy. Through the power of appointment, AMLO has secured a majority of the Banxico board. While today’s move is one thing, the real issue is the forward guidance about the possibility of another cut. It looks difficult without inflation falling further.

Rising oil and equities support the Canadian dollar, but it typically underperforms in a soft US dollar environment. Yesterday, it gained a little more than a third of a percent. Among the majors, only the New Zealand dollar did worse (+0.25%). The US dollar slipped through support in the CAD1.2680 area today to record its lowest level since January 23. It snapped back above CAD1.27 in late Asia/early Europe turnover and is straddling that area. Initial resistance is seen in the CAD1.2720-CAD1.2740 area. The greenback peaked near MXN20.60 at the end of January. It settled last week slightly below MXN20.09. Yesterday, it recorded its low so far here in February, just above MXN20.01. Resistance is seen in the MXN20.15 area. The rate decision may inject some volatility into the peso trading. It may require a break of MXN19.95 or MXN20.20 to be significant from a technical point of view.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-02-08

Update February 8 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

2021-02-08

Overview: The US dollar has drifted higher against the major currencies and most of the freely accessible emerging market currencies, paring the losses seen before the weekend in response to the disappointing employment report. Easing pressure from the pandemic as the surge in cases after the holidays may also be encouraging risk-taking to extend the global equity rally.

FX Daily, February 4: Negative Rates and the Bank of England: Having Your Cake and Eating it Too

FX Daily, February 4: Negative Rates and the Bank of England: Having Your Cake and Eating it Too

2021-02-04

Overview: The euro has been sold through $1.20 for the first time since December 1 and has now given back roughly half of the gains scored from the US election (~$1.16) to the early January high (~$.1.2350). More broadly, the greenback is bid against most of the major currencies, with the Australian dollar more resilient after reported record iron ore exports and all but a handful of emerging market currencies.

FX Daily, January 25: A Subdued Start to a Big Week

FX Daily, January 25: A Subdued Start to a Big Week

2021-01-25

What promises to be an eventful week has begun off on a mostly subdued note. Asia Pacific equities moved higher, again led by Hong Kong and ostensibly mainland buying. The Hang Seng rose 2.4% to bring this year’s gain to 10.75%. South Korea’s Kospi also increased by more than 2%, and, so far this month, it is up almost 11.7%.

FX Daily, January 6: High Drama Weighs on the Greenback and Lifts Yields

FX Daily, January 6: High Drama Weighs on the Greenback and Lifts Yields

2021-01-06

Overview: One of the two Georgia Senate contests remains too close to call, but the market appears to be pricing in a Democrat sweep. The 10-year yield has punched above 1% but has offered the greenback little support. Yesterday, the dollar-bloc currencies rose to highs since early Q2 2018 and are extending those gains today.

FX Daily, December 17: Dollar Thumped

FX Daily, December 17: Dollar Thumped

2020-12-17

Overview: The prospects of a UK-EU deal and US stimulus continue to underwrite risk appetites and weigh on the dollar. Equity markets are moving higher. Led by Australia and China, the MSCI Asia Pacific Index rose to new record highs, while Dow Jones Stoxx 600 in Europe is at its best level since February.

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

FX Daily, September 15: The Dollar Softens Ahead of the FOMC

2020-09-15

The capital markets are relatively quiet so far today as the FOMC meeting gets underway. Equity markets in the Asia Pacific region, but Japan and Australia advanced, and the regional benchmark rose for the fourth consecutive session. European stocks are a little firmer.

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

FX Daily, August 26: Hurricane Laura Lifts Oil Prices

2020-08-26

A consolidative tone has emerged after US equity benchmarks reached new highs yesterday. The MSCI Asia Pacific Index had reached seven-month highs on Tuesday, but Japan, China, and Australian stocks saw modest profit-taking today. European shares are recouping yesterday’s minor loss, and US shares are flat.

Tags: #USD,China,Currency Movement,Featured,inflation,newsletter,OIL,Olympics,Riksbank