(Disclosure: Some of the links below may be affiliate links) If you want to invest in the stock market, you will need to choose a portfolio. Ideally, you will want to invest in index funds via Exchange Traded Funds (ETFs). For, this you will need to decide on an ETF Portfolio for Switzerland. Choosing a good portfolio is an important decision. You need to invest in a portfolio that will have low fees, high diversification, and good returns. And you should be careful about keeping it simple! While there are many examples of ETF Portfolios for the United States, they are not so many for Switzerland. So, it is not ideal to decide on. In this article, we are going to go over the details of choosing an ETF Portfolio for Switzerland. And at the end of the article, I

Topics:

Mr. The Poor Swiss considers the following as important: 9) Personal Investment, 9) The Poor Swiss, Featured, Investing, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

(Disclosure: Some of the links below may be affiliate links)

If you want to invest in the stock market, you will need to choose a portfolio. Ideally, you will want to invest in index funds via Exchange Traded Funds (ETFs). For, this you will need to decide on an ETF Portfolio for Switzerland.

Choosing a good portfolio is an important decision. You need to invest in a portfolio that will have low fees, high diversification, and good returns. And you should be careful about keeping it simple!

While there are many examples of ETF Portfolios for the United States, they are not so many for Switzerland. So, it is not ideal to decide on.

In this article, we are going to go over the details of choosing an ETF Portfolio for Switzerland. And at the end of the article, I will give you an example of what I think is the best ETF Portfolio for Switzerland.

Investing involves risks of losses. Make sure you are aware of that before you start investing.

Choosing an ETF Portfolio for Switzerland

Choosing an ETF portfolio is an essential step in investing in the stock market. You should keep the same portfolio for a very long time. So, you need to choose carefully.

If you live in the United States, you will have seen tons of examples of ETF portfolios. But if you live in Switzerland, you probably have not seen that many of them.

And if you live in Switzerland or Europe, you should not blindly follow a portfolio that comes from another country. Switzerland cannot be compared with the United States. Our stock market is 20 times smaller. And in some other countries, it is even smaller than that. So we cannot invest in the same way.

I believe that the best ETF Portfolio for Switzerland has two essential parts:

- It uses an ETF representing the entire world stock market. Or it holds two ETFs, one for the Developed World and one for the Emerging Markets, but not more than two.

- It uses an ETF representing the domestic Swiss stock market. This part of your portfolio is called your home bias.

With these two parts, you can have a very diversified yet very simple portfolio. This portfolio is what I am investing in and what I recommend people to invest in.

We are going to see a few things into detail before I go over the ETFs that form the best ETF portfolios for Switzerland.

Home Bias

A good ETF Portfolio for Switzerland should have some domestic stocks. This allocation will be your home bias.

The main reason for this is related to currency. Since the Swiss Franc is a stable currency, other currencies tend to depreciate against the Swiss Franc. If your entire portfolio is in USD, you may lose a lot of value. So having an ETF in your local currency will help you.

Of course, you could hold only Swiss stocks in Swiss francs, and you will not have this issue. But having only Swiss stocks is not a great idea. A lot of Swiss companies are exporting to other countries. It means their performance is subject to currency exchanges.

And also, the Swiss stock market is tiny, about 2.5% of the world’s stock market. Do you want to bet your entire portfolio on 2.5% of the world?

Finally, the Swiss stock market has lower performance than the world stock market, at least historically. So if you only invest in Swiss stocks, you will need a larger portfolio to sustain your expenses.

Another way of reducing the currency risk is to use ETFs that are hedged to CHF. But currency hedging is expensive and is generally not the best tool for long-term investing.

So, how much should you allocate to your home bias?

I think that between 20% and 40% should be allocated to a Swiss Stocks ETF. 10% is also probably fine, but anything below 10% will not make enough of a difference to bother with it. 50% is also probably okay, but you are making a large bet on the Swiss Stock market with such a large allocation. It is why between 20% and 40% is a reasonable allocation.

In my ETF Portfolio for Switzerland, I have 20% of Swiss Stocks.

I have done simulations of early retirement in Switzerland with Swiss Stocks. If you look at the results, this will also confirm the 20% to 40% basis.

What about bonds?

Unfortunately, Swiss bonds have been in negative territory for a long time now. And given the current situation, I do not believe they will become positive any time soon.

Therefore, I think it is not a good idea to invest in Swiss bonds at this time. You should not add Swiss to your ETF portfolio for Switzerland.

If the situation improves and bonds are back to yielding 1% or more, they may become interesting again.

What about foreign bonds?

Some people try to invest in foreign bonds instead. I do not think this is a good idea. I made this mistake myself. The problem with international bonds is that they will incur an additional currency risk to your portfolio.

When you invest in bonds, you want this to lower the volatility of your portfolio. You want your bonds to help you when the stock market does not do well. But if you add currency risk on top of that, you will not achieve this goal.

So, investing in foreign bonds is a lousy alternative to Swiss bonds for an ETF portfolio for Switzerland.

Alternatives to Swiss Bonds

I think there are several solutions to emulate bonds:

- Allocate some of your Swiss Portfolio to cash. Currently, cash is better than bonds. It is not great since it is still losing value due to inflation. But it still beats Swiss bonds.

- Invest in your second pillar. Most second pillar accounts offer around a 1% interest rate. It is not great, but it is much better than cash. And you will have some tax advantages as well. For me, this is the best alternative to Swiss bonds.

- Invest in gold. Gold has better returns than the second pillar and the Swiss bond market. And there are some excellent Gold ETFs. So you can directly invest in gold in your ETF Portfolio.

Of these three options, I prefer investing in my second pillar. But the second pillar has two limitations. First, it is limited in that you cannot invest a limitless amount into it. Secondly, you will not be able to get the money before you retire. Therefore, it is not ideal for early retirement.

So, I would recommend starting with your second pillar. And then, you can allocate some part of your ETF portfolio for Switzerland into gold.

How to choose ETFs

For each position in your portfolio, there will be several choices for you. There are many ETFs for each stock market index. So, how can you choose between these ETFs?

There are several things you need to look at:

- The Total Expense Ratio (TER) of the fund, this is how much fees you are going to pay each year.

- The domicile of the fund, this is the country from which the ETF comes from.

- The size of the fund. You generally want large funds for smaller spreads and higher liquidity. But do not pay too much attention to the detail. A fund managing two billion dollars is not better than a fund managing a single billion. On the other hand, a fund managing 10 million is less attractive than one managing 200 million.

- The way the ETF is replicating the index. You only want to invest in funds with Physical Replication.

- The way the ETF is handling dividends. A fund can either distribute or accumulate dividends. In Switzerland, you will pay the same taxes for both, so it is mostly a matter of preference. I prefer distributing funds so that I will get the cash once I need it in retirement.

One excellent resource to find and compare ETFs is justetf.com. They have an extensive list of ETFs, and you can compare the information on different ETFs in a very convenient way.

If you want more detail about this process, I have an article about choosing and comparing ETFs.

The best ETF Portfolio for Switzerland

Now, we have covered the most important aspects of designing an ETF portfolio. We can finally go over the details of the ETFs.

Now, keep in mind that this is only an example, and this only reflects my way of investing. This portfolio may not be the best ETF Portfolio for Switzerland for everybody. And remember that I am not a personal advisor and that you should still do your research and not merely copy what I am doing.

Here is what I consider to be the best ETF Portfolio for Switzerland:

- 80% World ETF

- 20% Swiss Stocks ETF

It is extremely simple and highly diversified. As I said, the percentages can vary. Between 20%and 40% to Swiss stocks is a good range. So you could go 25/75 or 60/40, for instance. Anything between 20% and 40% would be fine. Adding more Swiss stocks will reduce your currency risk but reduce your returns.

Now, we can look into the ETFs. Which one you use will depend on whether you have access to U.S. ETF or not.

ETF Portfolio with U.S. ETFs

If you have access to U.S. ETFs, for instance with Interactive Brokers, I recommend the following ETFs:

- Vanguard Total World (VT) for the World ETF with a TER of 0.08%

- iShares Core SPI (CHSPI) for the Swiss Stocks ETF with a TER of 0.10%

With this portfolio, you will have very low fees and high diversification. You also have the advantage of saving 15% of the U.S. dividends on VT. Saving on dividends will make a significant difference compared to the other portfolio. It is some extra optimization that you can do to your portfolio. But in the grand scheme of things, it will not change everything.

As an example, with my allocation of 20% to Swiss Stocks, this would give this ETF Portfolio for Switzerland:

- 80% Vanguard Total World

- 20% iShares Core SPI

This portfolio is the current portfolio I am investing in.

ETF Portfolio without U.S. ETFs

If you do not have access to U.S. ETFs, for instance with DEGIRO, I recommend the following ETFs:

- HSBC MSCI World UCITS ETF for the World ETF with a TER of 0.15%

- iShares MSCI Emerging Markets UCITS ETF with a TER of 0.18%

- iShares Core SPI (CHSPI) for the Swiss Stocks ETF with a TER of 0.10%

Unfortunately, the best European World ETFs do not contain both developed markets and emerging markets. So, we need to use two ETFs. I recommend allocating 10% to emerging markets. With my allocation of 20% Swiss Stocks, this would give:

- 70% HSBC MSCI World

- 10% iShares MSCI Emerging Markets

- 20% iShares Core SPI

This portfolio would be the one I would be using if I were not investing in U.S. ETF.

Now, many people prefer to use Vanguard. If you want, you can also use the Vanguard FTSE All-World UCITS ETF (VWRL) with a TER of 0.22%. It is a really good ETF. And it has the advantage of being in the free list of DEGIRO. So, if you use DEGIRO, you will not pay transaction fees when buying and selling shares of this ETF.

Another advantage of VWRL is that it includes both developed and emerging countries. This means that you do not have to use a second ETF. Simplicity makes a lot of sense for investing, so this may really be worth the small extra fee.

This portfolio has two disadvantages over the one with U.S. ETFs:

- The TER is slightly more expensive.

- You will lose 15% of the U.S. dividends because you will not profit from the tax treaty since the funds are not in the United States. This difference is more significant than the first one. But this difference is often ignored by many investors.

If you can, you should probably invest in U.S. ETFs. But I want to emphasize something that many elitists will not tell you: Investing in a good portfolio is much more important than investing in the perfect portfolio!

If your broker does not give you access to U.S. ETF and you do not want to change, then go ahead and invest with European ETFs!

Conclusion

You should now know what ETFs you should invest in Switzerland. You can now decide on your ETF Portfolio for Switzerland.

The ETF Portfolios from this article are just examples of what I recommend to invest in. This portfolio may not be the best ETF Portfolio for everybody. But you should now know enough so that you can do your research and decide for yourself in which ETF Portfolio you want to invest.

And remember: investing in a good portfolio is more important than investing in the best portfolio. If you take years to decide on the best portfolio and delay investing, you are losing out on some opportunities. It is better to get started with a good portfolio, and you can refine it over the years.

Of course, you will need to have a broker account to invest in your ETF Portfolio. If you do not yet have a broker, I have a guide on choosing the best broker account for Switzerland.

If you want more control over your portfolio, I have a guide on how to create an ETF portfolio from scratch.

What do you think of this ETF Portfolio for Switzerland? How does your portfolio look like?

You Might Also Like

What is the best broker in Switzerland in 2020?

What is the best broker in Switzerland in 2020?

(Disclosure: Some of the links below may be affiliate links) I have talked about several brokers on this blog. But I have not yet answered the question of which one is the best broker in Switzerland!It is now time to answer this important question. There are several Swiss brokers, and most Swiss banks have their broker service. But some international brokers are also available in Switzerland.If you want to invest in the stock market, you will need a broker account.

What does the U.S. Estate Tax mean for Swiss Investors?

What does the U.S. Estate Tax mean for Swiss Investors?

Many people think that investing in the United States Exchanged Traded Funds (ETFs) is dangerous. They believe that because of the U.S. Estate Tax. This tax will heavily tax the assets of a decedent. This tax means that your beneficiary will only get a portion of your estate when you decease. Because of that, many people recommend not to invest in American ETFs (or even stocks).

How to Invest in the 2020 Bear Market

How to Invest in the 2020 Bear Market

We have just reached a new bear market due to the fears of the coronavirus pandemic. The chances are that this is your first bear market. And the chances are that you are freaking out.

April 2020 – A month at home

April 2020 – A month at home

(Disclosure: Some of the links below may be affiliate links) April 2020 is now over! That was one of the weirdest months of our life. We spent the entire month in our village, mostly at home. We only went out to buy groceries and help some of my relatives.Fortunately, we have a large backyard, so we spent a lot of time outside. And Switzerland is not in full lockdown, so we still went out for walks.

6’000 CHF Dividenden im Jahr 2020 ??

6’000 CHF Dividenden im Jahr 2020 ??

6’000 CHF an Dividenden möchte ich im Jahr 2020 netto verdienen. Ob das machbar ist, möchte ich in diesem Beitrag genauer erläutern und analysieren. Im Jahr 2019 hatte ich 3’001.89 CHF an Dividenden netto erhalten, das möchte ich dieses Jahr verdoppeln. Verdopplung der Dividenden möglich?Ist es möglich, die Dividenden im vergleich zum Vorjahr zu verdoppeln? Ich glaube schon, aber nicht allein durch das Dividendenwachstum.

Some Thoughts on Recent Foreign Exchange Intervention

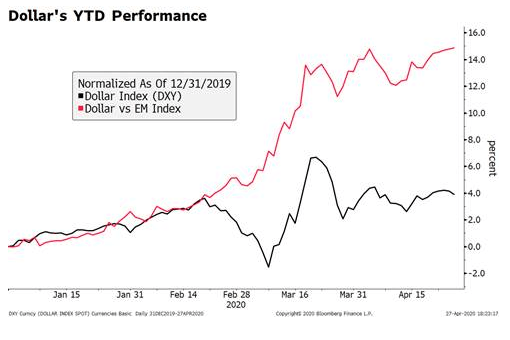

Some Thoughts on Recent Foreign Exchange Intervention

Dollar softness this week will take some pressure off of the foreign currencies but it’s too early to sound the all clear. This piece focuses on how central banks around the world may be intervening to influence their currencies. Most of the world, particularly EM, is grappling with supporting weak currencies but a select few are dealing with stronger currencies. This is a very opaque process and so we are simply making our best guesses.

SNB’s swollen balance-sheet poses risk to ‘credibility’

SNB’s swollen balance-sheet poses risk to ‘credibility’

When the Swiss National Bank (SNB) followed last year’s $50 billion (CHF48.6 billion) profit with a record $39 billion first-quarter loss, it was a stark illustration of the volatility created by a decade of unconventional monetary policy.

The Global Airline Industry Is in Even Worse Shape Than You Think

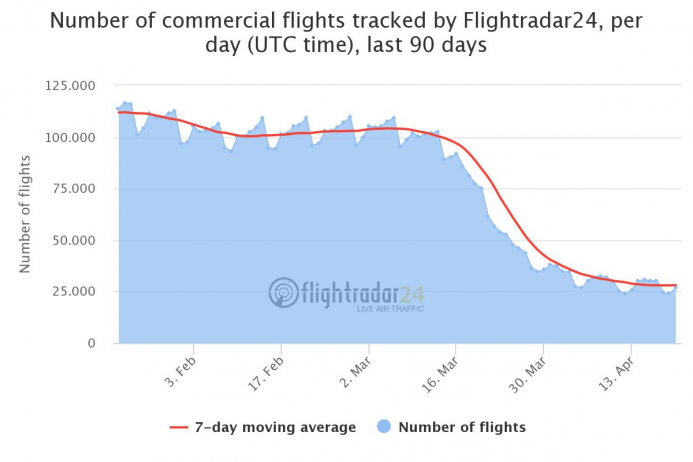

The Global Airline Industry Is in Even Worse Shape Than You Think

The economic impact of the COVID-19 pandemic has reached all productive sectors. The massive spread of the virus and social distancing measures have led to a dramatic decrease in economic activity. The aviation industry, vital for tourism and business, has been hit hard. Investors and analysts state that this crisis could be worse than the one that followed the SARS outbreak in 2003 and the one after 9/11.

Tags: Featured,Investing,newsletter