Over here, on the other side of that ocean, the US economy can only dream of the low levels Chinese industry has been putting up this late into 2020. At least those in the East are back positive year-over-year. Here in America, manufacturing and industry can’t even manage anything like a plus sign. Summer slowdown extends in Industrial Production. According to the Federal Reserve, the outfit which has kept tabs on this economic sector for more than a century, the economic rebound from 2020’s big collapse bent the wrong way around July and hasn’t yet been able to curve its way back in the good direction. US Industrial Production, SA 2011-2020 - Click to enlarge Over the four months since, through November, IP has come back by just a little over 2%. While a 6.7%

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, consumer goods, currencies, economy, employment, Euro$ #4, Featured, Federal Reserve/Monetary Policy, GFC1, GFC2, global dollar shortage, industrial production, industry, manufacturing, Markets, newsletter, private payrolls, Recession

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Over here, on the other side of that ocean, the US economy can only dream of the low levels Chinese industry has been putting up this late into 2020. At least those in the East are back positive year-over-year. Here in America, manufacturing and industry can’t even manage anything like a plus sign.

Summer slowdown extends in Industrial Production. According to the Federal Reserve, the outfit which has kept tabs on this economic sector for more than a century, the economic rebound from 2020’s big collapse bent the wrong way around July and hasn’t yet been able to curve its way back in the good direction. |

US Industrial Production, SA 2011-2020 - Click to enlarge |

| Over the four months since, through November, IP has come back by just a little over 2%.

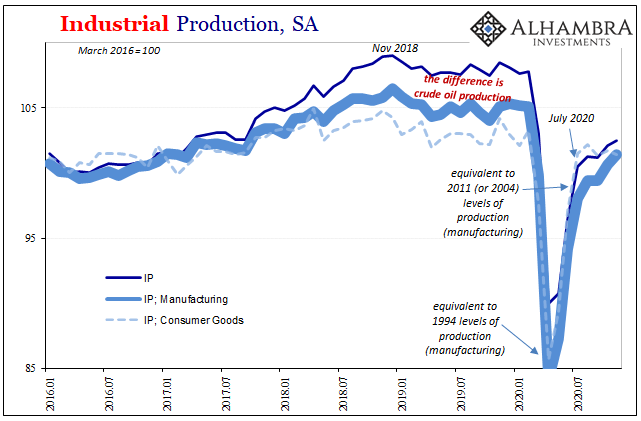

While a 6.7% annual rate sounds fantastic – given where things stood even before COVID – it isn’t near enough to make up for the almost 17% drop March and April. Because of the clear and sustained slowdown, IP in November 2020 remained a very recession-like 5.5% below where it had been in November 2019. And, lest we forget, US industrial output in November 2019 was already a touch (-0.4%) less than it had been in November 2018. Landmines and their (ongoing) aftermath. |

Industrial Production, SA 2016-2020 - Click to enlarge |

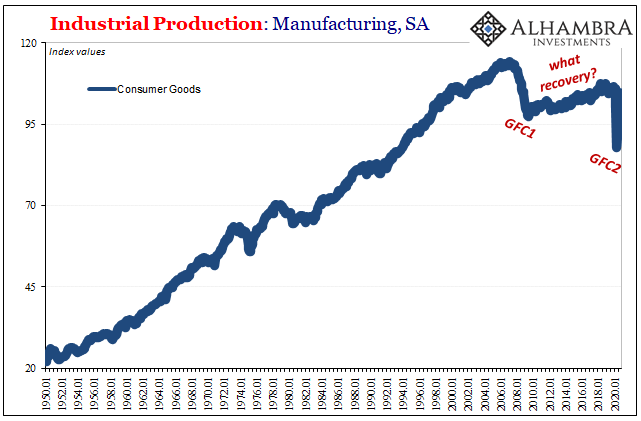

Industrial Production: Manufacturing, SA 1950-2020 - Click to enlarge |

|

| The implications, at least, are very simple and straightforward: as we’ve been saying since summer, the production side of the economy never bought the “V.” Largely because of this, this segment (which includes services; so much of the service sector is dedicated to managing, transporting, and selling what industry makes or extracts) hasn’t been hiring and rehiring near enough to create a recovery. Negative spillovers abounded.

Like the labor market, output isn’t even halfway. And that should boggle the mind given what would have happened if there had been a “V.” Economic activity beginning with industry should’ve not only rebounded to where it was prior in February (or November 2018, if we’re truly keeping score), it would’ve surged way above for at least a few months to make up for those when production was largely closed down. In the immediate aftermath, during the reopening frenzy, that scenario had been somewhat plausible, at least for officials hoping to make the message reasonably saleable to the general public as a way to float as much optimism as humanly possible. |

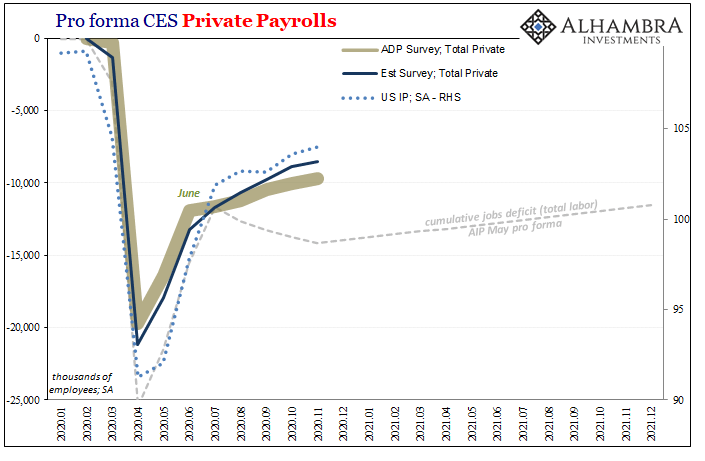

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

| Overall economy activity, including the labor market, came back really quickly in the initial stage (gigantic positives).

That all stopped, though, and for reasons that no one seems to want to venture an explanation. The “V” died and we’re left otherwise to believe that a resurgent COVID bug did the deed. Nope. This thing turned, again, back in July for IP and in June for a lot of data including employment figures (and markets which sniffed it out in real-time). As gigantic as those positives had been, they actually weren’t near enough to convince economic actors (employers, consumers) to take on the risks a true recovery demands. Neither was QE and all those government stipends pretending to be “stimulus.” Of the latter, such aid was legitimate and legitimately necessary given the situation. It wasn’t, however, going to be sufficient to bring about the “V”-shaped recovery. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

Already the economy was put in a horrible position by GFC2; on top of what had been, at minimum, a manufacturing and industrial recession prior to this year which had been ongoing for a very long time (Euro$ #4). I wrote the following on March 26, the title all-too-accurate as it has turned out, if you’ll permit me the extent of the reminder:

Add US industry to the already-lengthy list populated by a broad survey of wide-ranging data showing you that, yes, definitely more slowly, way too slowly, such that sadly fewer of displaced workers really will have their livelihoods restored. Vaccines won’t fix this. Nor is inflation coming out of it. |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

You Might Also Like

Meaning Mexico

Meaning Mexico

2020-08-25

It took some doing, and some time, but Mexico has managed to bring its car production back up to more normal levels. For two months, there had been practically zero automaking in one of the biggest auto-producing nations. Getting back near where things left off, however, isn’t exactly a “V” shaped recovery; it’s only halfway.

A Japanese Stall?

A Japanese Stall?

2020-07-24

In sharp contrast to the sentimental deference towards central bank stimulus exhibited by Germany’s ZEW, for example, similar Japanese surveys are starting to describe potential trouble developing. Like Germany, Japan is a bellwether country and a pretty reliable indicator of global economy performance.

Reality Beckons: Even Bigger Payroll Gains, Much Less Fuss Over Them

Reality Beckons: Even Bigger Payroll Gains, Much Less Fuss Over Them

2020-07-05

What a difference a month makes. The euphoria clearly fading even as the positive numbers grow bigger still. The era of gigantic pluses is only reaching its prime, which might seem a touch pessimistic given the context. In terms of employment and the labor market, reaction to the Current Employment Situation (CES) report seems to indicate widespread recognition of this situation. And that means how there are actually two labor markets at the moment.

Of Incomplete Plans and Recoveries

Of Incomplete Plans and Recoveries

2020-07-21

At the monthly press conference China’s National Bureau of Statistics (NBS) now regularly gives whenever the Big Three economic accounts are updated (this time along with quarterly GDP), spokesman Liu Aihua was asked by a reporter from Reuters to comment on how the global economic recession might impact the Communist government’s long range goal of reaching its assigned GDP target.

It Was Bad In The Other Sense, So Now What?

It Was Bad In The Other Sense, So Now What?

2020-08-18

According to the latest figures, Japan has tallied 56,074 total coronavirus cases since the outbreak began, leading to the death of an estimated 1,103 Japanese citizens. Out of a total population north of 125 million, it’s hugely incongruous.

Part 2 of June TIC: The Dollar Why

Part 2 of June TIC: The Dollar Why

2020-08-21

Before getting into the why of the dollar’s stubbornly high exchange value in the face of so much “money printing”, we need to first go back and undertake a decent enough review of the guts maybe even the central focus of the global (euro)dollar system.

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

*These* Are The Real Huge Jobs Numbers, And They Will Make Your Blood Run Cold

2020-08-24

There is simply no way to spin these figures as anything good. Not just the usual ones were talking about here, but more so some new data that you probably haven’t seen before. Beginning with the regular, it doesn’t matter that the level of initial jobless claims has declined substantially over the past few weeks

There Have Actually Been Some Jobs Saved, Only In Place of Recovery

There Have Actually Been Some Jobs Saved, Only In Place of Recovery

2020-12-04

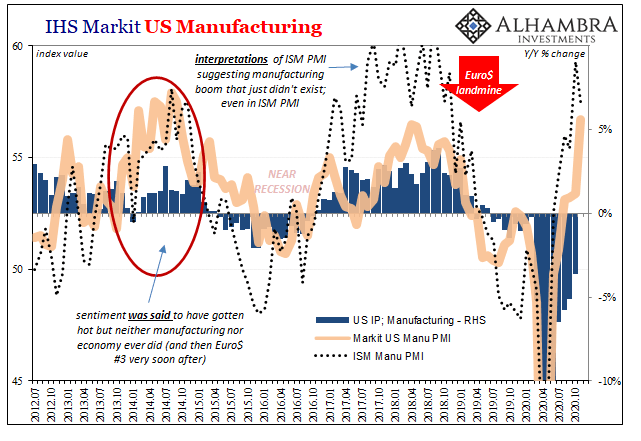

The ISM reported a small decline in its manufacturing PMI today. The index had moved up to 59.3 for the month of October 2020 in what had been its highest since September 2018. For November, the setback was nearly two points, bringing the headline down to an estimate of 57.5.

Tags: consumer goods,currencies,economy,employment,Euro$ #4,Featured,Federal Reserve/Monetary Policy,GFC1,GFC2,global dollar shortage,industrial production,industry,manufacturing,Markets,newsletter,private payrolls,recession