So enjoy the GBOAT (greatest bubble of all time) but watch the clock. Sports fans debate who qualifies as GOAT–the greatest of all time: in hoops, Kobe, Jordan, Kareem, Magic; in boxing, Ali, and so forth. What we have today is GBOAT–the greatest bubble of all time That it’s GOAT is beyond doubt, as the charts below reveal. Bubbles have a few unique characteristics which cannot be captured by financial metrics. The most important such characteristic is that mainstream financial managers don’t see it as a bubble. For those who do admit valuations may be a bit stretched (heh), these professionals shrug and say that since the music’s still playing, they have to keep dancing, i.e. yes there may be a bubble but it won’t pop anytime soon. The other characteristic of

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

So enjoy the GBOAT (greatest bubble of all time) but watch the clock. Sports fans debate who qualifies as GOAT–the greatest of all time: in hoops, Kobe, Jordan, Kareem, Magic; in boxing, Ali, and so forth. What we have today is GBOAT–the greatest bubble of all time That it’s GOAT is beyond doubt, as the charts below reveal. Bubbles have a few unique characteristics which cannot be captured by financial metrics. The most important such characteristic is that mainstream financial managers don’t see it as a bubble. For those who do admit valuations may be a bit stretched (heh), these professionals shrug and say that since the music’s still playing, they have to keep dancing, i.e. yes there may be a bubble but it won’t pop anytime soon. The other characteristic of a bubble is that it continues expanding far beyond historic valuation redlines, as if nothing in the real world (earnings, multiples, etc.) actually matters. Anyone proclaiming such extremes are unsustainable is laughed off the stage as extremes become more extreme, and those who bet against the tsunami of euphoric confidence that this isn’t a bubble can be found huddled in a cardboard box beneath the freeway overpass, begging for a handful of Cheetos. |

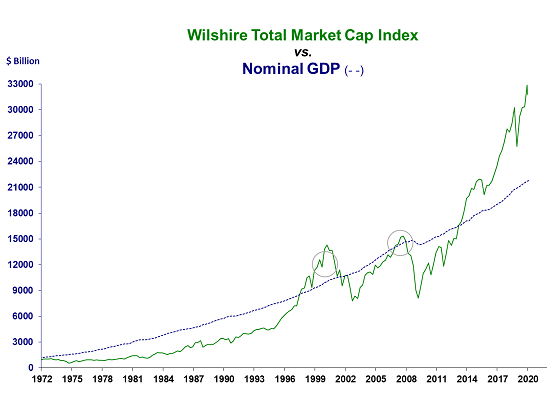

Wilshire Total Market Cap Index vs. Nominal GDP, 1972-2020 - Click to enlarge |

| Another characteristic worth noting is the acceleration of duration, amplitude and volatility as bubbles reach their zenith. So while bulls are cheering the greatest post-election rally in 73 years (or was it 743 years? 2,743 years? Whatever…), they should be quaking in their designer boots for what increasingly manic rallies are signaling: it’s about to pop, baby.

Jesse Felder of TheFelderReport.com succinctly summarized the case for GBOAT in This Is The Textbook Definition Of “Late Cycle” In The Stock Market (Zero Hedge). The charts below bolster the (painfully obvious) case for this being the Wilshire total stock market capitalization to nominal GDP: record disconnect from GDP. Regression to trend: all-time high. (via advisorperspectives.com) |

S&P Composit Index: Regression to Trend, 1870-2020 - Click to enlarge |

| Private sector financial assets as a percentage of GDP: all-time high. |

US Private Sector Financial Assets, 1950-2020 - Click to enlarge |

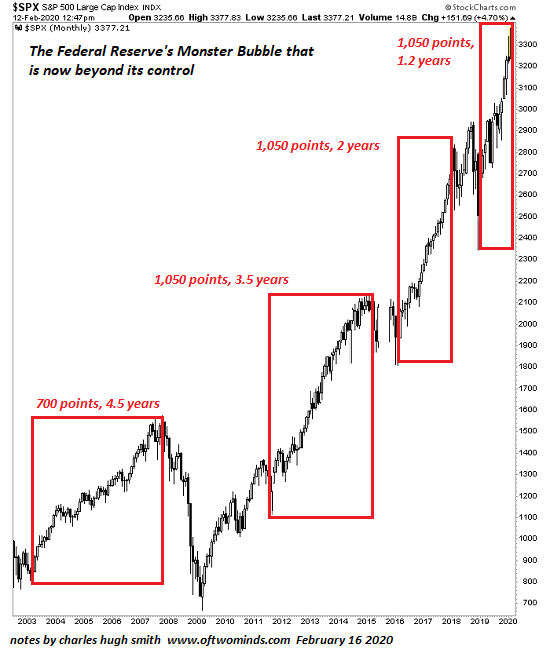

| Every leg higher takes less time and reaches greater extremes:

So enjoy the greatest bubble of all time but watch the clock. Those Cinderella gains vanish at midnight. |

S&P 500 Large Cap Index, 2003-2020(see more posts on S&P 500 Large Cap Index, ) - Click to enlarge |

You Might Also Like

Could America Have a French-Style Revolution?

Could America Have a French-Style Revolution?

As with the French Revolution, that will be the trigger for a wholesale replacement of our failed institutions. Since it’s Bastille Day, a national holiday in France celebrating the French Revolution, let’s ask a question few even think (or dare) to ask: could America have a French-style Revolution? Not in some distant era, but within the next five years?

Welcome to the Crazed, Frantic Demise of Finance Capitalism

Welcome to the Crazed, Frantic Demise of Finance Capitalism

The cognitive dissonance required to ignore the widening gap between the real economy and the fraud’s basic machinery–speculation funded by "money" conjured out of thin air–has reached a level of denial that can only be termed psychotic.

The Bogus “Recovery,” Stress and Burnout

The Bogus “Recovery,” Stress and Burnout

We have three basic ways to counter the destructive consequences of stress.We have all experienced the disorientation and "brain freeze" that stress triggers. The pandemic and the responses to the pandemic have been continuous sources of stress, i.e. chronic stress, which is the pathway to burnout, the collapse of our ability to cope with the burdens pressing on us.

Here’s Why the “Impossible” Economic Collapse Is Unavoidable

Here’s Why the “Impossible” Economic Collapse Is Unavoidable

This is why denormalization is an extinction event for much of our high-cost, high-complexity, heavily regulated economy. A collapse of major chunks of the economy is widely viewed as “impossible” because the federal government can borrow and spend unlimited amounts of money because the Federal Reserve can create unlimited amounts of money: the government borrows $1 trillion by selling $1 trillion in Treasury bonds, the Fed prints $1 trillion dollars to buy the bonds.

Our Systemic Drift to Collapse

Our Systemic Drift to Collapse

Thus do the lazy complacent passengers drift inexorably toward the cataracts of collapse just ahead. The boat ride down to the waterfall of systemic collapse is not dramatic, it’s lazy drifting: a lazy complacency that doing more of what worked in the past will work again, and an equally lazy disregard for how far the system has drifted from the point when things actually worked.

This Is How It Ends: All That Is Solid Melts Into Air

This Is How It Ends: All That Is Solid Melts Into Air

While the Federal Reserve and the Billionaire Class push the stock market to new highs to promote a false facade of prosperity, everyday life will fall apart. How will the status quo collapse? An open conflict–a civil war, an insurrection, a coup–appeals to our affection for drama, but the more likely reality is a decidedly undramatic dissolution in which all the elements of our way of life we reckoned were solid and permanent simply melt into air, to borrow Marx’s trenchant phrase.

Everything is Staged

Everything is Staged

All the staging is a means to an end, and everyone in America is nothing more than a means to an end: close the sale so the few can continue exploiting the many. You know how realtors stage a house to increase its marketability: first, they remove all evidence that people actually live there.

What We Don’t Elect Matters Most: Central Banking and the Permanent Government

What We Don’t Elect Matters Most: Central Banking and the Permanent Government

We’re Number One in wealth, income and power inequality, yea for the Fed and the Empire! If we avert our eyes from the electoral battle on the blood-soaked sand of the Coliseum and look behind the screen, we find the powers that matter are not elected: our owned by a few big banks Federal Reserve, run by a handful of technocrats, and the immense National Security State, a.k.a. the Permanent Government.

Tags: Featured,newsletter