After the Diamond Princess cruise ship docked in Tokyo with tales seemingly spun from some sci-fi disaster movie, all eyes turned to Japan. Cruisers had boarded the vacation vessel in Yokohama on January 20 already knowing that there was something bad going on in China’s Wuhan. The big ship would head out anyway for a fourteen-day tour of Vietnam, Taiwan, and, yes, China. Three days in, news reached the Diamond that the Communists had closed down the affected region. Worse, on February 2, the company operating the tour disclosed to the captain that one passenger who had disembarked in Hong Kong tested positive for this novel coronavirus. The crew and passengers were told they had to immediately turn around and head back toward Tokyo. What followed was a nightmare.

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Bank of Japan, currencies, economy, Featured, Federal Reserve/Monetary Policy, industrial production, Japan, Markets, newsletter, QE, QQE, Retail sales, Shinzo Abe

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

After the Diamond Princess cruise ship docked in Tokyo with tales seemingly spun from some sci-fi disaster movie, all eyes turned to Japan. Cruisers had boarded the vacation vessel in Yokohama on January 20 already knowing that there was something bad going on in China’s Wuhan. The big ship would head out anyway for a fourteen-day tour of Vietnam, Taiwan, and, yes, China.

Three days in, news reached the Diamond that the Communists had closed down the affected region. Worse, on February 2, the company operating the tour disclosed to the captain that one passenger who had disembarked in Hong Kong tested positive for this novel coronavirus.

The crew and passengers were told they had to immediately turn around and head back toward Tokyo.

What followed was a nightmare. Since it was pretty much the only information the world had at the time about this disease, it played an outsized role in provoking often draconian responses. The numbers would end up projecting a situation beyond imagination, invoking the Spanish flu.

But those ended up being an unusual outlier, a case study only in what the most perfect conditions for the viral spread might unleash. It wasn’t representative, at all, for how the rest of the world would end up facing COVID-19. And it was nothing like what Japan would experience.

While Tokyo would fall under suspicion for the Diamond Princess sitting in its harbor under quarantine, as well as its close links to China, the Japanese government didn’t panic and never did impose a country-wide lockdown. Prime Minister Abe would issue restrictions, of course, but only asking that the Japanese people heed guidelines along with a healthy dose of common sense.

In the middle of May, the Abe government began to roll back those recommended restrictions with most of Japan already stirring back to life. As the AP reported:

Under the emergency, people were asked to stay at home and non-essential businesses were requested to close or reduce operations, but there was no enforcement. Since May 14, when the measures were lifted in most of Japan, more people have been leaving their homes and stores have begun reopening.

At the time, there had been 16,600 confirmed COVID cases, with 850 reported deaths associated with the disease.

|

While good news, to be sure, these figures can’t be taken in isolation. The question which will really plague Japan, as across the rest of the world, one which I fear we all will be forced to wrestle with and debate endlessly for years: was it worth it? There is this information asymmetry to begin with; we will never know just how many deaths and health problems might have appeared had things gone differently, a lighter touch focused instead on the most vulnerable rather than blanket measures unnecessarily imposed upon those with little danger. On the other hand, though, we are starting to get a sense of what it cost. In Japan, where the death toll remains fewer than 1,000 out of a total population of more than 126 million, more and more it appears like the economic collapse will only get sorted out over years; certainly not months. And that’s according to the mainstream econometric models which in Japan place a surplus of effort into the QQE column (despite it having moved into its eighth year of existence). Japan may have come back during May 2020, its economy did not. |

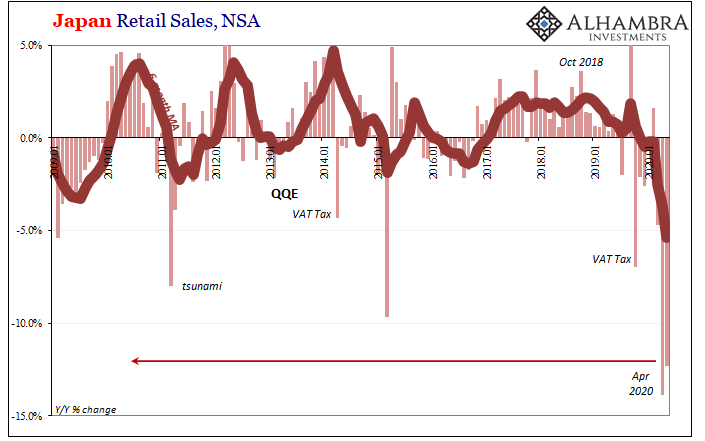

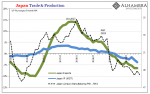

Japan Retail Sales, NSA 2009-2020(see more posts on Japan Retail Sales, ) - Click to enlarge |

| Retail sales, for one thing, had plummeted during April down by almost 14% year-over-year, a level of economic destruction the country hadn’t seen since the darkest days of its (first) Lost Decade in 1998’s Asian flu. While some were expecting a sizeable turnaround, it ended up being more like the US payroll report (which was only hyped because it had a plus sign in front, not because it realistically indicated a significant, meaningful rebound).

Ostensibly a positive number, too, the seasonally-adjusted figure measured just +2.1% from April’s deep trough. Unadjusted, retail sales were down more than 12% – the second double-digit decline in a row – in May’s estimates. |

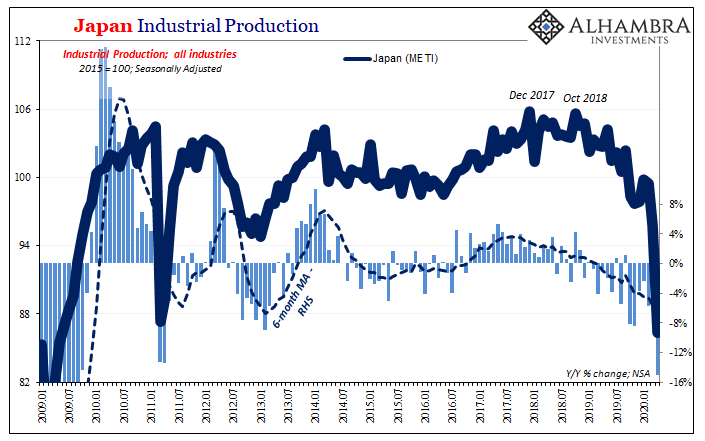

Japan Industrial Production, 2009-2020(see more posts on Japan Industrial Production, ) - Click to enlarge |

| Prime Minister Abe was quick to take credit for the first set of results, those of the pandemic; “We were able to bring the outbreak nearly under control in just a month and a half in a uniquely Japanese way.” In the long run, however, it is the second set which may doom his government.

The people in Japan have put up with two dozen QE’s including three different versions of QQE, and the lack of growth in the economy none of them could turn around. Imposing a deep recession, however, is a categorically different story. Already deeply pessimistic about an upside that may no longer exist, that doesn’t mean anyone will just accept a possibly deep downside with protracted negative pressures. Unlike in America, in Japan there was already unease over the state of the economy heading into 2020. While central bankers here declared it no more than a close call in 2019, those in Japan were already revving QQE back up because the global economy had pulled the Japanese economy into the significant minuses. And then this. Poll after poll conducted inside and outside the country has rated the Japanese government the worst – by its own citizens. And yet, Japan has hardly been hit compared with almost every other. Why the huge disparity? |

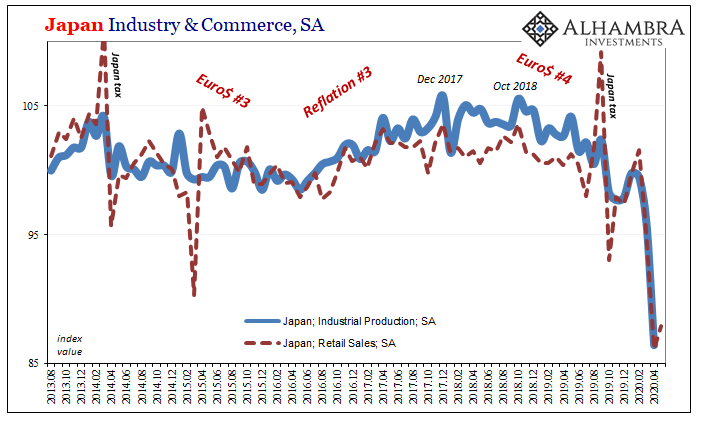

Japan Industry & Commerce, SA 2013-2020 - Click to enlarge |

But the way its leaders dealt with the crisis were rated poorest by citizens in all four fields — politics, business, community and media. The overall score, 16, was worst as well. Most often these write-ups go on to emphasize intangibles, or the lack of them being exhibited by officials; leadership or displaying public confidence. It obviously isn’t actual results, at least those so far as the pandemic is concerned, that is driving such widespread skepticism and frustration. Whatever the reason, where the economy is concerned the Japanese should be weeks if not months ahead of the rest of the world. Instead, the data continues to suggest the worst potential outcome – globally synchronized. The term globally synchronized growth, 2017’s key buzzword, may end up most relevant in its opposite place three years thereafter. A warning, perhaps, for even those nations currently enjoying higher approval ratings than Abe’s basement levels. Once the virus runs its course, what are the chances the economic disaster eclipses it in the long run conversation? A no-win situation from the beginning, still, when we look back after having completed what increasingly looks like the rough couple of years before all of us, which will end up still dominant over that future? |

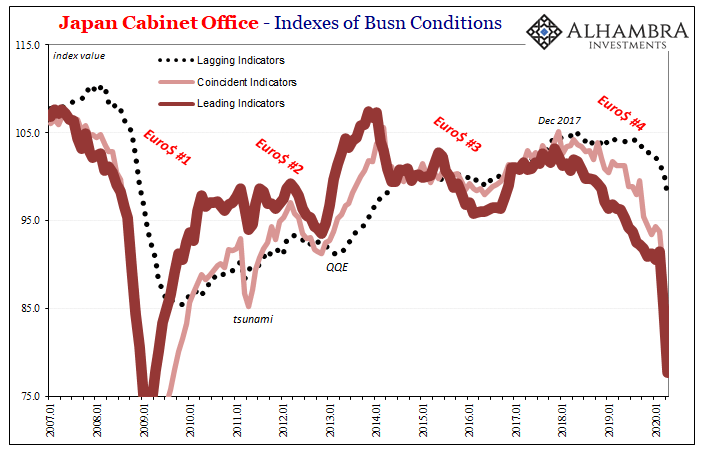

Japan Cabinet Office, 2007-2020 - Click to enlarge |

You Might Also Like

What Happens When Central Banks Buy Stocks (ETFs)? Well, We Already Know

What Happens When Central Banks Buy Stocks (ETFs)? Well, We Already Know

Can we please dispense with all notions that monetary policy works? Specifically balance sheet expansion via any scale asset purchase programs. Nowhere has that been more apparent than Japan. Go back and reread all the promised benefits from BoJ’s Big Bang QQE that were confidently written in 2013. The biggest bazooka ever conceived has fallen short in every conceivable way.

There Was Never A Need To Translate ‘Weimar’ Into Japanese

There Was Never A Need To Translate ‘Weimar’ Into Japanese

After years of futility, he was sure of the answer. The Bank of Japan had spent the better part of the roaring nineties fighting against itself as much as the bubble which had burst at the outset of the decade. Letting fiscal authorities rule the day, Japan’s central bank had largely sat back introducing what it said was stimulus in the form of lower and lower rates.No, stupid, declared Milton Friedman.

From QE to Eternity: The Backdoor Yield Caps

From QE to Eternity: The Backdoor Yield Caps

So, you’re convinced that low rates are powerful stimulus. You believe, like any good standing Economist, that reduced interest costs can only lead to more credit across-the-board. That with more credit will emerge more economic activity and, better, activity of the inflationary variety. A recovery, in other words. Ceteris paribus. What happens, however, if you also believe you’ve been responsible for bringing rates down all across the curve…and then no recovery.

Two Years And Now It’s Getting Serious

Two Years And Now It’s Getting Serious

We knew German Industrial Production for December 2019 was going to be ugly given what deStatis had reported for factory orders yesterday. In all likelihood, Germany’s industrial economy ended last year sinking and maybe too quickly. What was actually reported, however, exceeded every pessimistic guess and expectation – by a lot.

The Big And Small of Leading Japan

The Big And Small of Leading Japan

In the middle of 2018, Japan, they said, was riding so high. Gliding along on the tidal wave of globally synchronized growth, Haruhiko’s courage and more so patience had finally delivered the long-promised recovery. The Japanese economy had healed to a point that its central bank officials believed it time to wean the thing off decades of monetary “stimulus.”

Schaetze To That

Schaetze To That

When Mario Draghi sat down for his scheduled press conference on April 4, 2012, it was a key moment and he knew it. The ECB had finished up the second of its “massive” LTRO auctions only weeks before. Draghi was still relatively new to the job, having taken over for Jean-Claude Trichet the prior November amidst substantial turmoil.

The Smallness of the Most Gigantic

The Smallness of the Most Gigantic

These numbers do seem epic, don’t they? It’s hard to ignore when you have the greatest percentage increase in the history of a major economic account. Just writing that sentence it’s difficult to deny the power of those words. Which is precisely the point: we already know ahead of time how the biggest economic holes in history are going to produce the biggest positives coming out of them.

Wait A Minute, What’s This Inversion?

Wait A Minute, What’s This Inversion?

Back in the middle of 2018, this kind of thing was at least straight forward and intuitive. If there was any confusion, it wasn’t related to the mechanics, rather most people just couldn’t handle the possibility this was real. Jay Powell said inflation, rate hikes, and accelerating growth. Absolutely hawkish across-the-board.And yet, all the way back in the middle of June 2018 the eurodollar curve started to say, hold on a minute.

Tags: Bank of Japan,currencies,economy,Featured,Federal Reserve/Monetary Policy,industrial production,Japan,Markets,newsletter,QE,QQE,Retail sales,Shinzo Abe