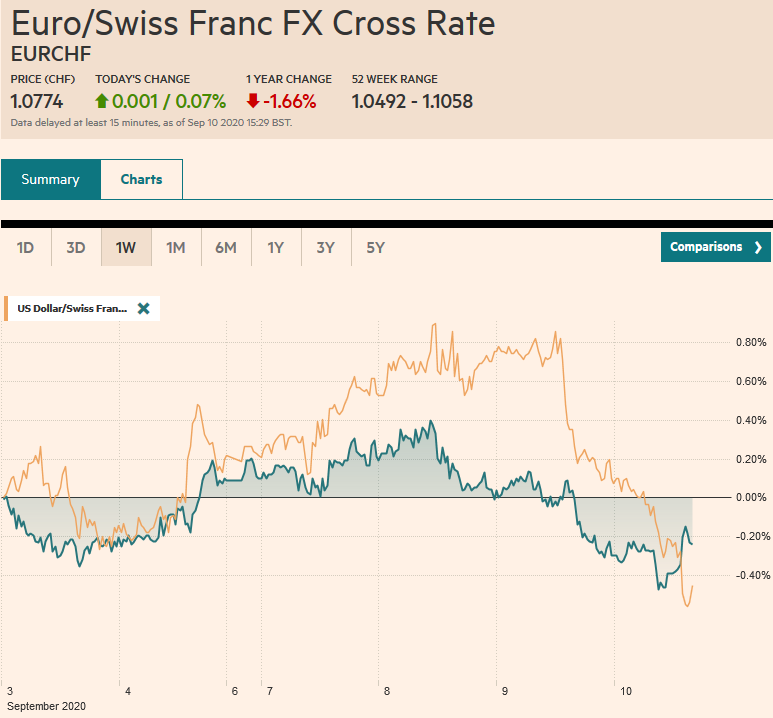

Swiss Franc The Euro has risen by 0.07% to 1.0774 EUR/CHF and USD/CHF, September 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: A strong recovery in US stocks, a softer dollar, and higher gold and oil prices may signal the end of the brief though dramatic correction, but the market is in a bit of a holding pattern ahead of the ECB meeting. Most of the major equity markets in the Asia Pacific region stabilized, except for Hong Kong and China. Indonesia’s plan to reimpose social distancing protocols saw the Jakarta Composite slump 5% before circuit breakers kicked in. European shares are giving back about a quarter of yesterday’s 1.6% increase, and US shares trading heavily after yesterday’s strong

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of Canada, Currency Movement, ECB, Featured, Mexico, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.07% to 1.0774 |

EUR/CHF and USD/CHF, September 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

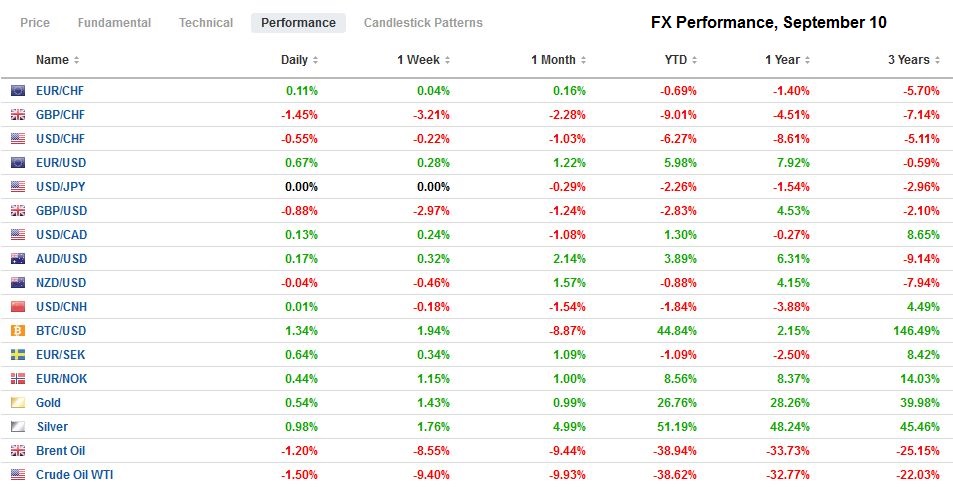

FX RatesOverview: A strong recovery in US stocks, a softer dollar, and higher gold and oil prices may signal the end of the brief though dramatic correction, but the market is in a bit of a holding pattern ahead of the ECB meeting. Most of the major equity markets in the Asia Pacific region stabilized, except for Hong Kong and China. Indonesia’s plan to reimpose social distancing protocols saw the Jakarta Composite slump 5% before circuit breakers kicked in. European shares are giving back about a quarter of yesterday’s 1.6% increase, and US shares trading heavily after yesterday’s strong advance. Periphery European bond yields are lower, while the core is flat to slightly higher. The US 10-year benchmark yield is little changed a hair below 70 bp. Among the major currencies, the dollar-bloc are seeing yesterday’s gains pared. Sterling is hovering around $1.30. The euro and Swiss franc has have extended yesterday’s gains and are up about 0.3% near midday in Europe. Emerging markets currencies are narrowly mixed, and the JP Morgan Emerging Market Currency Index that rose almost 0.9% yesterday is fractionally higher today. Gold is hovering around $1950 after the $1900 area held yesterday. Oil is also consolidating yesterday’s recovery, leaving the Oct WTI contract near $37.50. |

FX Performance, September 10 - Click to enlarge |

Asia Pacific

Japan reported core machinery orders rose 6.3%in July, well above expectations, and recoup a chunk of the 7.6% decline in June. The increase in the proxy for capex lends credence to ideas that after a three-quarter contraction, the world’s third-largest economy is expanding here in Q3. With a new Prime Minister a week away and elections rumored for Oct/Nov, a supplemental budget seems even more likely than before. The BOJ meets next week, and although it may be too soon for a move, Governor Kuroda may set the stage for new measures, perhaps new loans with negative rates, as the ECB has done.

Tomorrow, Japan will report August producer prices. Although they likely increased for the third consecutive month, the year-over-year pace will most likely remain below zero as it has since February. With some conservative assumptions, it can return to positive territory in Q4. Ahead of the weekend, China may report is money supply and lending figures for August. Bank lending is expected to have risen by a quarter over the nearly CNY1 trillion lent in July. However, the non-banking financial institutions, which include the wealth-management arms of banks, appear to have lend as much as the banks.

The dollar fell to JPY105.80 yesterday but is holding above JPY106 today. It is in about a 30-tick range. Large expiring options may ringfence it today. Support the greenback are $3.7 bln in options between JPY105.80 and JPY106.00. Capping the upside maybe $1.2 bln in options struck between JPY106.50 and JPY106.75. The Australian dollar is consolidating yesterday’s recovery and is in about a quarter-cent range above $0.7260. Nearby resistance is at the week’s high near $0.7300,, while support extends toward $0.7250. At CNY6.8331, the PBOC’s reference rate for the dollar was in line with the median forecast in the Bloomberg survey of bank models. After weakening steadily in August, the US dollar appears to be carving out a new near-term range of roughly CNY6.81 to CNY6.86.

Europe

The ECB dominates today’s agenda. There are no expectations for fresh actions. Instead, keen interest is how ECB President Lagarde frames the issues and respond to recent developments. The press reported that the officials are a little more confident then they were in June, the last time the forecasts were updated. Yet, as Germany has shown, it could be a two-edged sword. It revised up 2020 growth but cut next year’s. Just as importantly, disinflation/deflationary concerns are elevated. The preliminary August inflation was unexpectedly weak. Not only did the headline fall into negative territory, but the core rate tumbled to new record lows (0.4%). We are sympathetic to arguments that the inflation data is so skewed by various shocks related to the pandemic and the response that it makes little sense to put much stock in it now. Yes, it is low, but deflation probably overstates the case. The “close to but lower than 2%” inflation target is being reviewed, but the conclusion of the strategic view is expected next year., making it unlikely that it can respond in kind to the Fed’s move.

Lagarde may be pressed to discuss the exchange rate, but she is deft. No doubt what the ECB’s chief economist Lane said is factually true; the exchange rate is input into its models and assessment of economic conditions. A decision to increase extend the Pandemic Emergency Purchase Program is anticipated in December. Lagarde can also caution against reading much into the weekly changes in the bond-buying efforts that are influenced by a number of factors, none of which contain signals of ECB’s policy intent. We expect that after the ECB press conference, attention will swing back to next week’s FOMC meeting, where a more overtly dovish posture is likely. The euro has been in a $1.17-$1.19 range and prematurely jumped higher. The market got ahead of itself and fell back toward the lower end of the range yesterday (~$1.1755) before recovering (~$1.1835).

Last week, Germany reported disappointing industrial output figures (1.2% instead of the median forecast in the Bloomberg survey for a 4.5% gain). France disappointed today. July industrial production rose by 3.8%, not the 5% economists projected, and the small upward revision in June (13.0% from 12.7%) underscores a slower pace. A bright spot, though, was manufacturing output was stronger than anticipated at 4.5% (vs. 3.5%). Italy was the source of a pleasant surprise. July industrial output jumped 7.4%, more than twice the median forecasts, and almost matches June’s 8.2% increase.

The euro traded on both sides of Tuesday’s range yesterday, but the close was within the range. Today it has edged a little higher (~$1.1840), just below the 20-day moving average and the (38.2%) retracement of the retreat from above $1.20. The ECB is likely to inject some intraday volatility. Support is seen near $1.18. The $1.1780-$1.1800 houses 2.2 bln of euro options that expire today. Another for nearly 790 mln euros is struck at $1.1890. Sterling’s dramatic recovery yesterday from $1.2885 back above $1.30 reflects the US dollar’s setback rather than a bullish pound view. Recall that the euro finished last week near GBP0.89 and pushed above GBP0.91 yesterday and has straddled that area today.

America

The Bank of Canada did not surprise yesterday. It promised to keep rates down until the slack in the economy is absorbed. It will continue to buy at least C$5 bln a week of government bonds, though hinted it could adjust the buying if needed. It dropped language that suggests it is prepared to take additional measures, which seems to imply a more optimistic outlook. Bank of Canada Governor Macklem gives a speech today and then holds a press conference that could shed more light on the outlook. The Bank of Canada’s balance sheet swelled to about 27% of GDP (~C$540 bln) in July but has stabilized as the increase in bond holdings offsets the maturing bills. The Bank of Canada’s monetary policy meeting is October 28.

The US reports weekly jobless claims and August producer prices. A small monthly rise in producer prices is expected, but the year-over-year rate is unlikely to improve much from the -0.4% reading in July. The core measure is expected to tick up by 0.2% but leaves the year-over-year rate at 0.3%. Weekly jobless claims may be more challenging to read, given that new seasonal adjustment that makes comparisons difficult. The median forecast in the Bloomberg survey looks for 850k weekly initial jobless claims, down from about 880k the previous week. Oil and gasoline inventory data may attract more interest than usual after the API estimates that oil stocks rose for the first time in six weeks, while gasoline stocks tumbled for a fifth week.

The US dollar rose to almost CAD1.3260 yesterday after having slipped below CAD1.30 on September 1. Yesterday’s high was its best level since mid-August. However, the greenback reversed lower and settled near Cad1.3145, the session’s low. It slipped a little more today (~CAD1.3130) but held the (50%) retracement of the rally since the start of the month (~CAD1.3125). It seems to be at the mercy of the broader greenback movement and the risk-appetites, which don’t seem as enthusiastic as yesterday. The US dollar posted a big outside down day against the peso yesterday. The 200-day moving average (~MXN21.56) now offers nearby resistance. The next big target is near MXN21.00. The higher than expected CPI yesterday, above the upper end of the central bank’s target, means that the attractive cetes rates (peso bills) of around 4.4% continue to attract funds.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

FX Daily, September 09: Investor Anxiety Continues to Run High Despite Some Stability in the Capital Markets

News that the AstraZeneca Phase 3 test had to be stopped to study the adverse reaction of one subject added to the uncertainty of investors amid one of the more significant reversals of risk appetites since March. Equities continued to slump in the Asia Pacific region, with many large markets off more than 1%, led by Australia’s more than 2% decline.

FX Daily, May 26: Fear is Still on Holiday

FX Daily, May 26: Fear is Still on Holiday

Overview: The heightened tensions between the US and China sapped risk-appetites before the weekend, but appear to be missing in action today. Equity markets have rebounded strongly. Nearly all the equity markets in the Asia Pacific region rose (India was a laggard) led by an almost 3% rally in Australia, which was seen as particularly vulnerable to the Sino-American fissure.

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

Overview: Profit-taking, perhaps spurred by disappointing retail sales figures, sent Chinese equity markets down by 4.5%-5.2% today, the most since early February. It appears to be triggering a broader setback in equities today. The Hang Seng fell 2%, and most other markets in the region were off less than 1%.

FX Daily, July 28: Dollar Bounces, Gold Slips, while Equities Hold Their Own

FX Daily, July 28: Dollar Bounces, Gold Slips, while Equities Hold Their Own

The main development in the capital markets today is the firmer dollar against nearly all the major and emerging market currencies. Among the majors, the New Zealand dollar and Swedish krona are the heaviest (~-0.4%), while the Swiss franc and yen are marginally lower.

FX Daily, July 30: Greenback’s Bounce is Likely Short-Lived

FX Daily, July 30: Greenback’s Bounce is Likely Short-Lived

A wave of profit-taking is seen through most of the capital markets today, with the exception of the bond market, where yields continue to trend lower. The US 10-year is now yielding 55 bp, a new low since early March, and the five-year yield set a new record low near 23 bp. European yields are 2-4 bp lower.

FX Daily, September 1: Dollar Lurches Lower

FX Daily, September 1: Dollar Lurches Lower

The US dollar has been sold-off across the board. The euro approached $1.20, and sterling neared $1.3450. The greenback traded below CAD1.30 for the first time since January. Most emerging market currencies but the Turkish lira, are also advancing today.

FX Daily, September 3: Corrective Forces Maintain Grip

FX Daily, September 3: Corrective Forces Maintain Grip

The US dollar is continuing to recover after hitting new lows earlier in the week. It is lower against all the major currencies and most of the emerging markets. A report in the Financial Times suggesting that there is a concern about the euro’s recent strength at the ECB has added a bit more fuel to the move, and the euro, which had pushed above $1.20 earlier in the week, briefly traded below $1.18.

Tags: #USD,Bank of Canada,Currency Movement,ECB,Featured,Mexico,newsletter