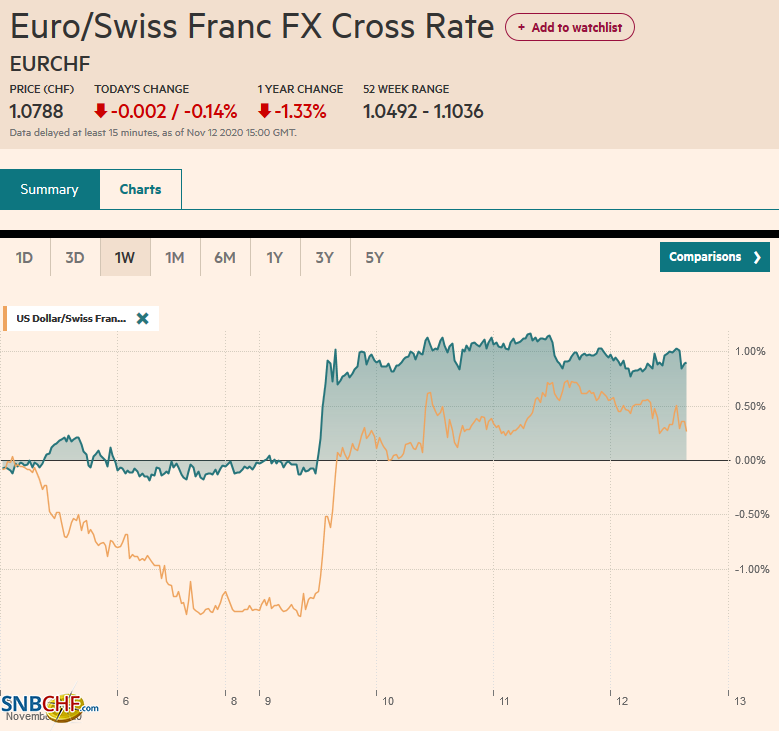

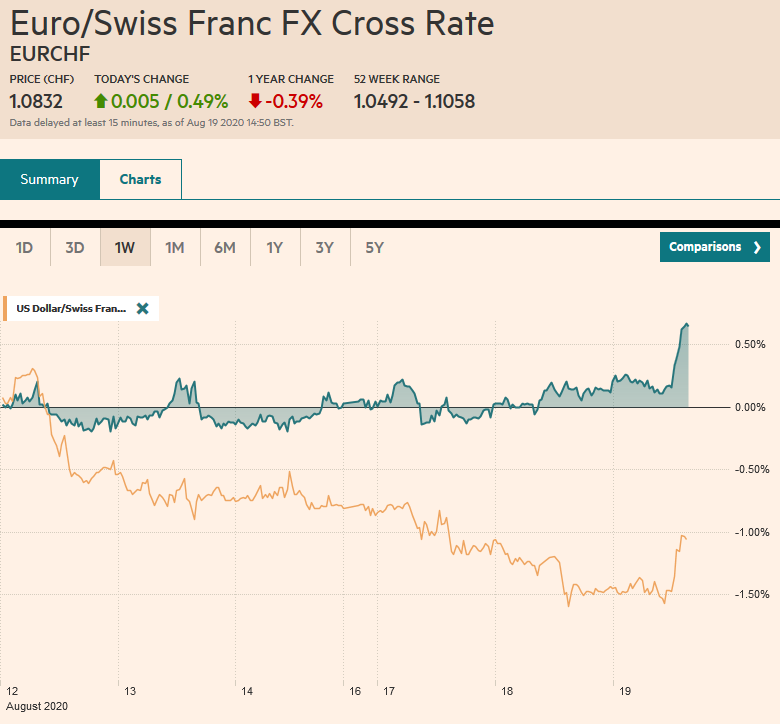

Swiss Franc The Euro has fallen by 0.14% to 1.0788 EUR/CHF and USD/CHF, November 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: There is a nervous calm in the capital markets today. The equity rally in the Asia Pacific region stalled to end an eight-day rally, though the Nikkei’s rally remains intact. The Dow Jones Stoxx 600 in Europe is consolidating near eight-month highs visited yesterday, and US shares mixed, with the NASDAQ futures a little higher and the S&P futures slightly lower. US cash bond trade resumed today after yesterday’s holiday, and the benchmark 10-year yield is off a few basis points to 0.94%. European bond yields are lower as well, and Greece’s two-year yield is at a new record lower

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, Featured, Japan, Mexico, newsletter, Turkey, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.14% to 1.0788 |

EUR/CHF and USD/CHF, November 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: There is a nervous calm in the capital markets today. The equity rally in the Asia Pacific region stalled to end an eight-day rally, though the Nikkei’s rally remains intact. The Dow Jones Stoxx 600 in Europe is consolidating near eight-month highs visited yesterday, and US shares mixed, with the NASDAQ futures a little higher and the S&P futures slightly lower. US cash bond trade resumed today after yesterday’s holiday, and the benchmark 10-year yield is off a few basis points to 0.94%. European bond yields are lower as well, and Greece’s two-year yield is at a new record lower of minus 6.5 bp. The dollar is mixed, with the sterling and the dollar bloc softer and the euro, yen, and Swiss franc a little firmer. The Turkish lira is extending yesterday’s sharp gains, while many of the regional Asia Pacific currencies lower and the European complex mostly higher. The JP Morgan Emerging Market Currency Index is about 0.25% higher after a six-day advance ended yesterday. Gold is firmer but is still consolidating near the lows set Monday. More talk that OPEC+ may delay the output increase well into next is helping underpin prices. The December WTI futures contract poked above $43 yesterday for the first time in two months. It is consolidating this week’s bounce (from almost $37 on Monday). Initial support now is seen near $40.80. |

FX Performance, November 12 . |

Asia PacificJapan’s core machine orders, which are seen as a lead indicator of capex, fell 4.4% in September, well more than expected. On the other hand, the tertiary index (service sector) was stronger than expected, rising 1.8% on the month, half again as high as economists forecast. It is the best since the outsized snapback in June (9%) after a four-month slide as the virus struck. Japan reports Q3 GDP next week. A 4.4% quarter-over-quarter increase in output is projected after the world’s third-largest economy contracted for the previous three quarters. Similar to other major countries, growth appears to be slower here in Q4. Prime Minister Suga formally began the process of cobbling together a third supplemental budget. |

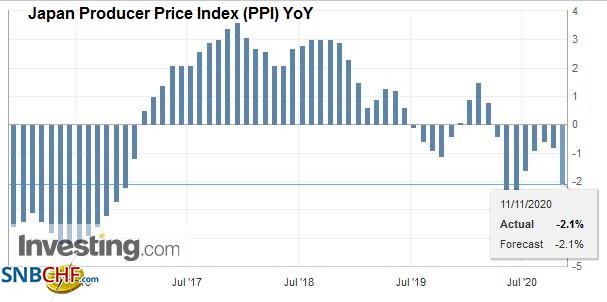

Japan Producer Price Index (PPI) YoY, October 2020(see more posts on Japan Producer Price Index, ) Source: investing.com - Click to enlarge |

Last week as the dollar broke below JPY104 for the first time since March and fell to almost JPY103, Japanese institutional investors took advantage of the strong yen to boost foreign bond buying. The weekly data from the Ministry of Finance reported Japanese investors purchased JPY1.365 trillion of foreign bonds. To put those purchases in perspective, consider that the four-week average is near JPY200 bln, and the year’s weekly average before last week was just below JPY300 bln. Meanwhile, foreign investors do not appear to be participating very much in the rally that has lifted the Nikkei to its best level since the early 1990s. They did buy JPY485 bln of Japanese equities last week, but in the previous eight-weeks, foreign investors sold an average of about JPY103 bln a week.

The dollar is chopping around the upper end of this week’s range that saw a high yesterday, a little shy of JPY105.70. It is in about a third of a yen range today above JPY105.15. We imagine that the roughly $1.4 bln in options in the JPY105.40-JPY105.50 area that expire today have been neutralized. The intraday technicals suggest mild pressure on the dollar’s downside is likely early North American activity. The Australian dollar is also consolidating. Its dip below $0.7250, setting the low for the week and was snapped up in the European morning. The $0.7290-$0.7300 offers resistance. The US dollar is mostly within yesterday’s range against the Chinese yuan. It is the first session this week that the greenback has held above CNY6.60. The high for the week was set on Monday near CNY6.6345. The PBOC set the dollar’s reference rate at CNY6.6236, in line with the projections. A squeeze in the money markets continues, and the overnight repo rate rose to 2.56%, the highest since January. The PBOC injections in the money market have been small, and officials appear to have been probing participants about possibly exiting the monetary easing given the economic recovery. The PBOC is expected to inject at least CNY200 bln via the medium-term lending facility on Monday.

EuropeThe ECB’s summit continues today, and Fed chief Powell will speak later today. Lagarde’s comments yesterday helped shape expectations for next month’s ECB meeting, at which officials have practically guaranteed new measures. Lagarde said that the flexible Pandemic Emergency Purchase Program (PEPP) and Targeted Long-Term Refinancing Operations (cheap loans) will be the main tools. This seemed to play down the likelihood of a rate cut, even though the reversal rate (the rate at which the negative rates prove counterproductive) is closed to minus 100 bp (deposit rate is now minus 50 bp). |

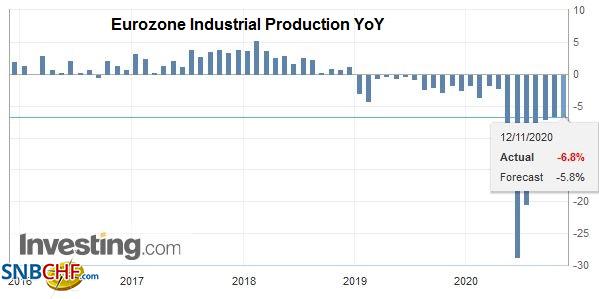

Eurozone Industrial Production YoY, September 2020(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

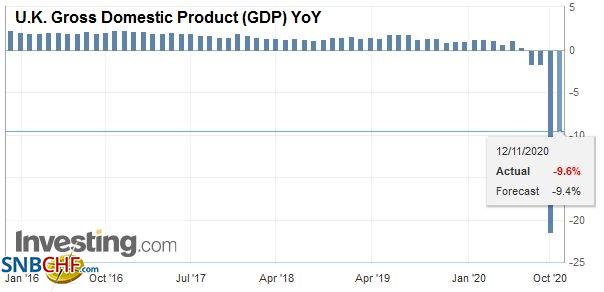

| The UK’s Q3 GDP of 15.5% was a bit softer than expected, primarily because activity was weaker than forecast in September. The British economy contracted by nearly 20% in Q2. In Q3, private consumption rebounded smartly (18.3% vs. -23.6%), while government spending was slower than anticipated (7.8% vs. median forecast for a 12.0% increase). |

U.K. Gross Domestic Product (GDP) YoY, Q3 2020(see more posts on U.K. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| Exports rose 5.1% in the quarter, half as much as expected, while the 13.2% increase in imports was about a third less than projected. September’s monthly GDP rose 1.1% instead of 1.5% after 2.2% in August. |

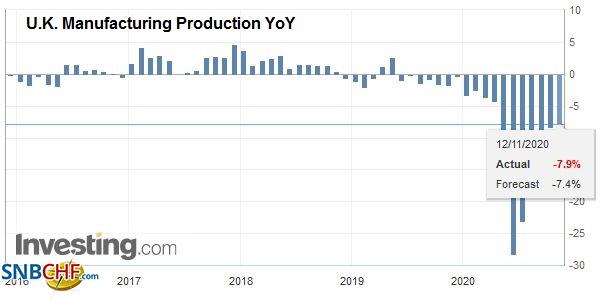

U.K. Manufacturing Production YoY, September 2020(see more posts on U.K. Manufacturing Production, ) Source: investing.com - Click to enlarge |

| Industrial output rose 0.5%, about half of what economists expected, and output in the service sector expanded by 1.0% rather than 1.3%. |

U.K. Industrial Production YoY, September 2020(see more posts on U.K. Industrial Production, ) Source: investing.com - Click to enlarge |

| The takeaway is the UK economy finished Q3 on a soft note, and with the new shutdowns, the Bank of England has projected the economy is contracting here in Q4. |

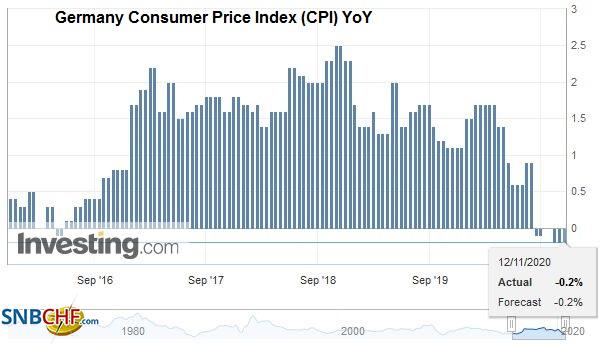

Germany Consumer Price Index (CPI) YoY, October 2020(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

Turkey appears to be turning a corner with a new central bank governor and a new finance minister. President Erdogan signaled he is ready for the “bitter” medicine, which likely means a formal rate hike next week. Yesterday, Turkey announced it will boost the amount of swaps and derivative deals local banks can conduct with foreign investors/banks. This easing of a capital control is also seen as a signal of a coming rate hike. The dollar reached almost TRY8.58 last week and tested TRY7.6850 today. It is difficult to talk about support for greenback, but there appears to be potential toward TRY7.50.

The euro is firm within yesterday’s range (~$1.1745-$1.1835). It probably requires a move above $1.1855 to be anything noteworthy. Sterling rose a little past $1.3310 yesterday but met a wall of sellers that pushed it back to $1.32, and follow-through selling today has taken it to almost $1.3160. Initial support is seen near $1.3140, and a break of it could see $1.3080 initially. There has been a big adjustment on the cross. The euro fell to about GBP0.8860 yesterday, a six-month low, but rebounded to leave a possible (bullish) hammer candlestick in its wake. Follow-through buying today has lifted the euro to almost GBP0.8965. A move above GBP0.9000 lifts the tone.

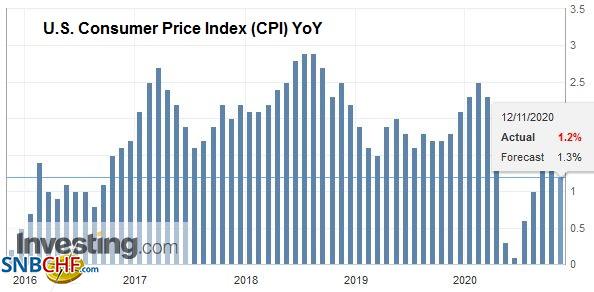

AmericaAfter yesterday’s partial holiday, the US returns today with the October CPI and the weekly initial jobless claims for the week ending November 7. |

U.S. Consumer Price Index (CPI) YoY, October 2020(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| Consumer inflation is expected to edge higher (0.1% on the headline and 0.2% on the core measures), but given the base effect (what happened a year ago), the year-over-year measures are expected to be little changed at 1.3% and 1.7% for the headline and core respectively. Remember, housing and health care are the two biggest components. |  |

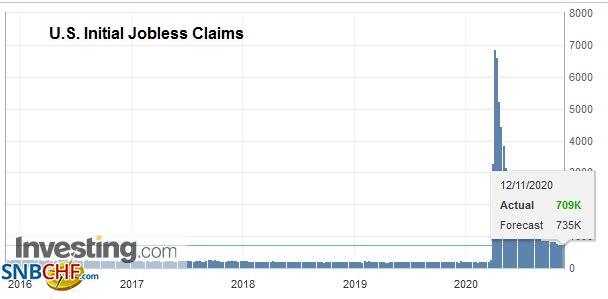

| Weekly jobless claims draw much attention, but they may not be capturing what is happening as those who exhaust their benefits can and are receiving assistance under the Pandemic Emergency Unemployment Compensation program. Meanwhile, as new curfews, shutdowns, and social restrictions are implemented, the demand for a new Payroll Protection Progam increase. |

U.S. Initial Jobless Claims, November 12 2020(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

The central bank of Mexico (Banxico) is widely, though not universally, expected to deliver a 25 bp rate cut today that would bring the overnight rate to 4%. The overnight target rate was 7.25% at the end of last year. Today marks the eighth cut of the year. Current inflation readings are just above 4%, the upper end of the 2-4% target range. Yesterday, the peso was pressured by local press reports that Finance Minister Herrera was going to step down. The report was denied. Also yesterday, Fitch reaffirmed its BBB- sovereign rating for Mexico with a stable outlook.

At the end of October, the US dollar tested CAD1.34 resistance. It subsequently sold-off and reached CAD1.2930 at the start of this week. The CAD1.3100 area tested in Asia today is a (38.2%) retracement of the decline. The greenback was sold in early European activity, and initial support is seen near CAD1.3050 and then CAD1.3020 today. The US dollar made a marginal new high for the week against the Mexican peso slightly in front of MXN20.63. The consolidative tone may persist through the central bank announcement later in the sessions. Support is seen in the MXN20.25-MXN20.30.area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

FX Daily, August 19: US Equities Outperform but Does Little for the Heavy Greenback

Overview: The S&P 500 and NASDAQ set new all-time highs yesterday, but the continued outperformance of US equities have failed to lend the dollar much support. It was sold to new lows for the year yesterday against the euro, sterling, the Swedish krona, and the Australian dollar.

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

FX Daily, August 31: Month-End Gyrations and the Fed’s Ad Hocery

Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week.

FX Daily, October 1: Hope Springs Eternal

FX Daily, October 1: Hope Springs Eternal

Speculation that a new round of fiscal stimulus from the US is possible is encouraging risk-taking today. Many large Asian centers were closed for holidays today, and a technical problem prevented the Tokyo Stock Exchange from opening.

FX Daily, October 19: Sterling Sparkles in Dollar Setback

FX Daily, October 19: Sterling Sparkles in Dollar Setback

Investors have not let the surge of the virus or uncertainty over the UK-EU talks or US fiscal stimulus to stand in their way. Sterling is leading the major currencies higher, returning to the $1.30 area, while global equities are trading higher.

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

FX Daily, November 9: Markets are not Waiting for Official Closure in the US

The new week has begun with robust risk appetites, driving stocks and stocks higher and sending the dollar broadly lower. Nearly all the equity markets in the Asia Pacific region gained more than 1%, except Malaysia and Indonesia.

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

FX Daily, November 13: Greenback Pares this Week’s Gains while the Turkish Lira Continues to Squeeze Higher

Overview: The largest bourses in the Asia Pacific region followed the US equity market lower, with the Nikkei posting its first loss in nine sessions. China, Hong Kong, and Australia moved lower as well. On the week, the MSCI Asia Pacific Index gained about 1% after rising 6.3% in the prior week.

FX Daily, August 17: The Dollar Softens to Start the New Week

FX Daily, August 17: The Dollar Softens to Start the New Week

The capital markets are looking for direction. Asia Pacific equity markets were mixed, with gains in China, Hong Kong, and Taiwan countering losses in Japan, South Korea, and Australia. European and US shares are trading slightly firmer.

FX Daily, August 21: PMIs Shake Investor Confidence

FX Daily, August 21: PMIs Shake Investor Confidence

The second disappointing Fed manufacturing survey report and an unexpected rise in weekly jobless claims helped reverse the disappointment over the FOMC minutes. Bonds and stocks rallied–not on good macroeconomic news, but the opposite, which underscores the likelihood of more support for longer.

Tags: #USD,China,Currency Movement,Featured,Japan,Mexico,newsletter,Turkey,U.K.