Swiss Franc The Euro has fallen by 0.27% to 1.0537 EUR/CHF and USD/CHF, March 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: A new phase of the market turmoil is at hand. Bonds are no longer proving to be the safe haven for investors fleeing stocks. The tremendous fiscal and monetary efforts, with more likely to come, have sparked a dramatic rise in yields. Meanwhile, equities are getting crushed again. Steep losses were seen in many Asia Pacific markets, with Australia off 6% and Hong Kong, South Korea, and India down more than 4%. The Bank of Japan’s ETF purchases are distorting the local equity performance with the Topix posting small gains while the Nikkei fell about 1.7%. European bourses are lower,

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brazil, cross currency basis swap, Featured, Federal Reserve, FX Daily, newsletter, South Korea, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.27% to 1.0537 |

EUR/CHF and USD/CHF, March 18(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: A new phase of the market turmoil is at hand. Bonds are no longer proving to be the safe haven for investors fleeing stocks. The tremendous fiscal and monetary efforts, with more likely to come, have sparked a dramatic rise in yields. Meanwhile, equities are getting crushed again. Steep losses were seen in many Asia Pacific markets, with Australia off 6% and Hong Kong, South Korea, and India down more than 4%. The Bank of Japan’s ETF purchases are distorting the local equity performance with the Topix posting small gains while the Nikkei fell about 1.7%. European bourses are lower, and the Dow Jones Stoxx 600 is off about 4% to give back yesterday’s gains in full plus more. The S&P 500 rose 6% yesterday and is giving three-quarters of it back. It has not risen for two consecutive sessions since February 11-12. In Europe, the more profound carnage is in the bond market today, where Italy’s 10-year yield is up over 50 bp. It is approaching 3% after being below 1% as recently as March 4. The German 10-year Bund yield is 17 bp higher near minus 26 bp. It was at minus 90 bp on March 9. The US 10-year yield rose 36 bp yesterday and is up another 7 bp today to 1.15%. The dollar remains firm against most of the major currencies, with the yen and Swiss franc the notable exceptions. Emerging market currencies remain under pressure, with the Mexican peso and Russian rouble posting more than 3% losses. Gold is off around $30 and continues to flirt with the 200-day moving average (~$1500), which it has not closed below for a couple of years. Crude oil prices are pushing lower. It is another 3.2% lower after losing more than 15% in the past two sessions. |

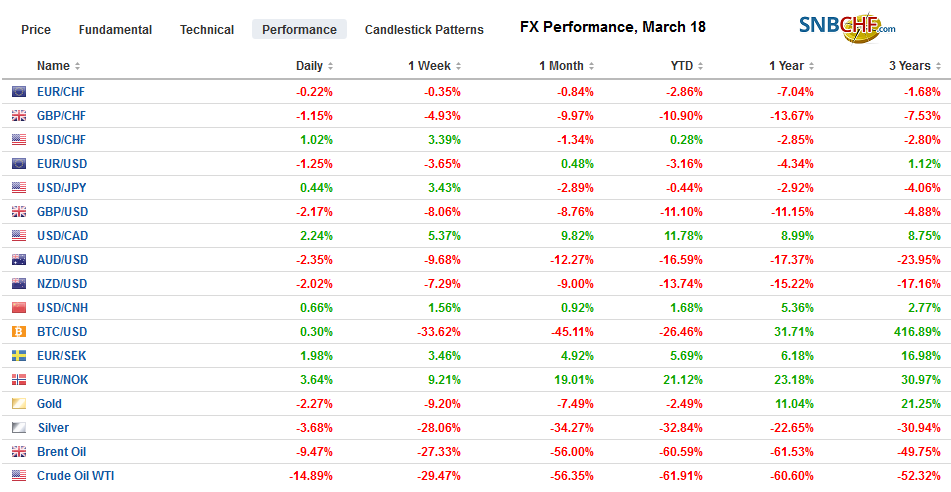

FX Performance, March 18 - Click to enlarge |

Asia Pacific

Governments and central banks continue to unveil new measures to cope with the public health crisis that is shaking the financial and economic systems to the core. Japan, for example, is considering a cash payout of JPY12k (~$112) per person. Australia is expected to announce new aid efforts tomorrow.

The South Korean won has been heavily sold as foreign investors liquidate local shares. The roughly $7.5 bln liquidation this month so far, is more than half of what foreign investors have sold over the past 12 months. The cost of securing the dollar jumped to its highest since 2009. The central bank intervened and capped the foreign exchange forward position of local banks.

The dollar-yen cross-currency basis swap stands around minus 69 bp. It finished near minus 85 bp yesterday. It is still reflected in elevated pressures. Consider that the 200-day moving average is near minus 30 bp. Japanese banks rely on the US repo market and cross-currency swaps. Some large players do not have direct access to the BOJ’s dollar auctions.

The dollar is consolidating at the upper end of yesterday’s range, but it is just below a band of resistance that extended from JPY107.80 to a little above JPY108.00, where around $4.5 bln of options have been struck that expire today. The sensitivity of the yen to falling stocks has eased over the past week or so. There has been no reprieve for the Australian dollar. Its losing streak is now into its eighth session. After being sold through $0.6000 yesterday, it fell to about $0.5925 in late Asian turnover before steadying in early European turnover. Initial resistance is seen near $0.6020. The dollar rose 0.25% against the Chinese yuan to settle the mainland session above CNY7.02. It continues to consolidate with the range set last Thursday (~CNY6.9685-CNY7.0370)

EuropeIn a provocative and potentially significant development, German Chancellor Merkel, for the first time, indicated a willingness to engage in a discussion about a common bond to help contain Covid-19. The idea, according to reports, was put forward by Italy’s Prime Minister Conte, who many seem to have underestimated. He was offered the job precisely because he was seen as weak, allowing, at the time, the two deputy PMs and coalition party leaders to dominate. Conte has gotten what no one has been able to do, and that is to get something besides “nein” as the answer. One way that discussions could go is that the European Investment Bank could issue “corona bonds,” perhaps insured by the European Stabilization Mechanism, which France reportedly suggested. These bonds could then be among the bonds the ECB buys in the secondary market. Cynics may suggest that “further discussions” is a political way to bury it. However, Merkel and Finance Minister Scholz did not dismiss it out of hand seems to reflect a fear of the coming economic and financial impact. It is also a good reminder to us as investors and business people that the crisis will call into question priors. One such prior, for example, is that the UK will end the standstill agreement at the end of the year and formally leave the EU. It appears that more people are willing to talk about the risk to the Olympics than the likelihood that an extension of the standstill agreement will most likely be necessary. |

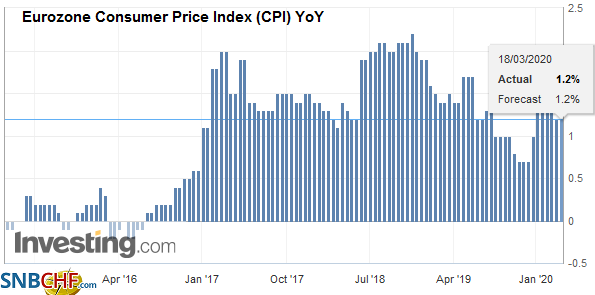

Eurozone Consumer Price Index (CPI) YoY, February 2020(see more posts on Eurozone Consumer Price Index, ) - Click to enlarge |

| The UK has announced a new support package. It includes a loan guarantee program for GBP330 bln (~15% of GDP) and GBP20 bln grant and tax cuts. Airlines, retailers, and hospitals are set to receive support. The Bank of England launched a lending facility to buy commercial paper.

European banks took $75.8 bln from the ECB’s dollar auction for the 84-day term and about $36.25 bln from its seven-day auction. Not since the middle of January have the banks taken more than $600 mln. Last Sunday, the Federal Reserve cut the cost of accessing dollars via to 25 bp on top of the OIS. The 3-month cross-currency basis swap had fallen beyond minus 120 bp yesterday snapped back to around minus 40 bp by the end of the session and is now quoted at a small premium for the first time since earlier this month. In contrast, the Swiss National Bank saw bids at its 84-day dollar auction for a minor $315 mln, while the seven-day facility saw $2.3 bln taken. UK banks took about $7.25 bln at the BOE’s 84-day dollar auction and about $8.2 bln for seven days. |

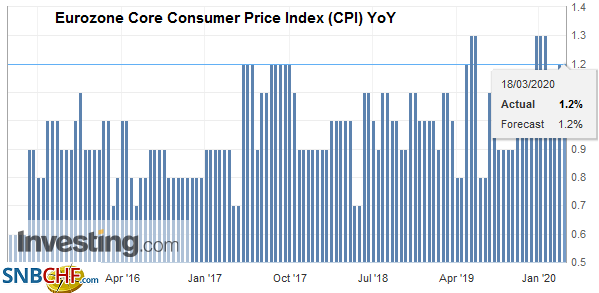

Eurozone Core Consumer Price Index (CPI) YoY, February 2020(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The euro is in a relatively narrow range near yesterday’s lows. It is holding above $1.0950 but has not been able to resurface above $1.1050. That said, recapturing the $1.11-handle would help stabilize the technical tone. Sterling briefly dipped below $1.20 in early European turnover, but buying emerged, and sterling has pared its losses. The intraday technicals suggest the recovery can be extended in the North American session. A move above $1.21 would help.

America

The has been a dramatic swing in the US fiscal stance in recent days. Last week, the Senate and the White House were balking at the House bill on partisanship and ideological grounds. Indeed, the House bill was a response in part to the initial push for a payroll savings tax cut, which was regressive and did not help a large swathe of people who were going to adversely impacted. Early yesterday, the White House (really Treasury Secretary Mnuchin and the Senate seemed to have settled on an $850 bln or so package. By the end of the session, the size had escalated to $1.2 trillion. The bond market got crushed like not seen since 1982. Consider the 10-year note yield settled just below 72 bp on Monday and shot up by 36 bp yesterday and is up another seven basis points today. A sharp steepening of the curve took place. It could be that investors become more optimistic about the growth and inflation prospects. That seems unlikely. Instead, the sell-off of the bonds is more likely to reflect the adjustment to the coming supply.

The Federal Reserve is reactivating facilities used during the Great Financial Crisis. The efforts to support the commercial paper market was complemented by the re-establishment of the Primary Dealer Credit Facility. During the crisis, it lent almost $9 trillion, making more than 20,000 transactions with financial institutions and foreign central banks. While it had been used for overnight loans, the new iteration allows for up to 90-day loans in exchange for a wide range of collateral. The Fed’s recognition of the seriousness of the economic and financial shock suggests that it will likely also restart a facility to support the asset-backed market.

The sharp and relentless gains in the dollar reflect a shortage in Europe and Japan. US banks, the main source of dollar funding, are understandably reluctant to lend to foreign banks During the Great Financial Crisis, this reluctance was a function of counterparty credit risk. The behavior is the same now, but the cause is different. US banks are scared not of the foreign bank’s creditworthiness, but because of their own perceived capital needs. Large corporations are not issuing unwanted commercial paper, though the Fed’s facility may be helpful nonetheless. They are drawing down their credit lines. At the same time, many borrowers, including households and small and medium-sized businesses, may struggle to service their debt. The volatility of the capital markets also tightens the willingness to lend. Other sources of revenue, such as underwriting and M&A work, is questionable. The continued low take-up in the Fed’s huge repo operations suggests a pushing on a string, as it were.

The continued drop in oil prices and the broad risk averseness is taking its toll on the Canadian dollar. Since February 21, the Canadian dollar has only risen in three sessions. The US dollar finished last week near CAD1.38 and today is pushing above CAD1.43. The next big chart point is near CAD1.47, the high from early 2016. Yesterday’s high was near CAD1.4270 and may offer initial support now. The greenback closed last week a little below MXN22 and was bid earlier today above MXN24. Here too, the technicals are stretched but are giving no encouragement to pick a dollar top. Initial support may be in the MXN23.50 area. Brazil’s central bank meets late today and is expected to cut the Selic rate by 50 bp to 3.75%. The dollar is at record highs against the Brazilian real, reaching BRL5.08 yesterday.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brazil,cross currency basis swap,Featured,federal-reserve,FX Daily,newsletter,South Korea,U.K.