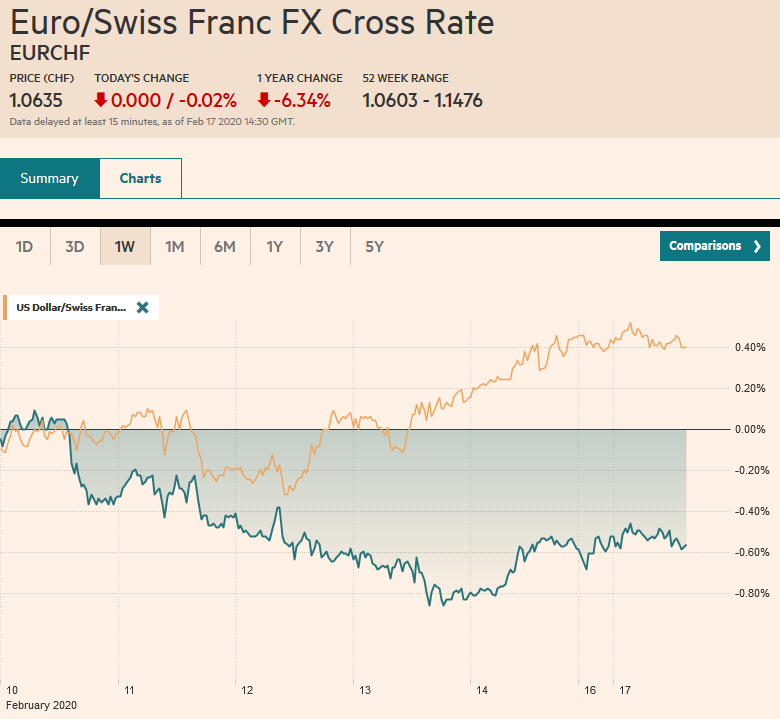

Swiss Franc The Euro has fallen by 0.02% to 1.0635 EUR/CHF and USD/CHF, February 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: It is only a US holiday today, but the global capital markets are subdued. In the Asia-Pacific region, equities traded lower with China and Hong Kong, the main advancers. The MSCI Asia Pacific Index has fallen in only two weeks since the end of last November, and that was during the last two weeks of January. Europe’s Dow Jones Stoxx 600 slipped in the previous two sessions but is recouping the losses fully today. It is being led by consumers, energy, and financials. US shares are firm in European turnover. Outside of a four basis point increase in China’s 10-year benchmark,

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, Currency Movement, Featured, Japan, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.02% to 1.0635 |

EUR/CHF and USD/CHF, February 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: It is only a US holiday today, but the global capital markets are subdued. In the Asia-Pacific region, equities traded lower with China and Hong Kong, the main advancers. The MSCI Asia Pacific Index has fallen in only two weeks since the end of last November, and that was during the last two weeks of January. Europe’s Dow Jones Stoxx 600 slipped in the previous two sessions but is recouping the losses fully today. It is being led by consumers, energy, and financials. US shares are firm in European turnover. Outside of a four basis point increase in China’s 10-year benchmark, yields are little changed. In Europe, yields are within a basis point of where they ended last week. The dollar is a little softer against most of the majors. The yen, sterling, and Norwegian krone are slightly lower. Among emerging market currencies, Eastern and Central European currencies, which underperformed last week on firm alongside, Singapore, China, and South Africa. Gold is paring the gains scored in the previous couple of sessions and is off around $3. April WTI is steady. |

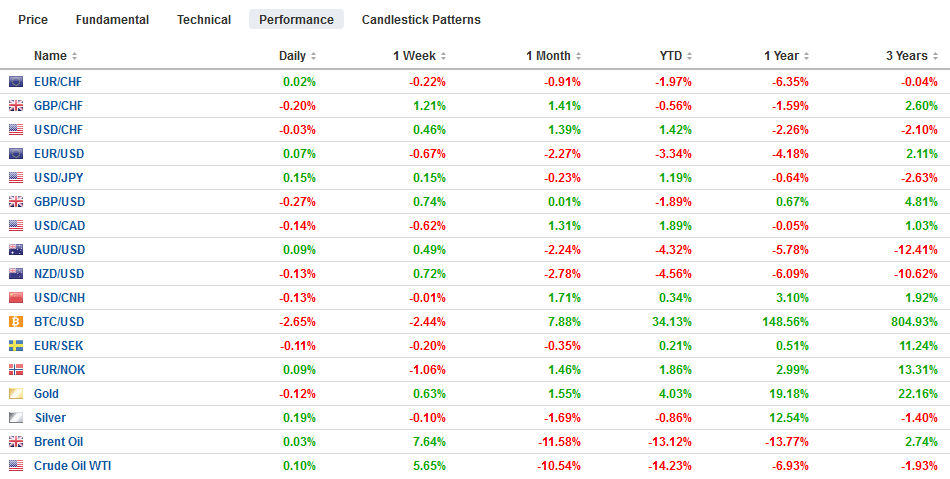

FX Performance, February 17 - Click to enlarge |

Asia Pacific

The coronavirus (Covid-19) contagion rates appear to be decelerating but have not turned down. The focus of observers seems to be shifting toward the number of severe or critical cases, which is running near 20%. China and Hong Kong have already started fiscal initiatives, and after revising down growth forecasts, Singapore is not far behind. The Philippines, Thailand, and Malaysia have cut rates. Indonesia is expected to reduce rates later this week. China cuts its Medium-Term Lending Rate (MLF) by 10 bp today (to 3.15%). When the new benchmark, the one-year Loan Prime Rate, is set on February 20 (4.15%), it is expected to fall by at least 10 bp (though the risk is of a greater decline). That said, investors need to take claims of the PBOC’s large injections of liquidity with a proverbial grain of sand. It did increase CNY200 bln at the new MLF rate and another CNY100 bln via a seven-day reverse repo. However, there was CNY1 trillion maturing today. Net-net, the PBOC allowed draining of liquidity. India did not cut rates last month, reduced reserve requirements for certain types of loans, and announced a new loan facility similar to the ECB’s long-term refinancing operations.

Japan’s Q4 GDP preliminary Q4 GDP estimate was horrible. The median forecast in the Bloomberg survey anticipated a 3.8% annualized contraction, but instead, economic activity fell 6.3%. This reflects a 1.6% quarterly contraction rather than the 1% economist expected. Despite the tax hike in October being smaller than the 2014 increase and a number of measures by the government to cushion the blow, the economy contracted by nearly as much as it did then (7%). Private consumption plunged 11% in Q4 compared with 18% after the previous sales tax increase. Business investment fell by 3.7%, more than twice the projection. Although exports fell, imports fell by more, allowing trade to make a positive contribution. Of course, the economy suffered a blow not just from the tax increase but from a couple of typhoons today. Investors are looking past Q4 19, and there is concern that the coronavirus may spur another quarterly contraction, with tourism and trade being hit.

Before the weekend, the dollar was confined to about a 20-tick range against the Japanese yen. Thus far today, the range is even narrower (JPY109.72-JPY109.88).Last week’s range was about JPY10955-JPY110.15, which might limit the price action in the coming days. The Australian dollar spent most of last week between $0.6700 and $0.6750. The technical indicators seem to favor the upside, and a close above $0.6750 may be among the first signs the next leg up has begun. The dollar advanced against the yuan in the last three sessions, but the gains were shaved today. A weaker yuan is consistent with the more accommodative fiscal and monetary stance.

Europe

A US energy official claimed that the Nord Stream 2 pipeline that would ship Russian gas to Germany under the Black Sea to bypass Ukraine has been thwarted. Whether this is true or aspiration has yet to be proven. US sanctions in December forced a Swiss underwater pipe-laying business to withdraw from the project. However, reports suggest that Russia’s Gazprom’s own pipe laying vessel may step-in to the vacuum. Several companies have invested nearly 6 bln euros as of a year ago in the project. In a different context, to be sure, Mexico’s President has still not recovered his credibility among investors since canceling a nearly $14 bln airport project that was a third completed.

Investors continue to wrestle with the implications of the resignation of Javid and the appointment of Sunak as Chancellor of the Exchequer. The Conservatives campaigned on fiscal austerity (reduce debt, keep net public investment below 3% of GDP, and run a balanced current budget). However, even before Javid resigned, the fiscal rules were being relaxed, and now the speculation is that a more expansionary budget will be delivered next month.

The euro initially extended its recent losses in early Asia to almost $1.0820, but in quiet turnover has edged higher toward $1.0850. The high from the end of last week was near $1.0860. It has not settled above $1.09 since last Tuesday. Although the $1.08 level may hold in the near-term, a break of could quickly see another half-cent drop Sterling is trading mostly in a quarter-cent range below $1.3050. Last week’s high was about $1.3070. Support is seen in the $1.2980-$1.3000 area.

America

At the weekend Munich Security Conference, a high-profile annual gathering, both US Secretary of State Pompeo and House Speaker Pelosi took a hard-line against China. They argued strongly against allowing Huawei, against which the US filed racketeering charges last week, to build out the 5G network. At the same time, the US is stepping up its efforts to defeat a Chinese national’s bid to become the head of the World Intellectual Property Organization in next month’s election. Despite the heated rhetoric, especially about domestic issues, there appears to be a broad bipartisan consensus in the US to make a greater effort to counter China’s ambitions in the multilateral agencies. Nevertheless, the US unilateralist approach undermines its ability. The US belatedly and without coordination, tried to block China’s push to head the Food and Agriculture Organization. It resulted in sapping support from the French candidate, allowing the Chinese candidate to win.

France’s Alstom reportedly has struck a deal to acquire Canada’s Bombardier’s train business for more than $7 bln. The potential acquisition was first reported around three weeks ago. Some participants try to take a view on the foreign exchange market based on M&A deals. There is good reason to be skeptical. First, the acquirers often protect their international bid by taking out options, which may best address contingent risk. Second, the average daily turnover of the euro, according to last year’s BIS survey, was near $2.2 trillion, and the Canadian dollar was about $330 bln. Its impact would quickly evaporate. Third, companies often consider borrowing the needed foreign currency rather than buying it and thereby neutralizing the foreign exchange exposure. That said, the technical indicators do seem to favor the Canadian dollar, which had weakened to the lower end of a six-month range.

Indeed, the Canadian dollar among the strongest currencies in what has been a relatively quiet foreign exchange session in Asia and Europe. The US dollar has been sold through the shelf formed in the second half of last week (CAD1.3235-CAD1.3240) to test the 20- and 200-day moving averages (~CAD1.3220). A break of CAD1.3185 would lend credence to the bullish technical case for the Canadian dollar. The peso is paring last week’s rally. It gained in every session last week, including after the central bank cut rate by 25 bp. The peso was bought in late Asia today and initially extended last week’s gains (~MXN18.5235), but some light selling pressure in Europe brought it back to MXN18.58. Although the intraday technical indicators suggest that the dollar’s bounce may be nearly over, the risk may extend toward MXN18.62. The Dollar Index is in a narrow range of about 10-ticks (99.05-99.15) to trade within the pre-weekend range. Sentiment is constructive, but the technical readings are stretched.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,China,Currency Movement,Featured,Japan,newsletter