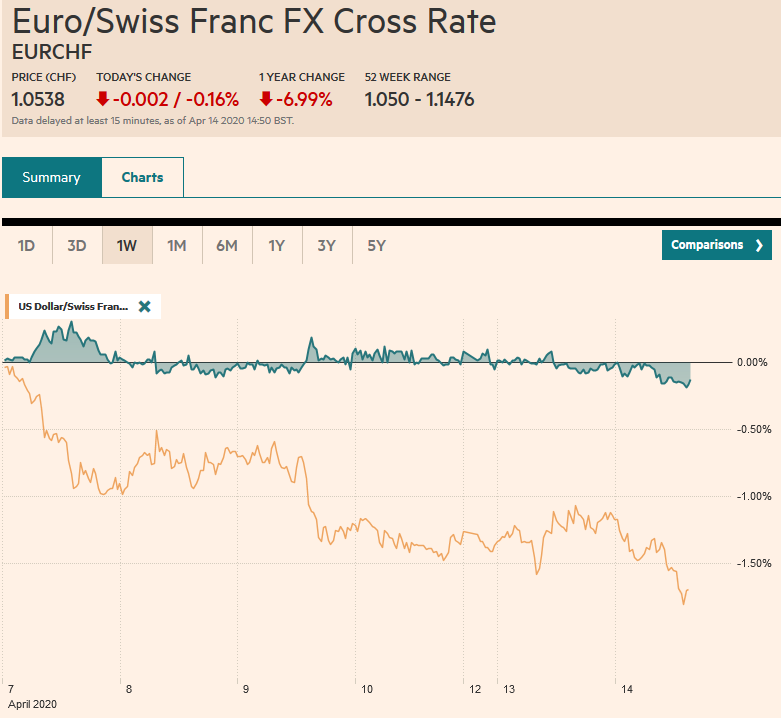

Swiss Franc The Euro has fallen by 0.16% to 1.0538 EUR/CHF and USD/CHF, April 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Risk appetites have returned today after taking yesterday off. The MSCI Asia Pacific Index advanced every day last week, slipped yesterday, and jumped back today. Most of the national benchmark advanced at least 1.5%, and the Nikkei led the way with a 3% rally to reach its best level since mid-March. European markets re-opened after the long weekend. Last week’s four-day rally is being extended today by almost 1% in the European morning. US shares are firm, and the S&P 500 loos set to recoup most of yesterday’s decline. Benchmark yields are mostly higher. Italian bonds are eight

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, COVID-19, Currency Movement, Featured, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.16% to 1.0538 |

EUR/CHF and USD/CHF, April 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

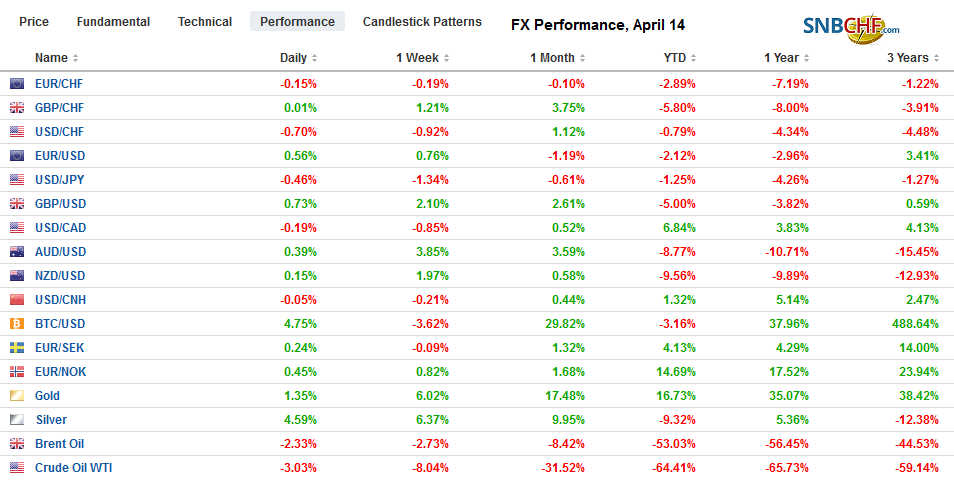

FX RatesOverview: Risk appetites have returned today after taking yesterday off. The MSCI Asia Pacific Index advanced every day last week, slipped yesterday, and jumped back today. Most of the national benchmark advanced at least 1.5%, and the Nikkei led the way with a 3% rally to reach its best level since mid-March. European markets re-opened after the long weekend. Last week’s four-day rally is being extended today by almost 1% in the European morning. US shares are firm, and the S&P 500 loos set to recoup most of yesterday’s decline. Benchmark yields are mostly higher. Italian bonds are eight basis points higher while peripheral yields are 3-4 bp higher. The US 10-year yield is a little below 75 bp. Rekindled risk appetites remove some demand for US dollars, and the greenback is mixed. It is a little heavier against the dollar-bloc currencies. Although the South African rand has appreciated and eastern and central European currencies are mostly firmer, the JP Morgan Emerging Market Currency Index is a little heavier for the second session after rising every day last week. Gold is holding above $1700, and May WTI is softer and struggling to stay above $22 a barrel. |

FX Performance, April 14 - Click to enlarge |

Asia Pacific

Singapore, South Korea, and China have seen new flare-ups of infections, and several countries in Asia and Europe are extending their lockdowns. China reported the highest number of new daily cases in almost six weeks on Sunday (108). The overwhelming majority of new cases are reportedly traced to people returning to China from abroad. Roughly half the new cases traceable to Russia and Chinese cites near the border indicated they would tighten border controls and quarantine measures (28 days in quarantines and nucleic and antibody tests) on new arrivals.

China reported a $19.90 bln trade surplus in March. It had recorded a combined deficit of $7.1 bln in the January-February period. Exports fell by 6.6% (in dollar terms), which is less than half the decline expected and a little less than a third of the decline reported in the first two months of the year. Exports to the EU (-24.2%), the US (-20.8%) and Japan (-1.4%) fell. Imports eased by a little less than 1%. Economists had expected a decline closer to 10%. Imports from the US fell 12.5% and from the EU 6.5%. Imports from ASEAN and Japan rose (10.5% and 4.8%) respectively. Those looking for insight into progress meeting the US trade deal will note that agriculture imports from the US rose 110% in Q1, led by a more than 200% increase in soy purchases. China imported nearly three times more pork in March (391k tons) than March 2019. Pork imports in Jan-Feb were more than double the comparable 2019 figures. Separately, the surge in integrated circuit imports (~43.5% after a 10.5% decline in Jan-Feb) appears to reflect the return to manufacturing and assembly of electronic goods as the economy re-starts.

Just like it makes little sense for the US to be so dependent on China for some types of medicine and rare earths, it makes little sense for China to be dependent on foreign chip makers. We have noted Japan’s exports of semiconductor fabrication equipment to China. Now one of China’s chipmakers (Yangtze Memory Technologies) claims to have the capability to build the most advanced chips (128-layer 3D NAND flash memory chips). Presently, the 96-layer 3D NAND is being done by global players, but the 128-layer is the next generation.

The dollar broke below JPY108 yesterday and has unable to resurface the area today. There is an option for about $760 mln that is struck there that will expire today. Support is seen closer to JPY107.00, and an option for $1.1 bln at JPY107.05 will be cut today. The Australian dollar pushed through $0.6400 to extend its streak to the seventh session. When the rally began, the Aussie was below $0.6000. The $0.6450 area corresponds to a (61.8%) retracement of this year’s decline. Initial support is pegged near $0.6370. The technical indicators are getting stretched and caution against chasing the market at these levels. The PBOC set the dollar’s reference rate a little above CN7.04 today, though the bank models implied something closer to CNY7.0375. The dollar is back into the CNY7.05-CNY7.12 range. We note that Indonesia’s central bank defied expectations and left the key rate steady at 4.5%. The rupiah is steady after falling about 3.8% in the past two sessions.

Europe

While France is extending the lockdown to May 11 and the UK expected to extend its to May 11, Austria is one of the first countries to ease restrictions. Italy had extended its lockdown at the end of last week into early May. Spain reported the fewest new cases in three weeks, and Germany reported a decline in infections for the fifth day. There is some concern that the numbers may have been depressed by the long holiday weekend, so the reports in the coming days are needed for confirmation.

The euro is trading quietly inside yesterday’s range (~$1.0895-$1.0970). It has been confined to less than a quarter-cent range on either side of $1.0925. There appears to be near-term potential toward $1.10, where an option for 733 mln euros will expire today. Sterling finally pushed above $1.25 yesterday, after first testing it in late March. Former resistance has now become support, and sterling has held above $1.25 today. It reached $1.2575, for the first time since March 13, when it traded as high as $1.2625. Above there, the 200-day moving average is near $1.2655. The technical readings are getting stretched.

America

Two groups of states, one on the West Coast (California, Oregon, and Washington) and one on the East Coast (New York, New Jersey, Connecticut, Pennsylvania, Deleware, Rhode Island, and Massachusetts) are trying to coordinate the re-opening of the economies. Together the nine states account for about a third of US GDP and 105 mln people. The press is playing up the conflict with the White House as the President claims complete authority. We suspect the drama may not be so great. The White House deferred to the states for shutdowns and will likely provide only broad guidelines as local containment varies greatly throughout the country. Moreover, if some lockdowns are needed again, as has been the case in several Asian countries, better that local officials have discretion.

Recognizing an easing of market tensions, the Federal Reserve announced it would reduce the frequency of its repo operations starting May 4. It would conduct one, not two overnight repo operations a day. The three-month term repo would be held once every two weeks rather than weekly. The one-month operation would continue on a weekly basis. The maximum amount was unchanged at $500 bln.

Texas regulators are expected to meet today to decide if the US will join OPEC+ and make additional cuts in output. Those that want to as thought to be in the minority. The signals from the White House suggest market forces alone will do the job.

The US reports import/export prices today, which do not garner much market attention even in the best of times. The US earnings season starts today before the equity open with JP Morgan and Wells Fargo reports. While trading revenue may have risen, there is concern that debt will be marked down as borrowers struggle in the shutdown. Meanwhile, recall that LIBOR eased last Thursday, the last time it was set, by 9 bp, the most in a month, to a hair below 1.22%. It remains elevated, and further easing is anticipated as the Fed’s commercial paper facility is launched today. The Fed’s Bostic, Bullard, and Evans speak today ahead of the Beige Book report due tomorrow.

The US dollar fell to almost CAD1.3855 yesterday, its lowest level since mid-March, but has stabilized today. It is reaching the session high near CAD1.3920 in late European morning turnover. Above there, and the greenback encounters resistance in the CAD1.3960-CAD1.3980 area. A move back through CAD1.40 would suggest a near-term low is in place. The US dollar is consolidating against the Mexican peso inside yesterday’s range (~MXN23.2460-MXN23.8660). A break of that range will likely point the near-term direction. Broadly speaking, the peso appears more correlated with the general risk appetite (S&P 500 proxy) than oil prices.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

FX Daily, February 24: Stocks Slammed and Yields Drop as Virus Containment Fails

Overview: The ring of containment of Covid-19 has grown from China. The new frontline is Japan, South Korea, Italy, and Iran. A lockdown of around 50k people near Milan and Austria blocking trains from Italy is scaring investors. Asian markets fell, but South Korea bore the brunt with a nearly 4% decline. The national holiday in Japan spared local equities.

FX Daily, November 5: Animal Spirits Remain Animated

FX Daily, November 5: Animal Spirits Remain Animated

The prospects that the US-China deal could include some rolling back of existing US tariffs helped underpin risk appetites. After new record highs in the US S&P 500 and NASDAQ, Asia Pacific markets marched higher, and the MSCI Asia Pacific reached its highest level since August 2018. A small rate cut by China and catch-up by Tokyo, which was on holiday on Monday, helped extended the regional rally for the 14th session in the past 17.

FX Daily, November 21: Markets Hear What it Wants from China’s Chief Negotiator, but HK maybe New Obstacle

FX Daily, November 21: Markets Hear What it Wants from China’s Chief Negotiator, but HK maybe New Obstacle

Overview: The strongest signs to date that even phase one of a US-China trade deal is proving elusive helped spur the risk-off mood that had already been emerging. The S&P 500 fell by the most in a month (~-0.40%) yesterday, closing the gap from last week we had noted was the risk, and follow-through selling was seen in Asia Pacific and Europe.

FX Daily, December 09: China’s Steps-Up Import Substitution Strategy while USMCA Comes Down to the Wire

FX Daily, December 09: China’s Steps-Up Import Substitution Strategy while USMCA Comes Down to the Wire

The important week is off to a slow start. While the MSCI Asia Pacific benchmark extended its gains for a third session, European and US shares are struggling. The Dow Jones Stoxx 600 is consolidating its pre-weekend 1%+ rally, while US shares are trading heavier after rallying for the last three sessions.

FX Daily, December 27: Equities Rally While the Dollar Slumps into the Weekend

FX Daily, December 27: Equities Rally While the Dollar Slumps into the Weekend

Overview: Equities are finishing the holiday-shortened week on a firm note, encouraged by strong holiday internet sales in the US. Most markets in the Asia Pacific region advanced except China and Thailand, while Japanese markets were mixed after weak industrial output and retail sales. The MSCI Asia Pacific Index rose for the fourth consecutive week.

FX Daily, January 15: Phase 1 Trade Deal Shifts Terrain of US-China Rivalry

FX Daily, January 15: Phase 1 Trade Deal Shifts Terrain of US-China Rivalry

News that US tariffs on China will remain until through at least the November US election and continued US attempts to stymie China (e.g., more curbs on Huawei under consideration and stepped up efforts to force it to cut subsidies to business) have taken some momentum from the push into risk assets. The MSCI Asia Pacific Index snapped a four-day advance today, with only Australian equities among the large regional markets able to sustain upticks.

FX Daily, March 11: US Over-Promises and Under-Delivers, while BOE Steps Up with 50 bp Rate Cut

FX Daily, March 11: US Over-Promises and Under-Delivers, while BOE Steps Up with 50 bp Rate Cut

Overview: The S&P 500 and Dow Jones Industrials sold off after the higher open and briefly traded below yesterday’s lows. Investors seemed disappointed that the Trump Administration was not ready with specific policies after Monday’s tease that had initially helped lift Asia Pacific and European markets earlier on Tuesday. This sparked a sharp decline in Europe into the close.

Tags: #USD,China,COVID-19,Currency Movement,Featured,newsletter